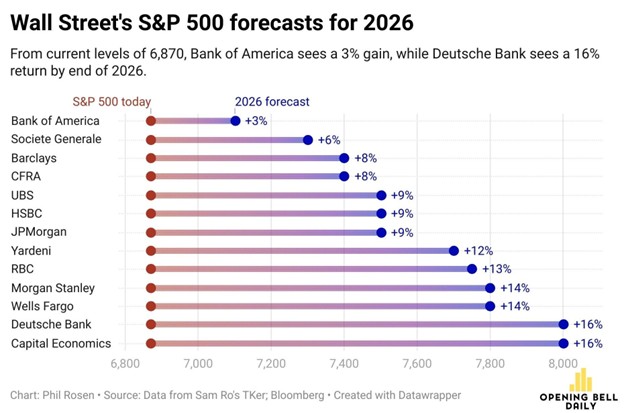

It’s that time of year when every Wall Street analyst posts their forecast for where the S&P 500 will close at the end of 2026. This year, as in every other, Wall Street expects the S&P 500 to post positive returns. As shown below, Bank of America is the most cautious, with a 3% gain, while Deutsche Bank and Capital Economics are the most bullish. On average, the analysts shown below forecast a 10.5% return in 2026, below last year’s 16% but slightly above the longer-term average.

Like Wall Street, we could spitball a 2026 price forecast for the S&P 500, but why? It’s a fruitless endeavor. No one has enough insight into the countless events that will unfold in 2026 and their potential economic, fiscal, and monetary consequences to make a meaningful forecast. Furthermore, even if we had a crystal ball that predicted how the year’s events would unfold, gauging their impact on investor sentiment and, ultimately, on markets would be nearly impossible.

Instead of offering a forecast for 2026, let us consider the potential events and factors that could influence investor sentiment and move markets this year. Inevitably, no matter how many events we and others are considering today, there will be market-moving ones that are not on anyone’s radar currently.

Perspective Matters

Before we focus on potential events in 2026, let’s review historical returns since 1970 to gain perspective.

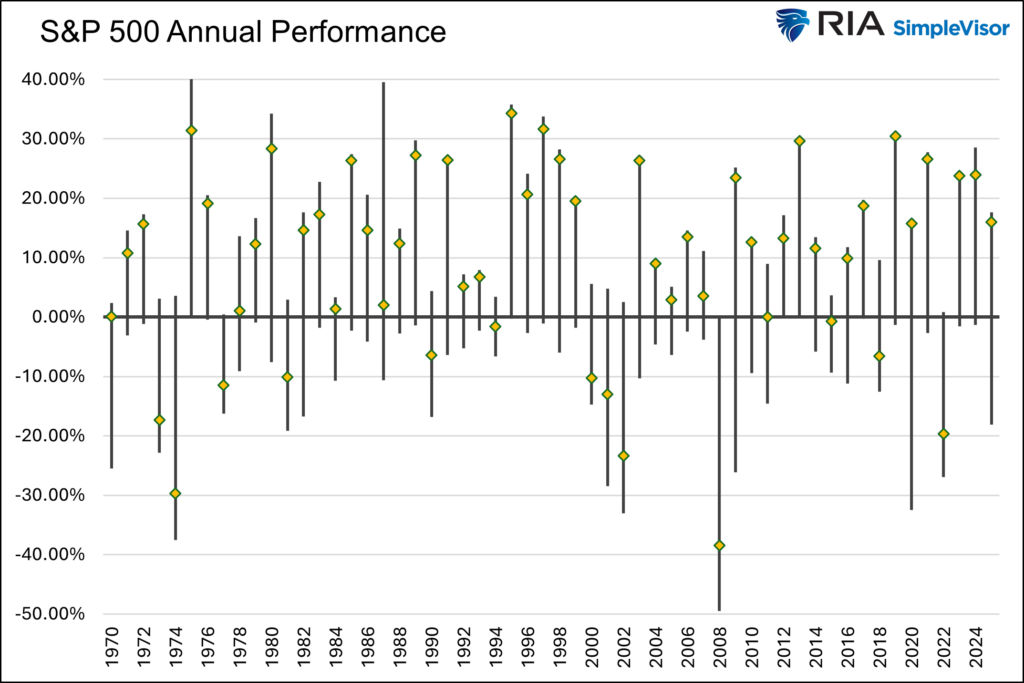

The graph below shows annual returns (gold diamonds) and the range between the minimum and maximum returns for each respective year. The average annual return since 1970 has been 9.43%, with an average yearly drawdown of 11.12%. Moreover, the average annual maximum gain was 16.35%, approximately 7% higher than the average closing price. Thus, the market, on average, closes at the 65th percentile of its range.

(Click on image to enlarge)

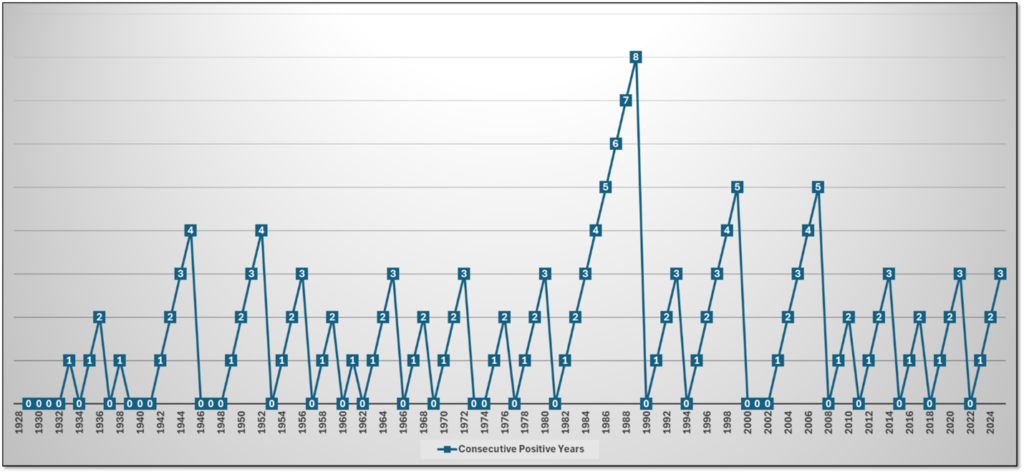

The second graph below is courtesy of one of our clients. His graph helps us assess whether we can expect a fourth consecutive year of positive returns. As shown, eight straight years is the record, with two four- and five-year winning streaks.

(Click on image to enlarge)

The odds are stacked against positive. Since 1928, there have only been five times that a four-year gains streak occurred.

Beware Of Valuations

Valuations are stretched! The first graphic below, courtesy of Goldman Sachs, shows that 12-month forward P/E ratios are significantly elevated globally. The second from Crestmont indicates that the average of four widely used valuation techniques is at a record high.

(Click on image to enlarge)

Current valuations should serve as a constant reminder throughout 2026 to avoid complacency. While caution may be rewarded this year, we must also bear in mind that valuations make poor short-term timing tools.

The first graph below shows the extent to which the CAPE10 valuation at 39 is stretched. Based on historical correlations between valuations and returns, we should expect negative real returns over the next 10 years. However, the second graph indicates that returns of +/- 25% are possible in 2026.

(Click on image to enlarge)

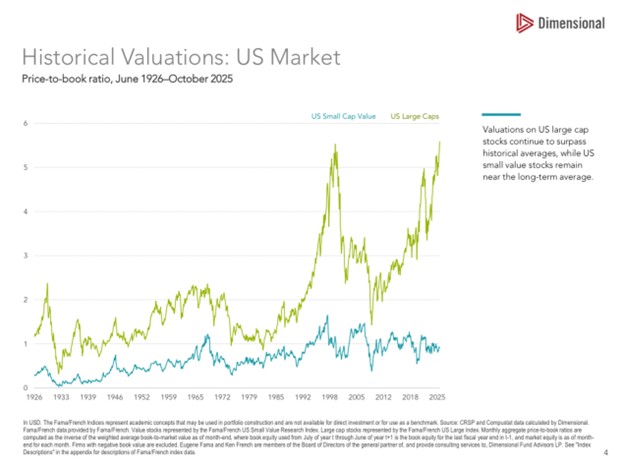

2026 may be the year that valuations normalize, thus resulting in a down year. Even if that is the case, we must recognize that market valuations and those of individual stocks and sectors can differ significantly. Some sectors are less expensive than others and may perform better in a down market. For example, the graph below, courtesy of Dimensional, shows that large-cap price-to-book ratios are at record highs, whereas those for small-cap value companies are at the midpoint of their range over the last 25 years.

Might 2026 be the year where value comes back into vogue, or will valuations, especially for the largest of stocks, get even more extreme?

QE And Liquidity

Last December, the Fed reintroduced QE under the guise of Reserve Management Purchases (RMP). The action is intended to supply the market with liquidity. Per the Fed’s Statement Regarding RMP:

The Desk plans to release the first schedule on December 11, 2025, with a total amount of RMPs of approximately $40 billion in Treasury bills; purchases will start on December 12, 2025. The Desk anticipates that the pace of RMPs will remain elevated for a few months to offset expected large increases in non-reserve liabilities in April. After that, the pace of total purchases will likely be significantly reduced in line with expected seasonal patterns in Federal Reserve liabilities.

Simply put, liquidity in the banking system was becoming scarce as reserves declined. To avoid worsening liquidity conditions, the Federal Reserve is injecting reserves into the banking system.

The question for investors is whether the $40 billion in monthly reserves, intended to last “a few months,” is sufficient to offset the expected decline in liquidity over that period.

If it’s not, then the markets may come under pressure as liquidity wanes.

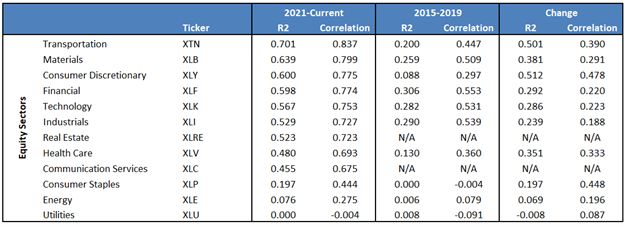

Conversely, if you think the Federal Reserve’s actions will boost reserves meaningfully, our article “QE Is Back” may offer a practical trading blueprint for the first few months of 2026. The article identifies which stock market indexes, sectors, and factors are strongly correlated with bank reserves. The table below, from the article, indicates that transportation, materials, consumer-discretionary, financial, and technology stocks could benefit most from a reserve increase. Conversely, the utilities, energy, and staple sectors offer little correlation.

Will QE once again prove to be a driving force for the stock market?

Powell Exits

Jerome Powell’s term as Fed Chair ends in May 2026, and Trump’s appointment of a new Chair is being closely watched. The new Chair’s stance on the trade-offs between inflation and labor-market weakness could significantly alter investor sentiment.

The two front-runners for Powell’s chair are Kevin Warsh and Kevin Hassett. We compared the two potential nominees in our Daily Commentary on December 17th–

Warsh is viewed as more hawkish than Hassett. He has frequently mentioned the inflation risk associated with dovish monetary policy. Moreover, as we noted above, he has expressed skepticism about aggressive QE. Conversely, Hassett, viewed as dovish, actively advocates deeper rate cuts to stimulate growth.

Kevin Warsh adheres to a Milton Friedman-style logic: inflation is a function of excessive money-supply growth. Based on recent speeches, Hassett is focused on growth-oriented easing and is not overly concerned with inflation.

Hassett likely appeals more to President Trump because of his dovish views. However, Kevin Warsh lends greater credibility to the Federal Reserve’s promise to reduce inflation. Additionally, Warsh is more likely to improve sentiment in the bond market, thereby lowering long-term yields.

Initially, the bond market is likely to be more affected than the stock market by President Trump’s decision regarding the next Federal Reserve chair. However, said changes in interest rates could readily impact the stock market.

To assess potential market reaction, we should monitor changes in inflation expectations. As noted below, 1-year inflation expectations are falling rapidly, despite the more dovish Kevin Hassett expected to replace Powell. Thus, at the moment, the market is not expressing concerns about a dovish Fed Chair.

Will it be the dovish Kevin Hassett or the hawkish Kevin Warsh running the Federal Reserve in 2026?

Midterm Elections and Fiscal Policy

The November midterm elections will determine the balance of power in the U.S. Congress. As shown below, the Polymarket betting site assigns a 79% probability to the Democrats taking control of the House and a 66% chance that the Republicans will maintain Senate leadership.

If one or both houses of Congress change hands, the administration will find it much more challenging to pursue its domestic and foreign policy objectives. From a market perspective, this may limit the President’s ability to manage fiscal spending and further change the tax code. Accordingly, changes in Congressional power and budgetary implications could significantly affect growth and inflation, as well as individual stocks and sectors.

As the year progresses, investors will likely pay closer attention to the betting markets and traditional polls for insight into the midterm elections.

While investors wait for the elections, it is worth noting that Americans will get a “gigantic” tax refund next year. The tax provisions in the Big Beautiful Bill should, in practice, result in larger-than-normal refunds this year. Per Treasury Secretary Scott Bessent via FoxBusiness:

I can see that we’re gonna have a gigantic refund year in the first quarter because working Americans did not change their withholdings,” Bessent told the “All-In Podcast” hosts. “I think households could see, depending on the number of workers, $1,000- $2,000 refunds.”

The AI Infrastructure Boom and Productivity Gains

The massive capital expenditure (CapEx) cycle for AI infrastructure, including data centers, the power grid, and supercomputing, is expected to continue into 2026 and beyond. As we saw in 2025, the spending will boost GDP growth and profits for many companies involved. However, toward the end of 2025, investors began to question whether some companies were spending and borrowing more than they would ever recoup.

We pose a few questions to help you consider what 2026 may bring.

- Will the AI-led bull market continue to charge ahead like last year on the belief and hope that massive CapEx spending will translate into enormous profits?

- Will the rapidly growing debt requirements needed to fund CapEx be a drag on the market?

- Given that technological change is occurring rapidly, might there be a new development to shake up the AI industry? Think about Deep Seek roiling the market last January.

- Might investors start to question whether the productivity benefits of AI are worth the cost?

- Is AI in a bubble like the dotcom bubble? If so, will 2026 be the year it surges, as in 1999, or the year it peaks, as in 2000?

Tariffs and Trade

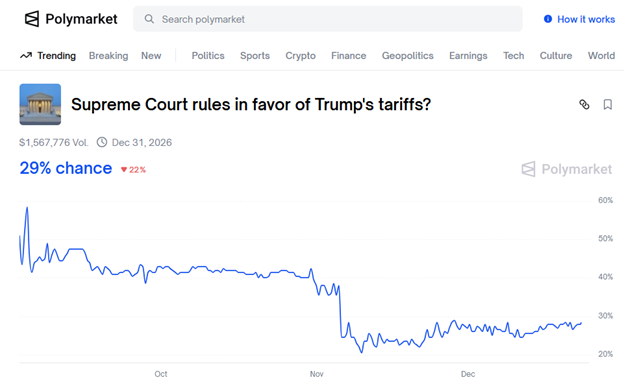

The Supreme Court has heard oral arguments in the tariff legality case and will announce its findings on January 9, 2026. According to Polymarket, the odds of a favorable ruling for Donald Trump are low at 29%.

If the Supreme Court strikes down the tariffs, the economic impact could be substantial. To begin with, the prices of some goods that are no longer subject to tariffs may fall, and trade flows will adjust accordingly.

However, it’s not wise to go down that road too far. The President reportedly has a Plan B ready. Tariffs or some other similar measure will most certainly be implemented if the Supreme Court rules against tariffs. But these measures may also be subject to judicial review.

Whatever the final trade policy is, there will be supply chain realignments that could significantly affect import costs, profit margins, and global trade patterns.

The question is not the Supreme Court ruling itself, but the mechanism the administration will ultimately use to implement tariffs, taxes, or trade restrictions. Moreover, we should consider how investors will handle a period of uncertainty.

Miscellaneous

Geopolitical Hotspots: Ongoing conflicts and tensions in Ukraine, Venezuela, and the Middle East, along with increased provocations between the US, China, Iran, and Russia, pose persistent headline risks. Many of these tensions can cause sudden changes in energy prices and economic activity, and disrupt supply chains and consumer sentiment.

Debt Levels and Sovereign Risk: 2025 began with higher bond yields, driven by the “bond vigilantes” and their grave concerns about the U.S. fiscal situation.With the U.S. government continuing to run massive fiscal deficits, the ability to finance these debts and manage interest costs will remain a concern. Renewed signs of bond market stress or investor concerns about a government’s ability to meet its debt obligations could trigger significant volatility, particularly in the U.S. Treasury market. Such volatility would quickly filter through to the stock markets. Will the bond vigilantes regain their voice?

Bear in mind, there is a risk of another government shutdown by the end of the month.

Monetary Policy: The ECB is considering raising interest rates. Might we find that the Fed reaches a similar conclusion later in 2026? Or might rates and inflation be heading much lower? As shown below, the Fed Funds futures market forecasts only one rate cut in 2026. The Fed has enough trouble predicting the next three to six months; what makes anyone think Wall Street is any better?

Yen Carry Trade: A depreciating yen strengthens the carry trade, supporting many US financial assets. At the same time, a depreciating yen heightens affordability issues and the popularity of its political leaders. This is primarily because Japan is heavily dependent on imports of energy and raw materials, whose prices rise when the yen depreciates.

Given domestic economic and political pressures, along with US persuasion, we expect the Japanese government to take steps to strengthen the yen. If any upward adjustment is done gradually, the impact on financial markets should be minimal. However, if it occurs suddenly, such as in August 2024, financial market volatility could spike.

Summary

There are 14 questions in this article, and we could easily have doubled or tripled that number. There are far more questions than answers about what the new year may hold. More importantly, there will be additional events that are not known today.

Thus, instead of forecasting where the S&P will close in 2026 with zero confidence, we would rather take the market and news as they come. We suspect that QE will provide initial support to the market through the winter. Valuations should keep us on guard throughout the year. Many of the other items we discuss pose a constant risk and or the potential for better returns throughout the year.

As you consider your forecast for 2026, we leave you with a thought to ponder from Arthur Zeikel:

Most investors tend to cling to the course to which they are currently committed, especially at turning points.

More By This Author:

Venezuela Leads Energy Stocks Out Of The Gate In 2026

Silver Mania And The Predictable Bust

QE Is Back: Which Assets Benefit From The Liquidity Boost

Comments

Log in or sign up to join the conversation.