Today is the last trading day of the second quarter. We came into the week noting that there were few catalysts in the early part but several over the final two days. Now those catalysts are behind us, and those too provided little impetus to sway market trends dramatically.

Yesterday’s GDP report failed to sway markets, as did today’s Core PCE Deflator. The Fed’s preferred inflation measure came in exactly as expected. The deflationary trends continue, but at the same pace that we had already anticipated. University of Michigan Sentiment rose, and Inflationary Expectations fell, but those only caused a relatively minor blip higher in stocks. We’ve previously noted that inflation expectations generally follow gasoline prices. Pump prices fell recently, and so did expectations

University of Michigan 1-Year Inflation Expectations (yellow) vs. AAA National Gasoline Prices (green), since December 2016

(Click on image to enlarge)

Source: Bloomberg

It should be obvious by now that I’ve thus far avoided the elephant in the room (and the donkey, for that matter) – last night’s Presidential debate. There’s no way to spin that as a positive for President Biden, but it’s not clear that markets are particularly banking on a Trump victory right now. I have a very active text group with a bunch of college friends (one of whom was running a focus group at the time), and, noting that US equity futures were modestly higher afterwards, they inevitably asked what I thought the market’s reaction would be. I told them, as I often tell people, that stock traders are notably bad at interpreting geopolitical events that don’t directly affect corporate top and bottom lines in the near term. My comment was to watch the Treasury bond market since they offer a clearer picture about concerns for inflation and the economy. At that time, rates were modestly higher by about 1 basis point. Now we see a bit more of a rise in rates and a slightly steeper curve. That may be attributable to bond market concerns about the former President’s preference for a set tariff hikes and tax cuts that could expand the government deficit. But the bond market has clearly not called the election one way or another.

If today’s gains hold, and since the expiring weekly options have a way of metastasizing Friday gains into something more substantial, they probably will, that will give us five straight days of gains for the S&P 500 (SPX) and four for the Nasdaq 100 (NDX). The Russell 2000 (RTY), which rebalances tonight, had a mixed week though. Interestingly, Nvidia (NVDA), the key stock of the moment, is slightly down for the week right now. Although it quickly recovered its Monday swoon, it has mostly muddled around for the rest of the sessions.

1-Week, NVDA (candles), SPX (yellow), NDX (blue), RTY (purple)

(Click on image to enlarge)

Source: Interactive Brokers

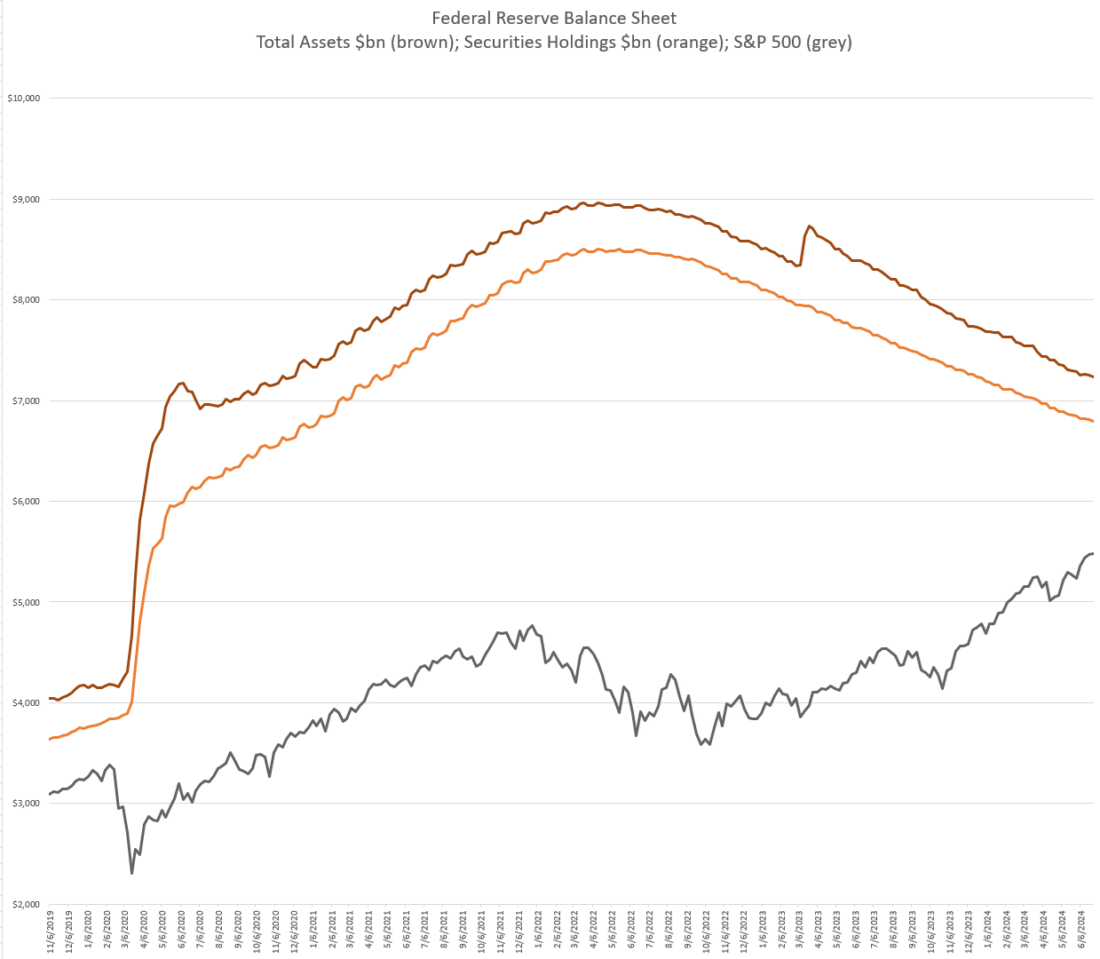

Finally, this seems like a good time to check in with a couple of our old favorite charts. The first compares the size of the Federal Reserve’s securities holdings and balance sheet with SPX. For a while, that relationship really mattered. Now it’s quite evident that equity investors haven’t cared at all about quantitative tightening for over a year. It will be interesting to see if the slower pace of QT will matter:

(Click on image to enlarge)

Sources: Federal Reserve, Interactive Brokers

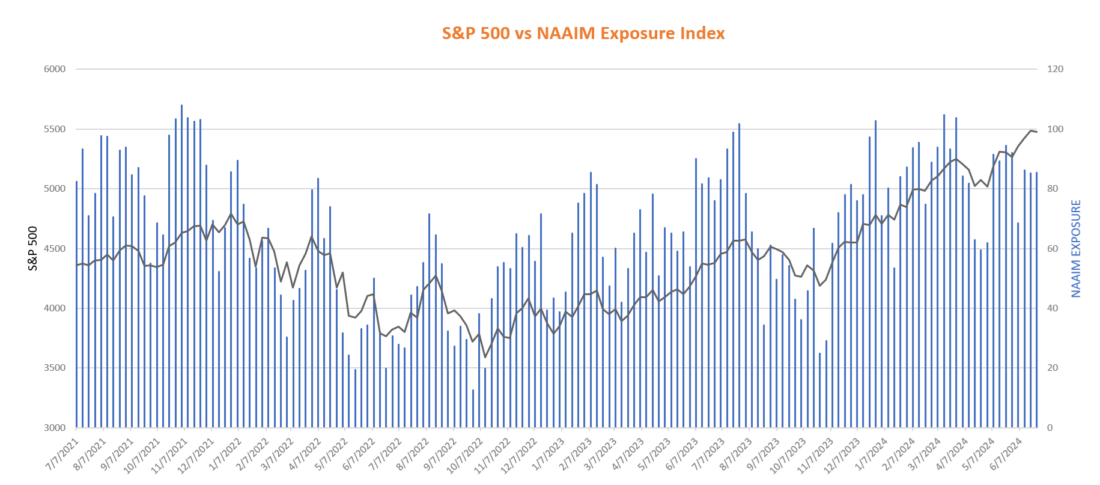

Another favorite chart of mine compares the sentiment readings from the National Association of Active Investment Managers (NAAIM) against SPX. Typically we see sentiment follow the market higher and lower. Of course, it does. When surveyed, investors’ answers tend to reflect what they have already done rather than how they intend to invest. Interestingly, NAAIM sentiment has declined in recent weeks even as SPX ground higher:

(Click on image to enlarge)

Sources: NAAIM, Interactive Brokers

There are some important questions that require answers on the political, monetary and sentiment fronts.But don’t expect too many answers during the holiday-shortened coming week.Instead, the adage “don’t short a dull tape” is more likely to be relevant in the coming days.

More By This Author:

Inflation Worries Resurface, Sending Yields North

Quiet Start Before A Big End To The Week

Stock Market Jenga

Comments

Log in or sign up to join the conversation.