Major Compression Regimes In Multiple Markets…

What an adaptive worldview means is that whenever you learn a new concept in an ill-structured domain, you know not to oversimplify — that is, to represent it as a single principle or concept. You do not try to reduce. You instead know to search for new, different cases in order to collect a cluster of prototypes in your head, and let that cluster inform your understanding of the concept. If you encounter a new case, you update the concept, because the concept is only useful when you know how it is instantiated in reality. ~ Cedric Chen via the post “Investing’s Big Blind Spot” by Tom Morgan

In this week’s Dirty Dozen [CHART PACK], we cover more recession signals, bullish price action in the main markets, a BIG set up in the US dollar, a major compression regime in bonds, and more…

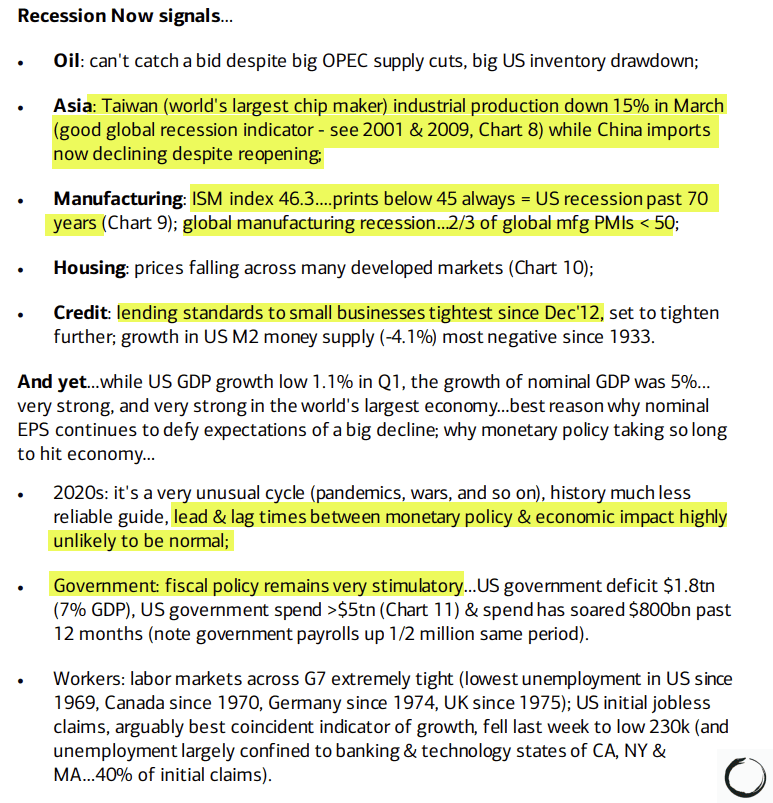

- Summary bullet points from BofA’s latest Flow Show with highlights by me.

- BofA is quite bearish… We think a recession later in the second half of this year is likely but excess consumer savings, amongst a few other cycle peculiarities, means the lead/lags this time around are not typical. So weak opinions weakly held.

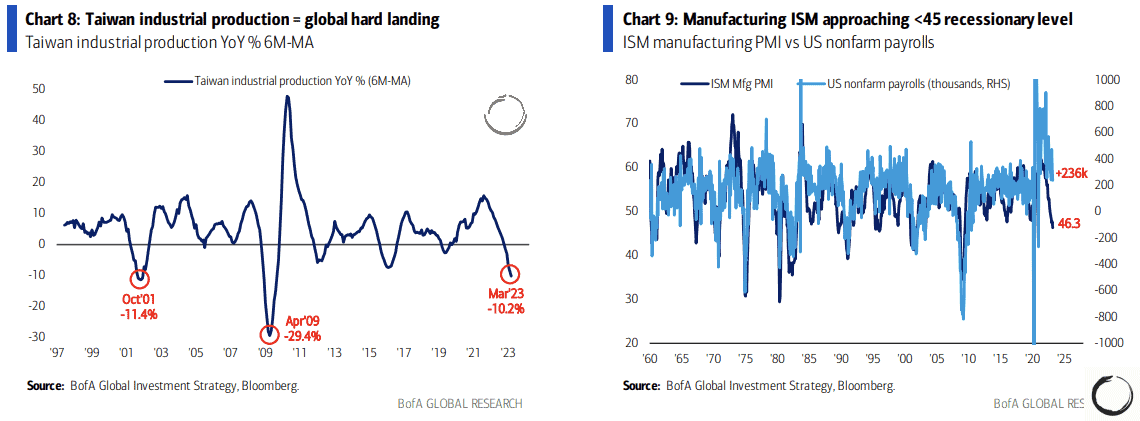

- Respect the tape… The Qs continue to trap bears and steadily rise in a Bull Quiet regime. This is not a tape you want to be short.

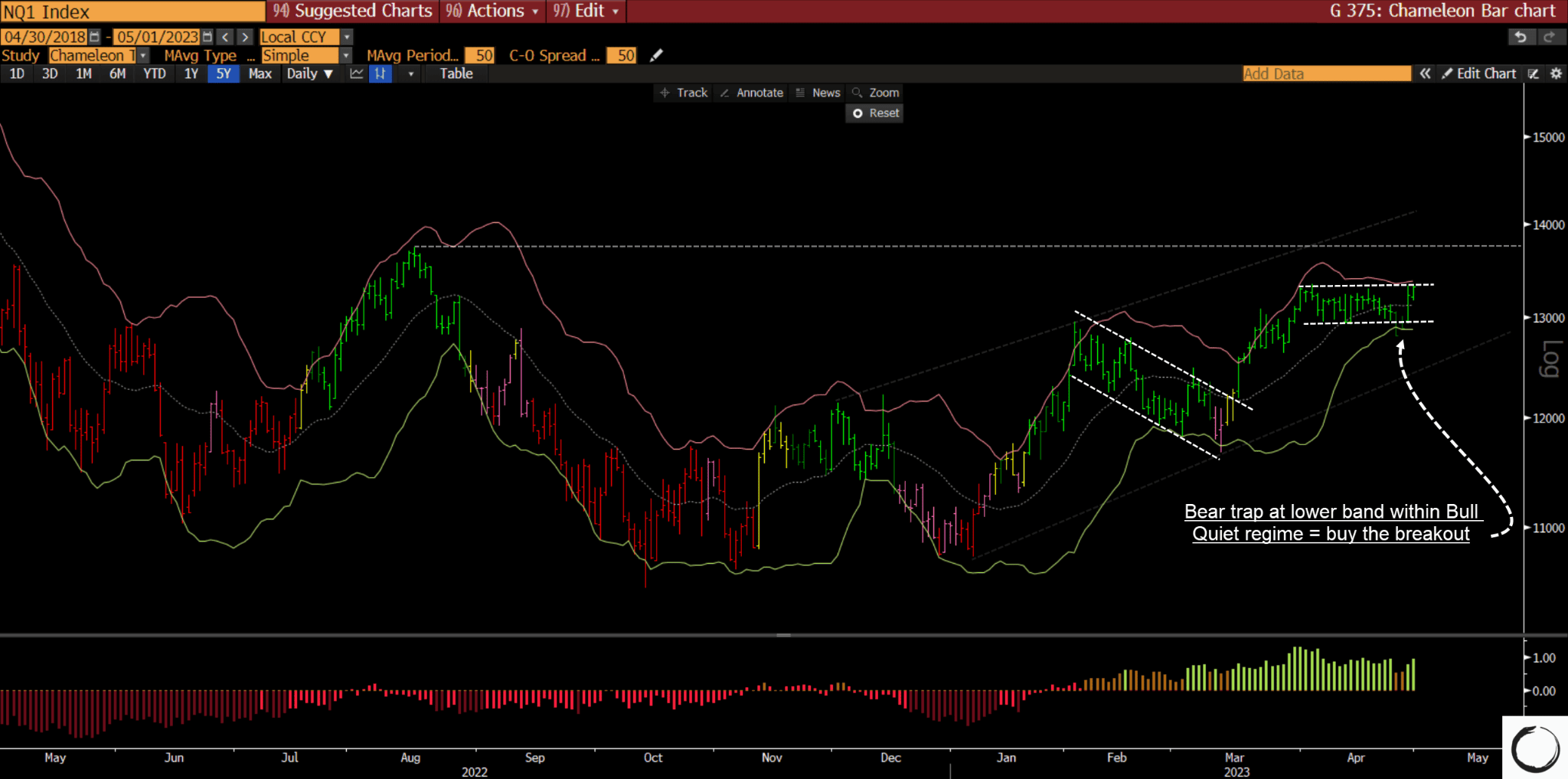

- Market internals present a mixed picture, neither overwhelmingly bearish nor strongly bullish. Semis and cyclical vs defense plus discretionary vs staples are trading weak to neutral while credit and the VIX curve support the uptrend.

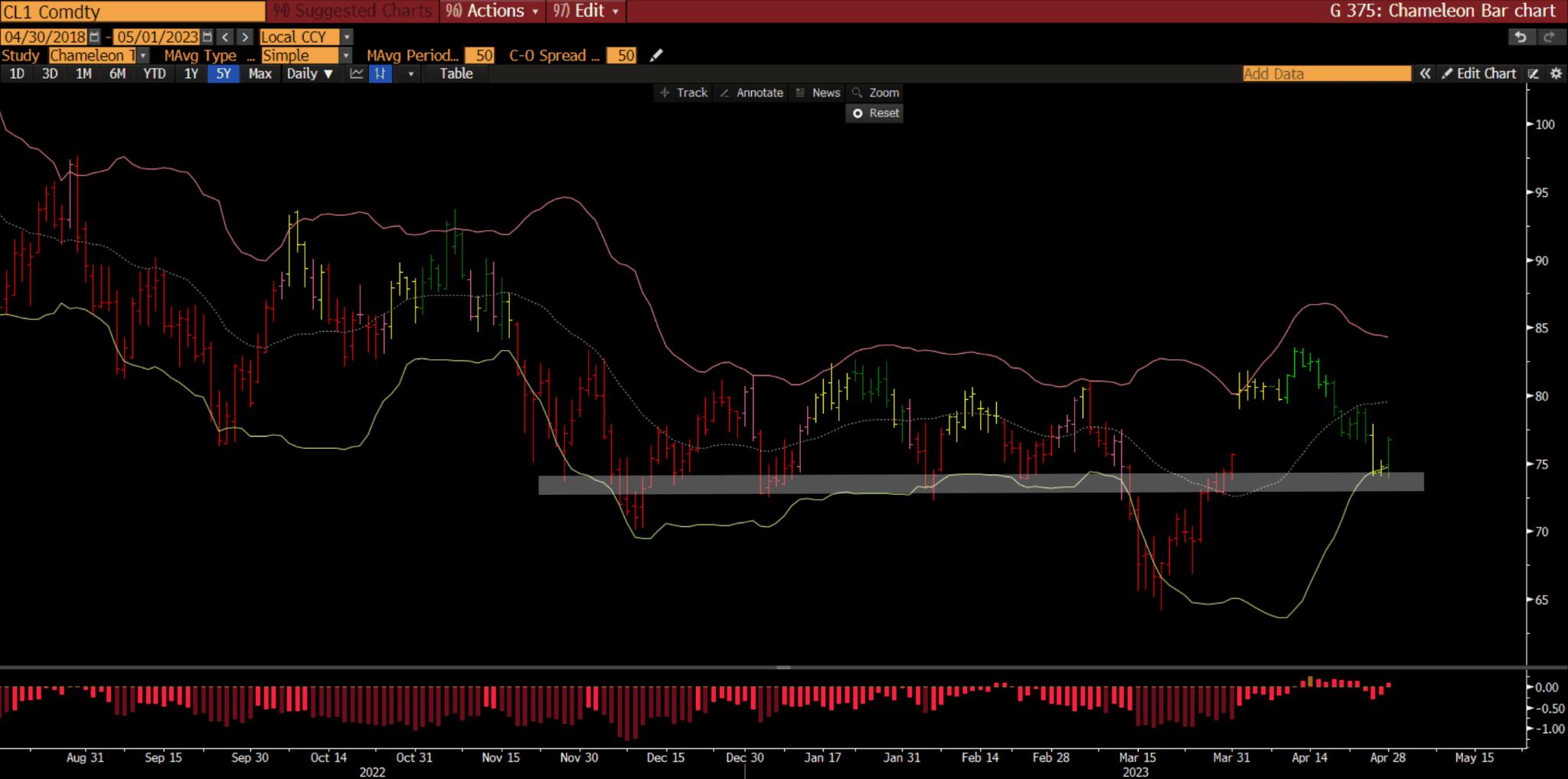

- Here’s a good inflection point in crude to take a stab at getting long. Price is at significant support and has rebounded off its lower Bollinger Band. Positioning is bearish and seasonality is supportive.

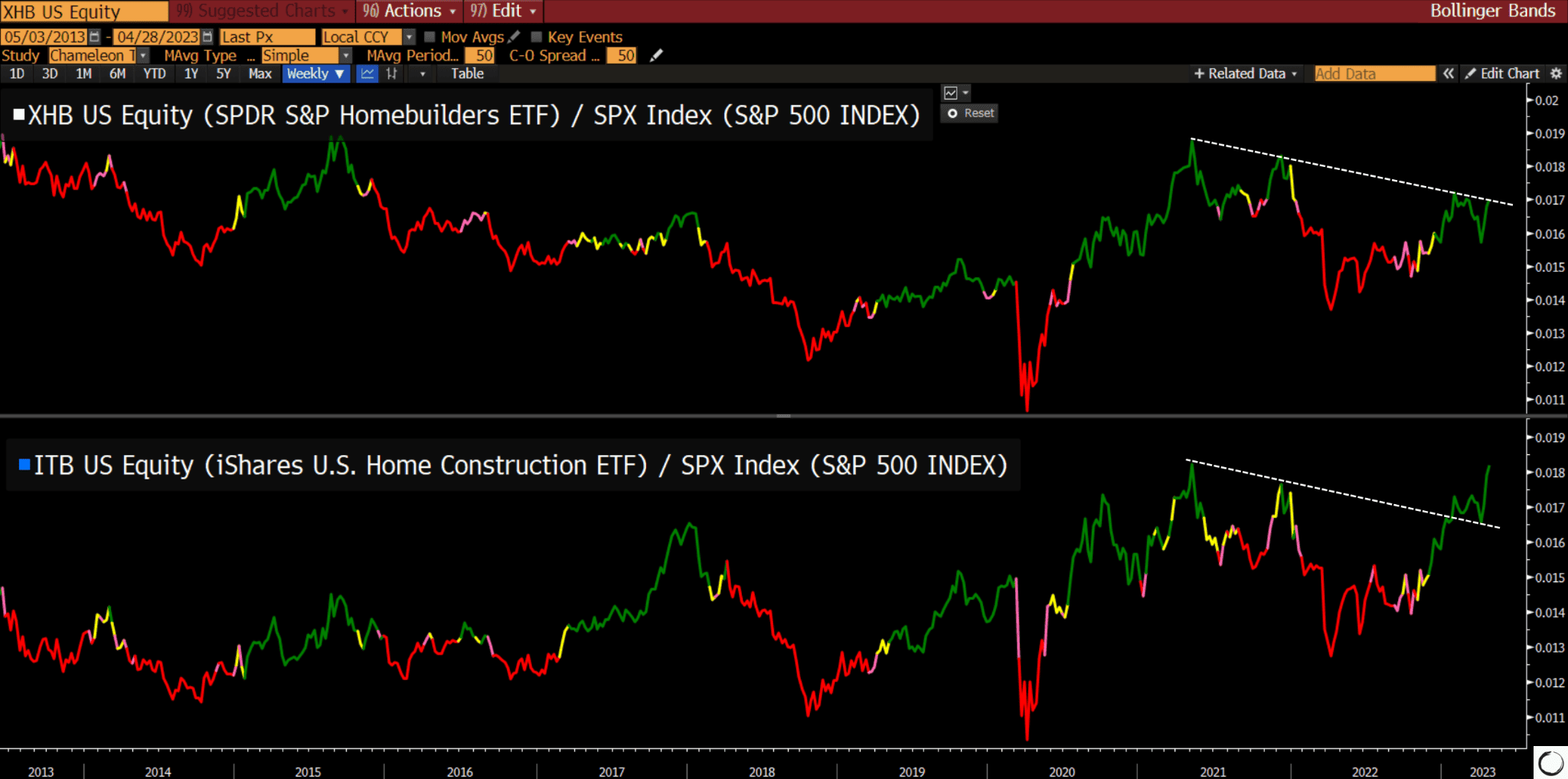

- Homebuilders and home construction is breaking out to new highs relative to the market. This obviously is constructive and a good reason to not fall prey to being overly bearish at this point.

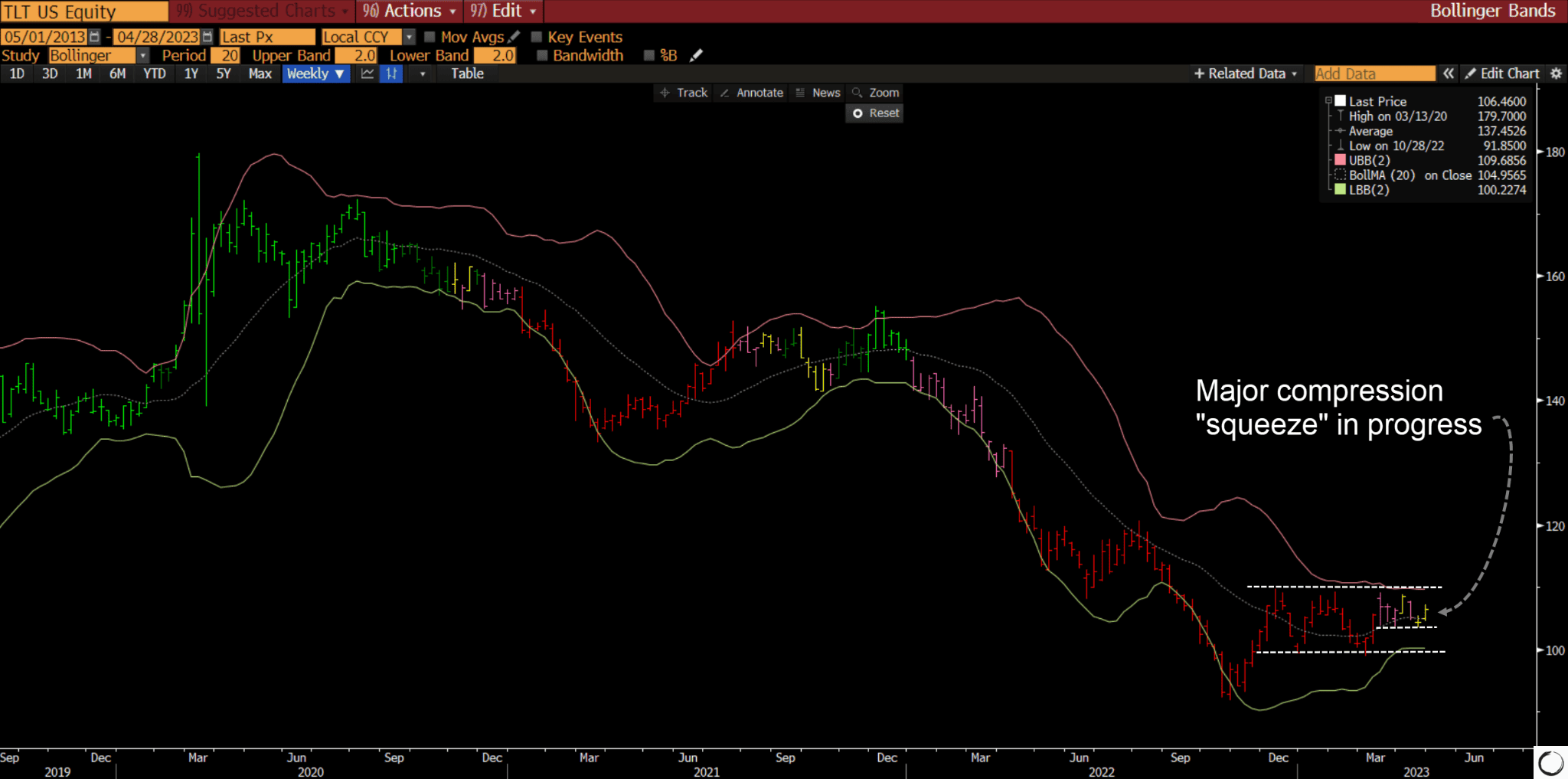

- Bonds are coiling and a big move is coming. Remember, compression regimes lead to expansionary regimes (big trends). Squeezes like this are directionally agnostic but this is worth keeping a close eye on as the rest of the market will key off what happens here (chart of TLT below).

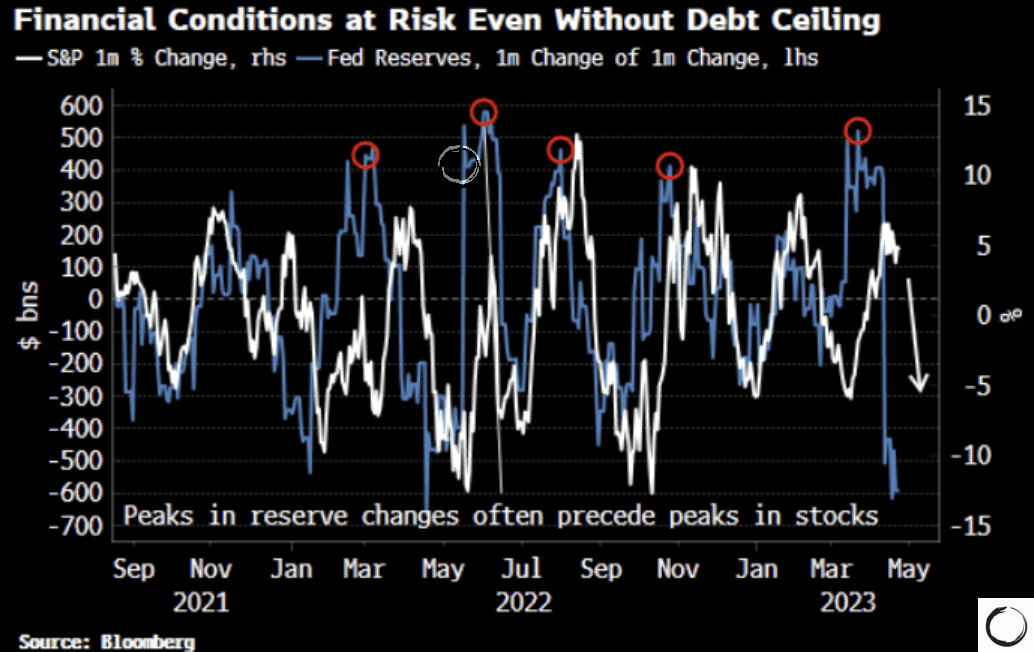

- Here’s an interesting chart from BBG’s Simon White. Simon writes that “Reserves are already very stressed, with their “impulse”, i.e. the change in their change, having just dropped precipitously. This points to weaker equities and tighter financial conditions even without higher-than-expected tax payments.”

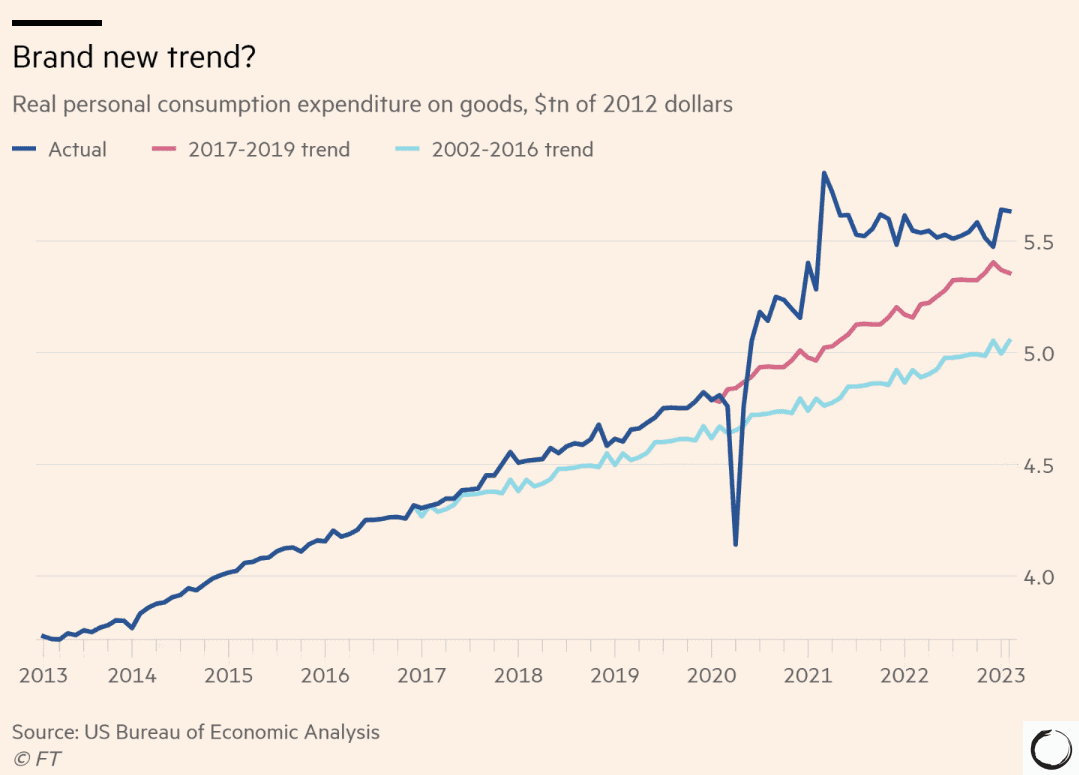

- What if durable goods spending has structurally shifted higher? That’s a question the FT explored in a recent column (link here), writing:

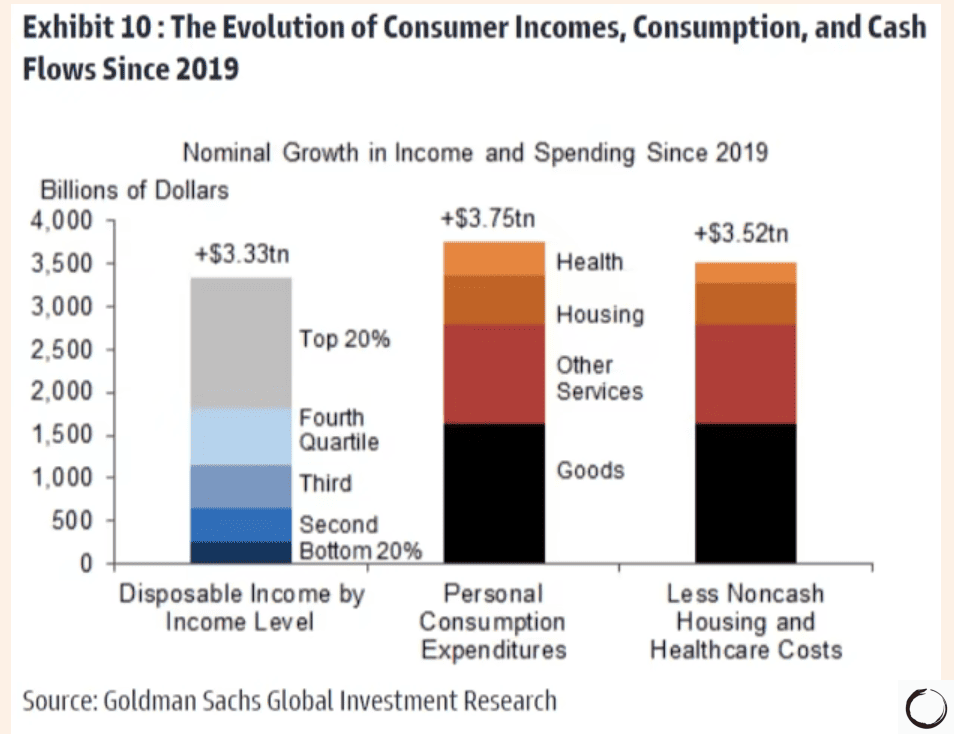

“In a note to clients published on Sunday, Spencer Hill of Goldman Sachs argues that something has changed. “Sustainably stronger consumer finances” have created fresh spending power for people at the bottom of the income distribution. After adjusting for composition effects, Hill estimates that real wage levels for the bottom 50 percent of earners were 6.2 percent higher in the first quarter of this year than in 2019 — and 9.6 percent higher than in 2017. That implies something like $150bn per year in additional spending power for the bottom half. The number rises to $250bn once you throw in other disposable income sources such as social security payments.

“This matters for two reasons: lower-income consumers spend more of each extra dollar earned, and they spend more of each extra dollar earned on goods, specifically. So long as bottom-half consumers have money to spend, goods consumption should stay high.”

- Hill goes on to note that “while the $1.6tn increase in consumer goods spending over three years is enormous in absolute terms, it may indeed be sustainable in the context of the $3.3tn rise in disposable income and the proportionately smaller spending increases for services categories on net. The increase in goods spending also does not look as outsized when one considers the strong disposable income growth of the bottom 3-4 income quintiles — recall that [government] data imply a high marginal propensity to consume goods for lower- and middle-income consumers.”

Meaning, both growth and inflation may be stickier than first thought.

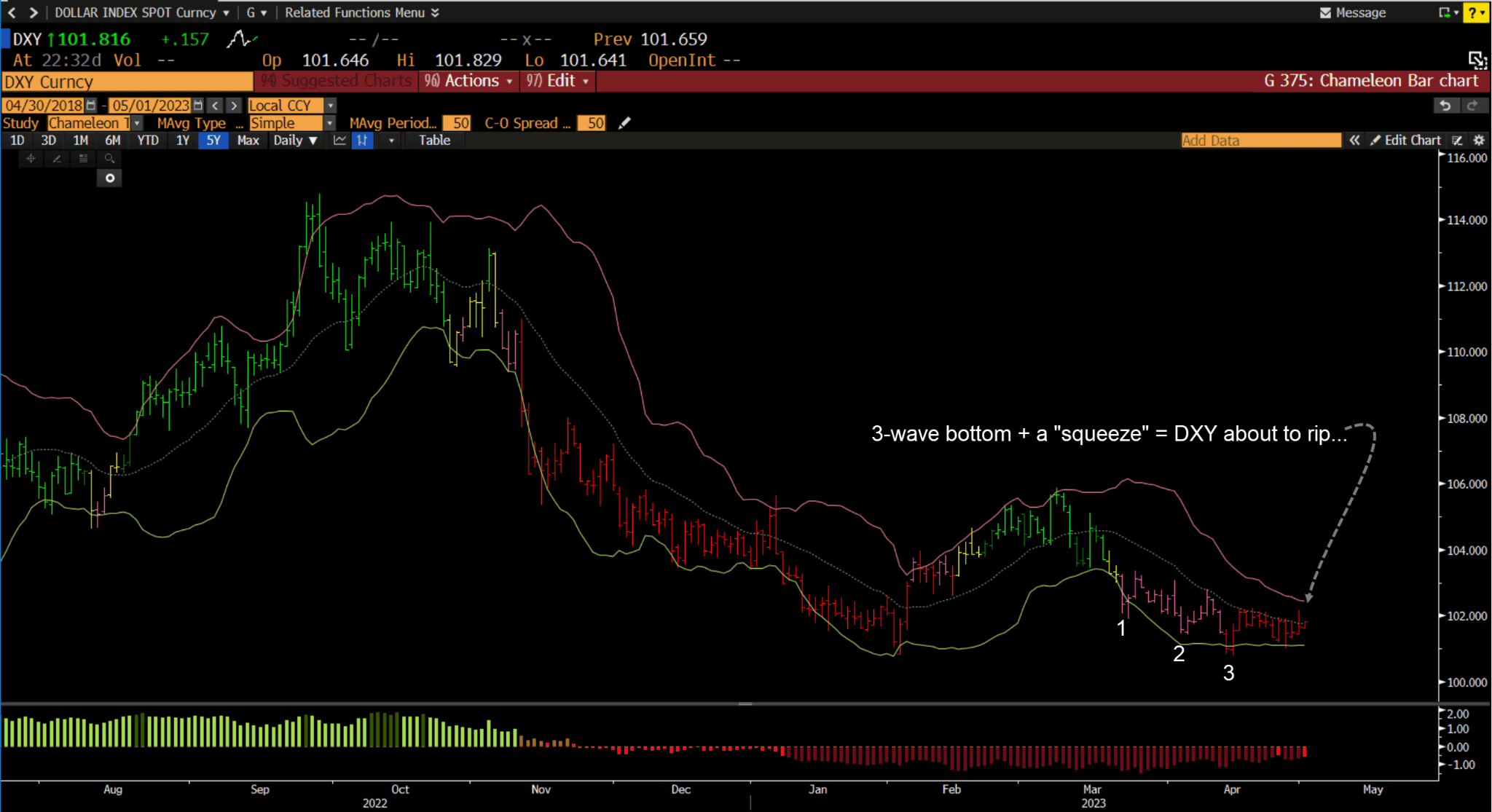

- We’ve been highlighting the bullish setup in the US dollar for the last three weeks. We think it pops and starts running soon. Below we have a compression regime within a 3-wave bottom, along with the background of a popular bearish narrative and crowded positioning.

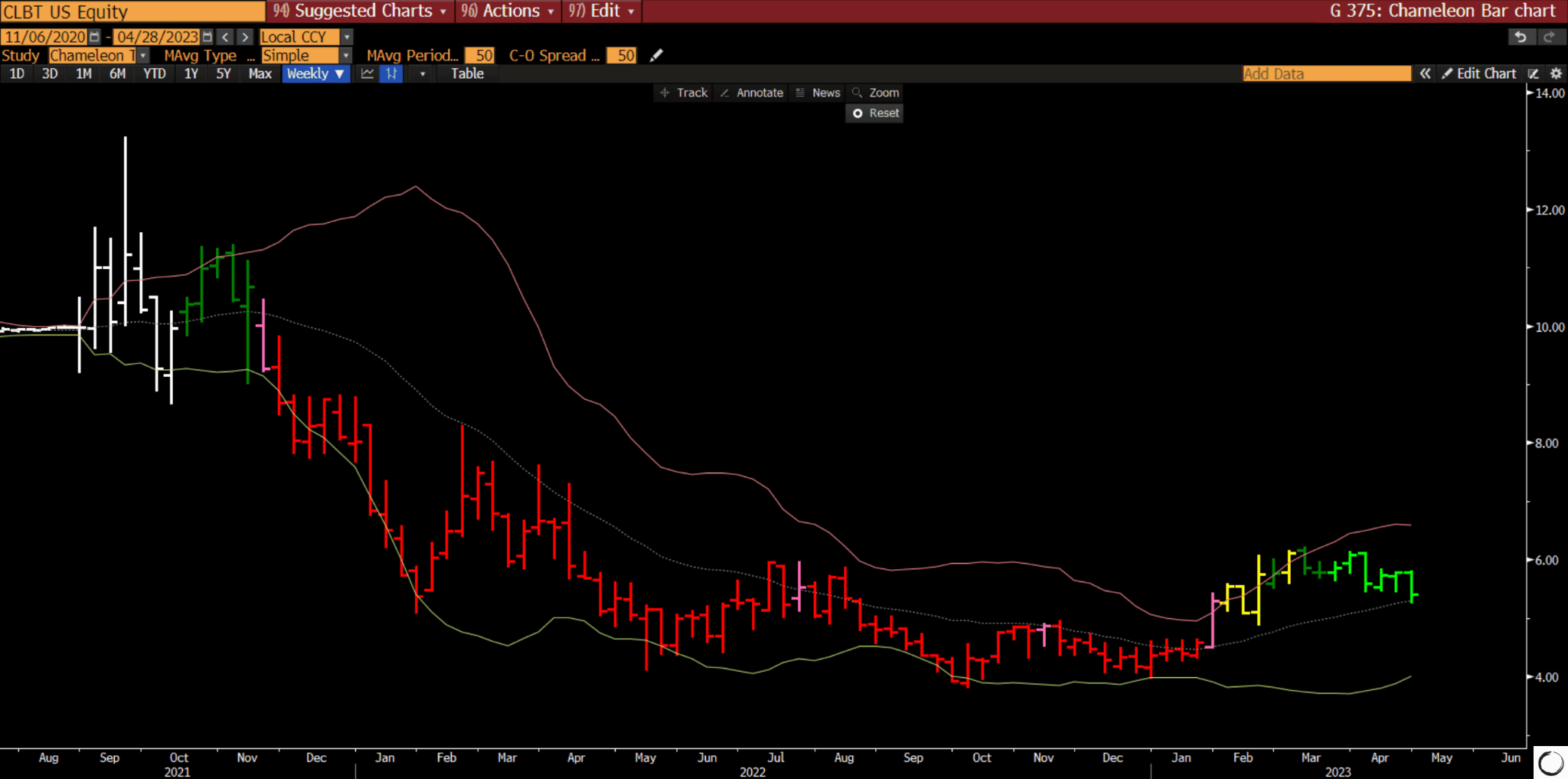

- Scott Miller of Greenhaven Road highlighted Cellebrite (CLBT) in his recent investor letter, writing “Cellebrite is an Israel-based company that came public via a SPAC and is half-owned by a Japanese company. In other words, it has three strikes against it before we even get started. However, Cellebrite has also been a self-funding, rapidly growing technology company since before it was fashionable.

“They have almost $200M in cash and investments, single-digit churn, gross margins north of 80%, and net revenue retention that has consistently been 125% or greater. Their GAAP reported growth has been depressed due to accounting rules for on-premise licenses and their transition from selling perpetual licenses (large up-front payment) to Software as a Service (SaaS).”

Chart below is a weekly.

Thanks for reading.

Stay frosty and keep your head on a swivel.

More By This Author:

EM Stocks Are At Record Cheap Levels

A Generational Buying Opportunity…

The Flow Show…

Disclaimer: All statements are solely opinions and are for educational purposes only.