Fundamentals Start To Catch-Up

Yesterday, the ECB delivered another 0.75% rate hike as expected by the market but the press conference left many traders with the impression that the European Central Bank was turning slightly more dovish. President Lagarde pointed to the risks of recession and highlighted that various indicators pointing downwards according to the FT.

Going into the meeting, the EUR/USD FX pair had moved back above parity but settled below in the hours that followed the press conference.

European Equity indices were largely unchanged over the session with the French CAC losing around 0.5% and the German DAX gaining around 0.1%.

In the US, the NDX continued to struggle dropping another 1.88%, the SPX losing 0.6% and the DJIA finishing higher by 0.6%.

Chinese Equities were slightly resilient with the HSCEI gaining around 0.5% over the day.

Looking at sectors, it will come as no surprise given the above that the Communications segment was the worst performing one over the day losing almost 5% while the Technology sector was lower by slightly more than 1%.

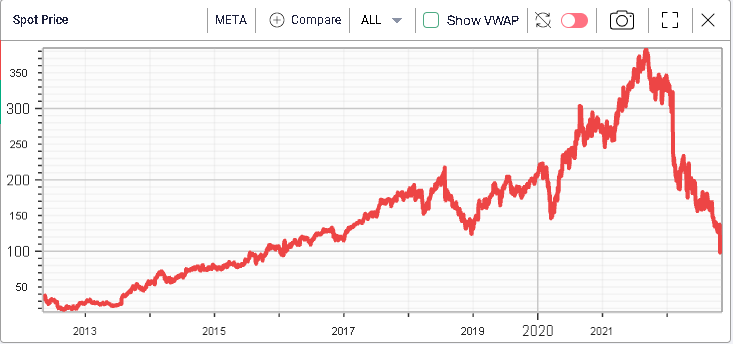

META dropped around 25% yesterday following the release of its earnings. Media reports (BBC) pointed to a slowdown in the advertising market as a source of concern for investors.

The stock is now trading at its lowest level since 2016 as seen on the below screenshot.

Despite that large move, implied volatility struggled over the day and remarked lower as seen on the below 30d IVX chart.

Other communications and tech names struggled as well with GOOG and MSFT losing a further 2% while AAPL finished around 3% lower.

The overall message from some of the largest companies in the US has been fairly concerning. For instance, the FT reported that AAPL’s earnings release was accompanied by some cautionary messages around FX headwinds seen in the form of a strong USD and some continuing supply chain challenges.

These early signals of a slowdown in the guidance and actual earnings of major US companies are important as the market had been expecting a significant growth slowdown over this hiking cycle.

In fact, it is possible that some market participants would view bad earnings from companies and a deterioration of economic indicators as a sign that the Fed might not have to do much more to slow the economy and tame inflation.

One of the most discussed themes over the past few days has been the surprising resilience of US Equity markets in the face of worrying earnings releases by US bellwethers.

For instance, looking at the SHY ETF which tracks 1-3 years US Treasuries, we can see that it has started to move higher over the past few days, a sign that short dated rates have stopped increasing and are even starting to move back lower. 2-year US yields peaked around 4.65% about a week ago and are now trading around 4.36%.

In that context, it will remain important to keep an eye on upcoming macro releases, whether on the inflation front or on the growth front and the next few weeks will give us many occasions to test the market’s reaction around key macro releases.

More By This Author:

Sectors Dislocations Between Europe And The U.S.

CPI Key Reversal

CPI Figures Take Center Stage

Disclaimer: IVolatility.com is not a registered investment adviser and does not offer personalized advice specific to the needs and risk profiles of its readers.Nothing contained in this letter ...

more