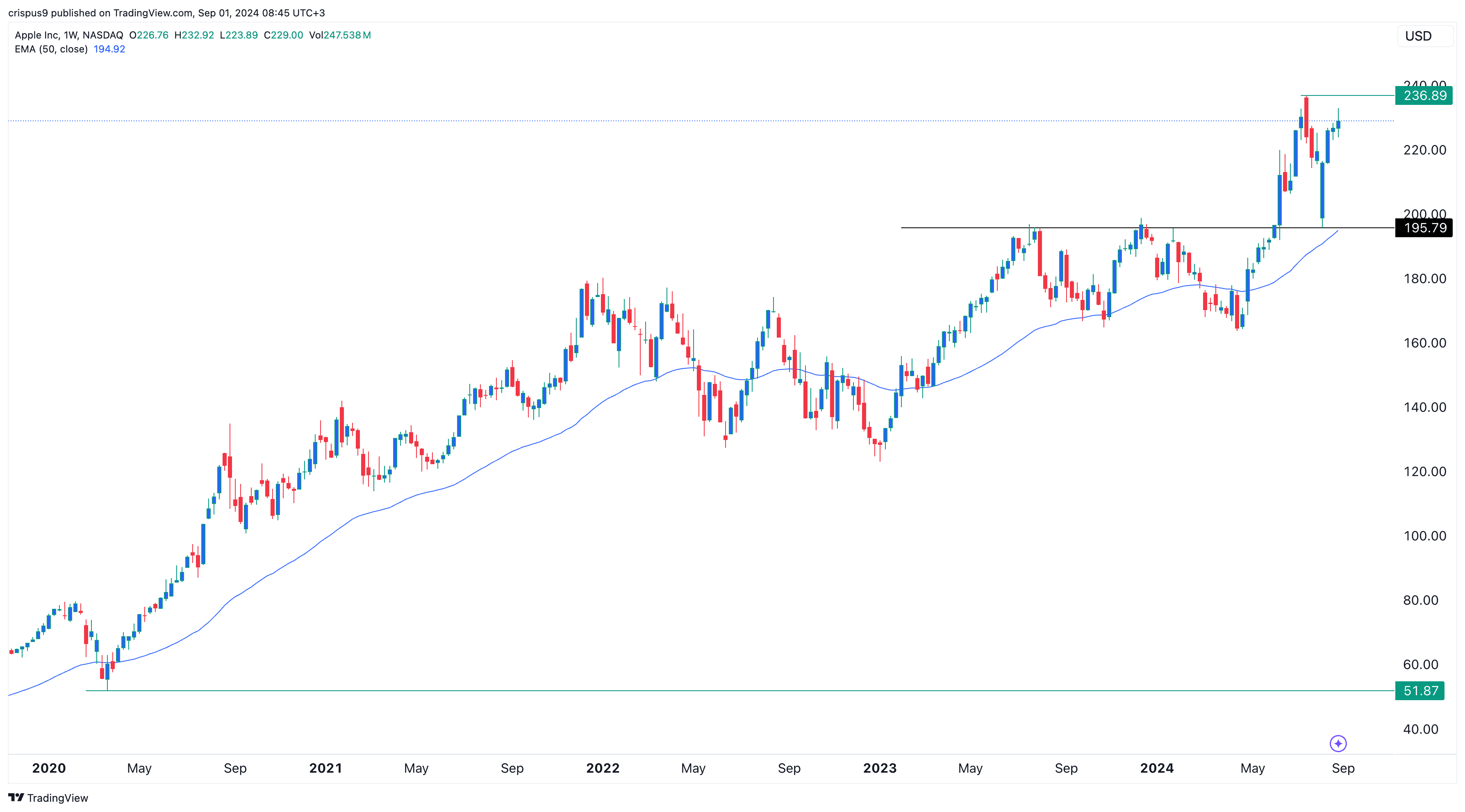

Apple (AAPL) stock price has staged a strong comeback after dropping to $207.23 in August. It has climbed 10.5% from its August lows and is nearing a bull market. Also, the stock has jumped by almost 39% from its lowest point this year, giving it a market cap of over $3.48 trillion.

Apple is under increased pressure

Apple shares have jumped even as the company came under increased pressure lately. Warren Buffett, one of its core shareholders, has dumped most of his stake, taking a big profit.

It has also lagged behind other competitors in the artificial intelligence (AI) industry and is now considering investing in OpenAI, a move that will value the ChatGPT maker at over $100 billion.

Additionally, Apple has struggled to find the next big thing as its iPhone sales slow. Its most recent product was the Vision Pro, which has not become popular. Apple’s crucial services segment is also facing pressure as its revenue growth slows.

Apple will launch its next iPhone on September 9. The latest leaks hint that the iPhone will not be all that different from the ones launched in 2023.

At the same time, its growth has stalled in the past few years. Its revenue rose by just 5% in the last quarter to $85.8 billion while its EPS jumped by 11%.

For the past nine months, Apple’s net profit jumped to $79 billion, making it the most profitable company globally.

Apple’s valuation metrics

To be clear: Apple is one of the best companies in Wall Street. However, its valuation metrics are not adding up well for a company with a market cap of over $3.4 trillion, which explains why Warren Buffett has decided to capitulate.

Looking at its income statement, we see that Apple’s revenue has jumped from over $260 billion in 2018 to over $383 billion last year. Its annual profit moved from over $55 billion to $97 billion in the last financial year. The last profit was down by over $2 billion from what it made in the previous year.

Understandably, Apple’s revenue is not growing as it used to a few years ago. This trend is mostly because people are no longer replacing their iPhones as they used to. Also, the important services segment is facing some growth challenges. Its services revenue rose from $21.2 billion to $24.2 billion.

Apple’s services segment is made up of platforms like App Store, Apple Music, iCloud, Apple TV+, Apple Arcade, Apple News+, and AppleCare. Most of these are highly popular platforms, but I don’t think their growth trajectory is all that strong.

Apple trades at a premium valuation. It has a forward P/E ratio of 34.2, higher than the sector median of 29.35. This valuation is higher than that of Microsoft (MSFT), which has a P/E multiple of 31.60.

Microsoft has multiple tailwinds, including its faster revenue and EBITDA growth of 15% and 26%, respectively. Apple’s forward revenue growth is 2.15% and its forward EBITDA growth is 3.6%.

Apple’s forward P/E of 34 is also higher than the S&P 500’s 21. According to FactSet, the S&P 500 index has an average growth rate of over 10%. It is also slightly lower than Nvidia’s 43. Nvidia’s (NVDA) revenue growth is over 100%.

Therefore, Apple needs to supercharge its growth in the coming years to justify a $3.4 trillion valuation. Remember, $3.4 trillion is a lot of money. For example, it is a figure higher than the GDP of all countries except the US, China, Germany, Japan, India, and the UK.

Apple stock price analysis

The chart above shows that Apple stock has done well after starting off 2019 at just over $39.00. It has now jumped to over $229 and is only $1.50 under its all-time high reached this June.

More By This Author:

JD.com Stock Analysis: JD Might Be A Big Bargain

EUR/USD Forecast: Signal Ahead Of August NFP Jobs Data

Asia-Pacific Markets Rise As US Economic Data Eases Recession Fears

Comments

Log in or sign up to join the conversation.