Market Briefing For Thursday, June 9, 2022

'Dispersion of holdings' is the latest rational presented investors to avoid air-pockets or landmine disasters going forward. In reality, much of that is now behind and has prevailed at least since the Fed pre-announced their intent to slam on the monetary brakes.

Risks on the mega-caps, rebounding after the prior couple months evacuation (as the Generals retreated to rejoin the troops already hunkered-down in the trenches), remains, although 'if' things go just right (that's the Fed threading of the needle for a 'soft-ish' landing, which is by no means certain) .. maybe less downside risk than those called for a collapse (typically the permabears).

On the very short-term 'front' (as in a theater of war), we've got tomorrow first the ECB move 'probably' to tighten policy in the face of stagflation in Europe. I know the pundits say they won't, but my hunch is they will have to join the Fed approach, even as it tends to be slightly counterproductive for the moment.

This is reflected a bit in a poor 10-year T-Note Auction here, and the poor one yesterday, reflect this tone of 'bring on inflation', as Governments can't forever get away with Quantitative Easing without repercussions. Foreign currencies are getting killed in countries that did that (Japan for-instance), and it was rife in a few others (South America particularly), some now are learning lessons.

In-sum:

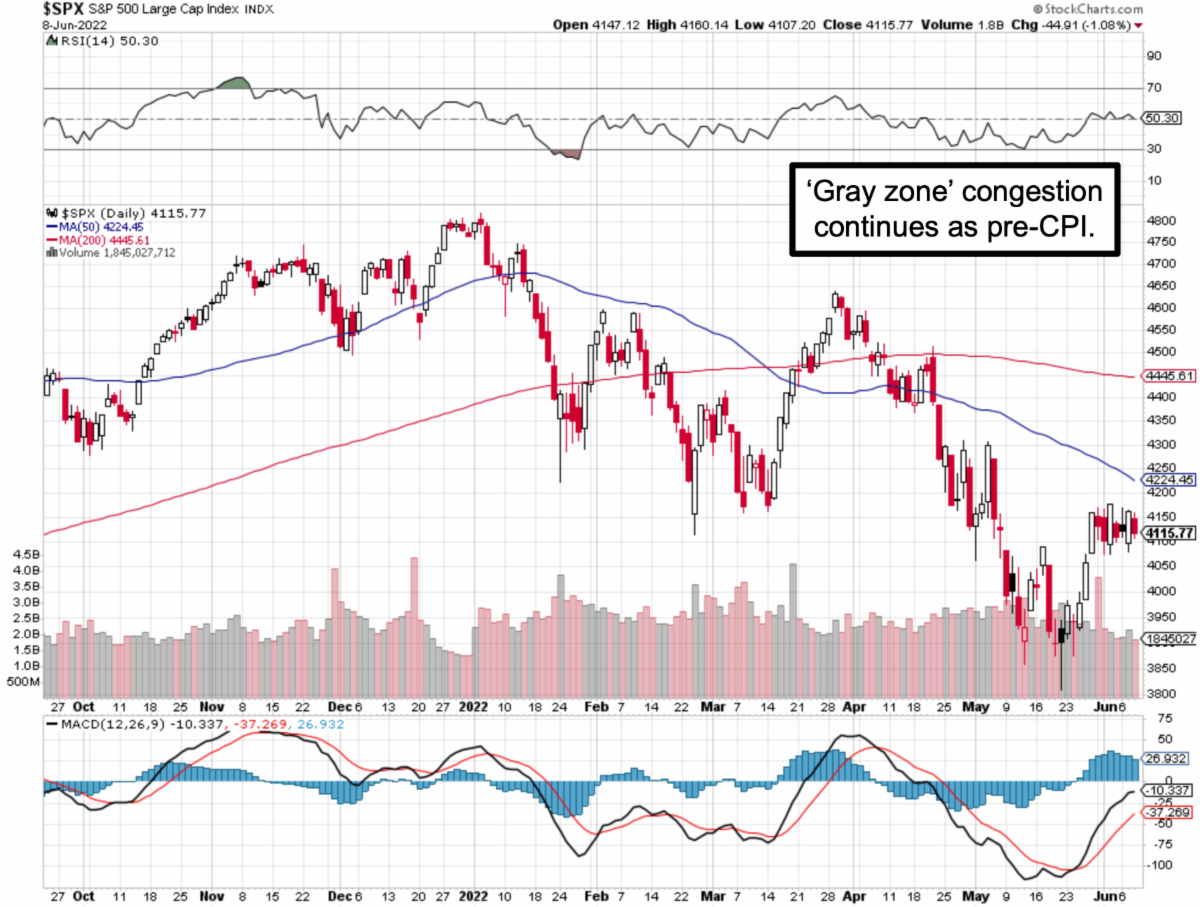

Little has changed, as S&P vacillates slightly defensively but within a congestion zone all week so far, that I referred to last weekend as 'gray zone'.

This is an indecision pattern bumping-up against resistance where targeted in my rebound/relief call from the also anticipated low near S&P ~3800. So, the goal for the snapback, fueled initially by short-covering, was ~4100-4200 S&P and we bounced around generally in the middle of that target area.

Even beyond (as well as tied-to) what happens is Oil prices, as contended for more than the past year. If it doesn't fade for one reason or another, there is nothing else but 'demand destruction'. We're not quite there yet, though the 'credit card' and 'savings' data I shared on the weekend suggest people at this point will do whatever (draining resources) to fuel traditional driving habits (if Oil doesn't decline until 'demand destruction', it's worse than stagflation).

The unanswered question is whether 'winter is coming for the stock market', a topic I've broached often by describing the bifurcated behavior over a year or so. That was (for any new readers) the distribution under-cover of strong S&P and NDX/QQQ action, as 'buybacks' aided and abetted the false Index upside that led to the historically high 'insider selling'.

Now we have timid but visible insider buying, but that doesn't mean anything's likely in terms of bullish phenomenon in the near-term. In reality it likely is not. However, the worst of the impact of Oil's projected advance and the Ukraine 'war', is probably being felt now, so 'if' CPI jumps and markets are walloped again, it probably will prove to be a better time to enter than to exit. TBD.

This is an excerpt from Gene Inger's Daily Briefing, which typically includes one or two videos as well as more charts and analyses. You can subscribe for more