Image Source: Pexels

Long-time readers know we place little faith in sentiment indicators. They capture a very specific moment and can change with little correlation to economic data. They serve the purpose of determining the “mood” of a certain segment of the population at any given time, but one should not make investment decisions based on them.

If you think about it, value investing is essentially betting against sentiment, isn’t it? We tend to be sellers when there is euphoria and buyers when all seems lost. We profit off sentiment being wrong.

“Davidson” submits:

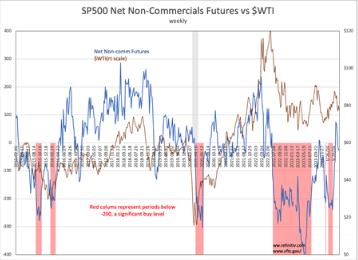

The SP500 rose on this week’s pessimistic sentiment numbers. The three sentiment indicators in this note are the SP500 Net Non-Commercial Futures, the 10yr minus the 3mo Treasury (Yield Curve), and WTI (West Texas Intermediate Crude Oil Price). Each is used to hedge bets on institutional economic expectations. The single event this week which said much about the institutional mind-set was Nvidia’s (NVDA) stellar earnings report that created the headline, NVDA Tops $2.5 Trillion As Traders Sell Everything Else On ‘Good News’. NVDA’s market cap rose by roughly the same amount everything else declined with the Dow Jones falling $600.

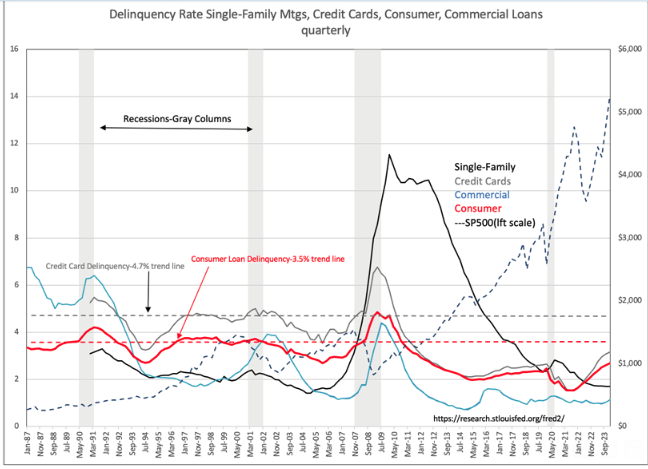

The day NVDA reported, May 23rd, the SP500 opened at $5,340 and closed at $5,267. It recovered to end the week at $5,304. NVDA had a rise of more than 20% for the week but was not enough to offset the declines elsewhere. Those who continue to bet on Mega-tech, as the only option expecting an economic slowdown with lower interest rates, are still leading this charge despite the Consumer Delinquency rates, also reported during the week, showing no signs of distress. Fundamentals continue to not support a pessimistic stance.

It has been an unusual period of pessimism which is tied to the Manufacturing PMI below 50. The Flash PMI was reported at 50.9 during the week to no effect. This indicator is pure market psychology but can influence business behavior if it signals strongly in a single direction. The Manufacturing PMI declined below 50 twenty-seven times for the last nine recessions with several signals occurring after a recession ensued. It is not a very reliable indicator based on how Purchasing Managers feel about the economy. But when pessimistic, no Purchasing Manager wants to be odd-man-out saying business is good when the cohort is pessimistic. The risk of being wrong when the majority opinion is negative can be career-ending. Very few do it. One is never faulted for being with the crowd. The SP500 pricing is correlated with the PMI. This is precisely why a PMI below 50 becomes a good equity buy signal making it a good time to look for value in areas few are looking for the best returns. That means, not NVDA!

Equities remain favored vs fixed income, especially those well-managed companies with discounts to historical financial performance who can pass on inflation cost profitably.

More By This Author:

Consumer Delinquencies Rising

Sentiment And Data Not Matching

Flush Money Market Funds Typically Mean Rally

Comments

Log in or sign up to join the conversation.