An 'outside-down' week implies lower prices ahead. That's a traditional big technical warning by making a higher S&P high, lower low and lower close in the same week. However it was also 'Quadruple Expiration'; more recognition that the Fed is at-risk of overdoing it; and the economic slowing actually being felt (for instance lower forward airline bookings, while some claim opposite).

There's been a consolidation of pessimism; 'after' months of negative action; and that's part of why we are not surprised to see a 'wide divergence' of 2023 earnings expectations (and so on); given that slowing top-line and economic growth were looked for over recent months. Eventually markets tend toward discounting the recovery (and that includes a reversing Fed posture) even as they talk of staying 'higher for longer'.

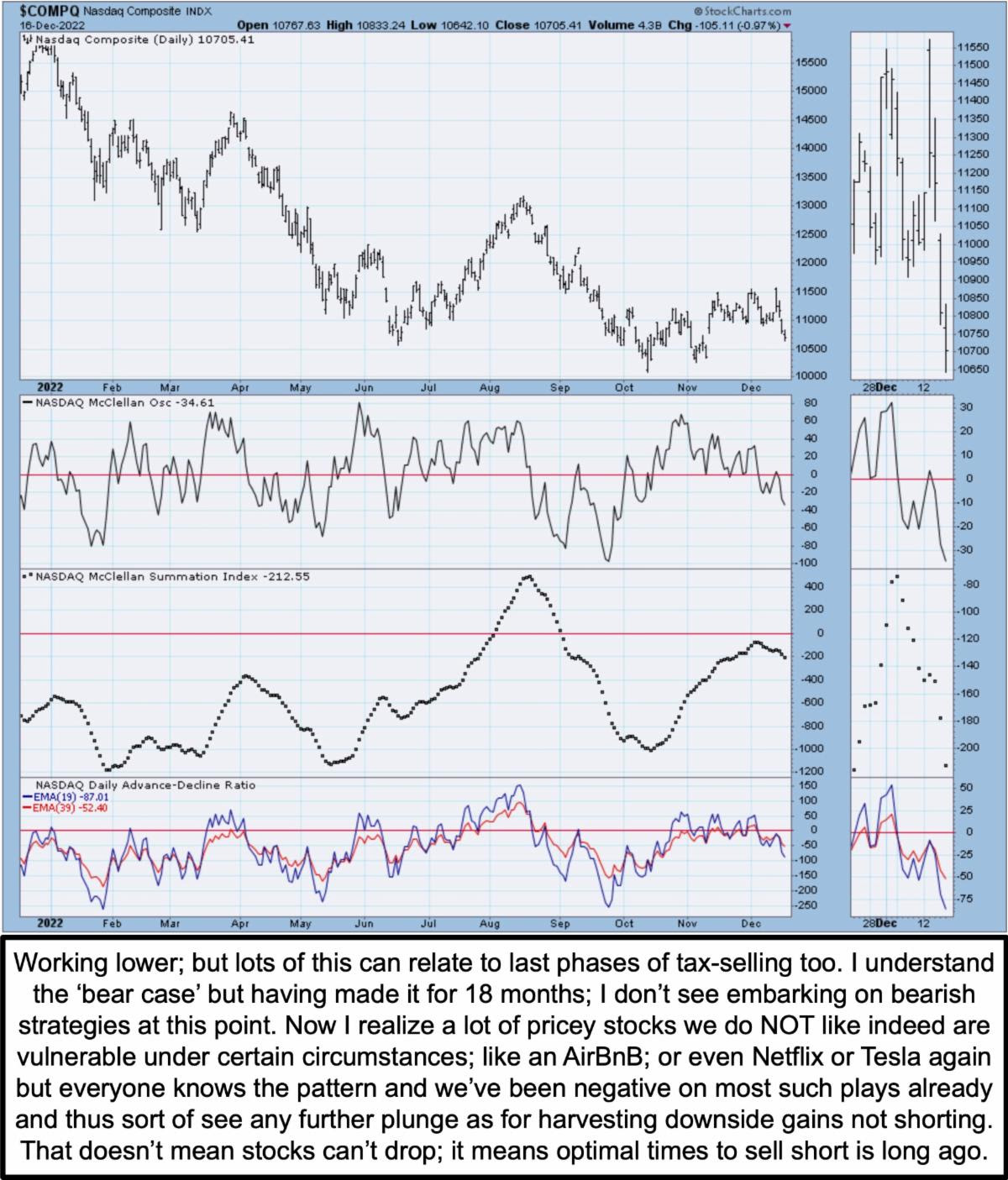

All the bears jumping on the downside case 'now, might be right temporarily; but ultimately will pay a price for doing so more than a year and a half after the actual distribution was subtly ongoing under cover of buybacks / S&P.

Most major 'shocks', including inflation, war, pestilence (well slightly); storms, Oil price surge and contraction; as well as rolling Covid abroad and liquidation of insiders having preceded all this by as much as a year or more.. well that's not to say the higher interest rate crusade of the Fed can't break furniture for awhile longer; it's to say that barring another 'black swan' a lot happened.

In sum: the Fed smashed the 'wealth effect' for Americans; after creating the preceding bubble in spending and wherewithal for the masses by overstaying low rates for too long, as argued in 2021. Major insider selling occurred amid the buybacks; and even that was funded by low-interest coupons at the time (for a lot of the companies).

We viewed that as distribution under strong S&P / NDX cover, as it sure was. Now we are mostly premature; but view purges as accumulation under cover of a weak market, which broadly got far weaker than the S&P. So we won't deny S&P and NDX could work even lower (valuation issues and stupid high PE multiples still around for some of them given 2023 prospects); but for the already-crashed stocks, which require a period of healing and base-building, it is likely to look like time for accumulation on dips when viewed a year hence.

So the multiple needs to come down; it's call compression. There's logically no reason (nor has there been) for an S&P multiple expansion for 2022 or in 2023; but somehow many analysts just figured out stocks were risky recently.

Typically this means the majority of pain .. especially for the few sectors that should do relatively better . . . like healthcare, energy or even semiconductors in some ways . . . while early cycle industries like Industrials should be lower; but don't forget you have huge infrastructure programs that disrupt the mix of stocks within such areas (those that have huge contracts vs. those that don't).

Looking at the dislocations of the market, this is not a great time to step into a slew of 'real estate' REIT's, because valuations were at insane levels; almost a twin of SPAC's, which have already crashed more than even we thought. But it's is not not a great time for some; and probably bumping along lows for others. Free cash-flow yields look good in energy; though that's volatile too.

Bottom line: there's not a lot new to add for now. We got through Expiration pretty well; and as I mentioned I personally thought we'd get late firming and we did. I also acknowledged taking a shot with options on a limited basis in a couple stocks. Again I'm not entirely confident about the market's early 2023 behavior; much less a post-Expiration rebound; but that might be the likelihood. To be a bit cautious I decided to play it with options a bit; and not common shares; recognizing that Calls are worthless if expiring at a level below the strike. Just a bit of (bored?) gambling today in weakness.

Hah. Really nothing changed and most of the variables are known; and while technicians keep telling us how significantly negative this week 'was' and the Fed-heads speaking amplify the downside, the market isn't quite so inspired with negatively as some of the pundits seem to be.

Purge or not early Monday; probabilities favor a post-Expiration rebound.

More By This Author:

Market Briefing For Thursday, Dec. 15

Market Briefing For Wednesday, Dec. 14

Market Briefing For Tuesday, Dec. 13

Comments

Log in or sign up to join the conversation.