Market Analysis:

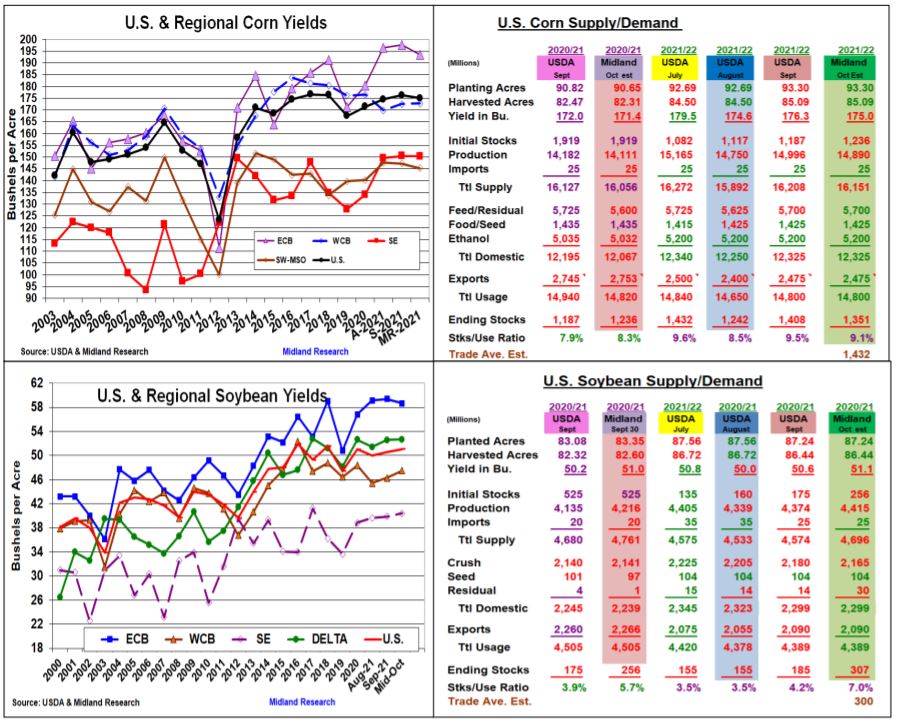

The USDA’s recent ending stocks updates had some surprising again this year. Soybeans (SOYB) hefty jump led the way with a 81 million larger carryover than was expected while corn was modestly higher and wheat’s September 1 stocks were 72 million lower than trade’s average estimate.

Changes in crop sizes were a significant part of these divergences along with some summer demand swings for US crops. These higher beginning corn (CORN) and soybean stocks have added to 2021/22 supplies, but the USDA’s October 12 US crop reports remain highly important in determining the available bushels for upcoming US crops.

Last week’s 49 million bu. rise in corn’s 2020/21 stocks occurred on a combination of a slight rise in exports, a drop in feed demand & a decline in last year’s crop because of slightly smaller area & yield. Field reports suggests that late season stalk disease issues could reduce the ECB’s lofty September 197 bu average yield by 4 to 193 bu. Interestingly this yield would still be above 2018’s previous 191 bu regional record.

Dryness in the SW and modest harvesting in the WCB so far suggests limited to stable yields in the other regions. Overall, a slight yield decline to 175 bu is anticipated. With no demand changes, October’s corn ending stocks could decline 57 million to 1.351 billion.

Soybeans’ 81 million larger 2020 US output upped this fall’s 2021/22 beginning stocks by the same amount. A late surge in exports appears to have sliced last year’s seed & residual demands to minimal levels. While the ECB and the South has been concentrating on their corn harvest, the W Midwest focus has been on their soybeans. Field reports of better bean yields despite the region’s dryness suggests the region’s average might increase 1.2 bu to 47.5 bu. The ECB might slip 0.7 bu on some disease issues while the Delta and SE remain steady near their 2017 and 2020 record levels.

Overall, a 0.5 bu rise in the October’s soybean yield is anticipated to 51.1 bu producing 4.415 billion bu crop. A 307 million 2022 carryover will occur if 2021/22 demand levels are left unchanged from last month.

What’s Ahead:

Wheat’s (WEAT) smaller US crop has tighten stocks to 2007/08 levels providing support to corn. This year’s building La Nina weather on S America’s corn & bean plantings along with US harvest yield reports will be price factors.

China’s actions with the Phrase 1 accord ending also remain important.

Still looking to add 10-15% sales to 20-25% levels at $12.90-13.10, $5.70-85 & $7.75-95 KC wheat prices.

Comments

Log in or sign up to join the conversation.