Forecast Earnings

In this video, Chuck Carnevale, co-founder of FAST Graphs, takes a deep dive into what he calls the single most important factor for long-term investing success: the ability to forecast future earnings growth. While past performance matters, it’s really what lies ahead that determines whether a stock will generate wealth or disappointment. Through detailed examples, Chuck demonstrates why valuation, earnings, and cash flow are inseparable from forecasting, and why investors who master this discipline will always have an edge.

Why Forecasting Matters

Chuck begins by stressing a foundational truth: in the long run, earnings and cash flow dictate stock prices and dividend income. Over short stretches, markets swing based on emotion, fear, or excitement. But sooner or later, price aligns with business performance. This makes forecasting—not guesswork, but disciplined analysis—the key to successful investing.

He also addresses a common criticism: analyst estimates aren’t perfect. That’s true, he admits, but dismissing them entirely is misguided. Forecasts collected by FactSet come from over 800 professional analysts at major firms like Goldman Sachs, Morgan Stanley, UBS, Credit Suisse, and others. These analysts are trained professionals who study company guidance, balance sheets, and industry trends. While not flawless, their consensus estimates provide a reliable starting point. FAST Graphs allows investors to test those forecasts against history, evaluate margins of error, and run their own scenarios.

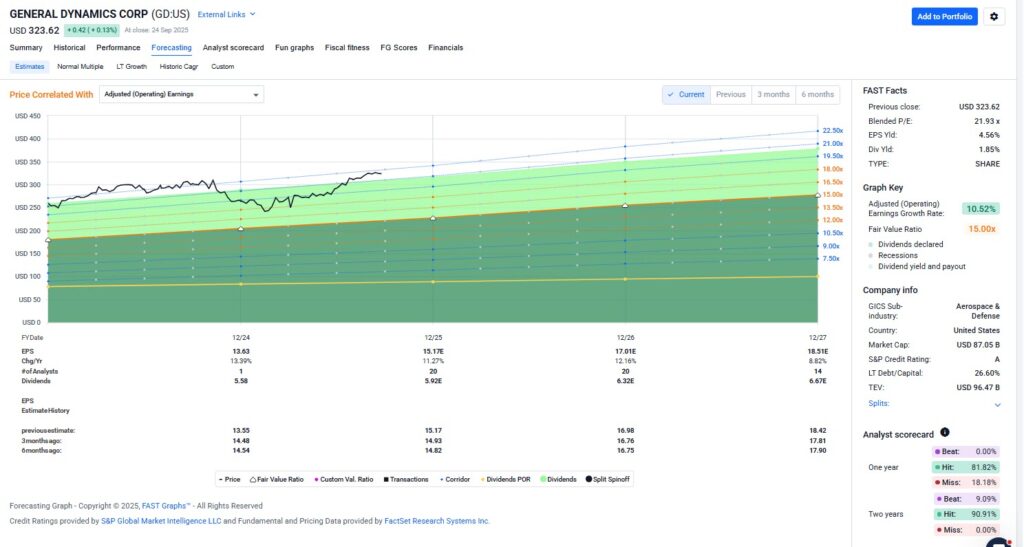

Case Study 1: General Dynamics (GD)

The first company Chuck examines is General Dynamics, a defense contractor with a long track record of solid earnings growth. FAST Graphs shows its historical earnings in orange, with dotted lines pointing to analyst forecasts. The stock’s price has generally followed its earnings trajectory, but valuation swings in both directions are clear.

During times of overvaluation, prices eventually reverted back toward earnings. The same happened during undervaluation periods. Chuck paraphrases Warren Buffett’s wisdom: “I can’t tell you when, but I can tell you with certainty that price will return to intrinsic value.”

Right now, GD trades at a P/E above 21, with an earnings yield below 4.5%. For Chuck, that’s unattractive—well under the 6.5–7% threshold he prefers. Even if forecasts are accurate, the valuation makes the stock unappealing. “Why waste time forecasting,” he asks, “if the stock is already too expensive?”

Although he’s owned and profited from GD in the past, he views it as overvalued today and not research-worthy at current prices. This illustrates an important lesson: great businesses aren’t always great investments if you overpay.

Case Study 2: Global Payments (GPN)

In contrast, Chuck highlights Global Payments (GPN) as a company where forecasting becomes not only worthwhile but essential.

Historically, GPN’s price closely tracked earnings, though it experienced stretches of overvaluation and eventual correction. In the 2012–2021 period, a $10,000 investment grew eightfold. But the stock later collapsed as valuations fell, despite continued earnings strength.

Today, FAST Graphs suggests intrinsic value near $180–$189 per share, while the market price hovers around $86—a massive discount. Analysts project 12%+ earnings growth going forward. To Chuck, this signals opportunity.

(Click on image to enlarge)

Analyst Scorecard: Testing Forecast Reliability

Skeptics often claim forecasts can’t be trusted, but Chuck points to FAST Graphs’ analyst scorecard. Looking back, one-year forecasts were generally within a 9% margin of error. Two-year forecasts, when judged with a 20% tolerance, were remarkably accurate.

For GPN specifically, analysts have shown a strong track record of forecasting reasonably well. That doesn’t mean perfection, but as Buffett famously said, “It’s better to be approximately right than precisely wrong.” With GPN, the evidence suggests forecasts are dependable enough to form the basis of rational decision-making.

Digging Into Fundamentals

Forecasting isn’t only about projecting numbers—it requires digging into the underlying fundamentals. Chuck examines GPN’s business and financials:

- Revenue: Over $10 billion annually, consistent growth even through industry shifts.

- Margins: Gross margins above 60%, operating margins around 22%, and improving net margins (15% in 2024 vs 10% in 2023).

- Cash Flow: Strong free cash flow supports dividends and debt reduction.

- Balance Sheet: Nearly $3 billion in cash and manageable leverage.

- Profitability Ratios: Returns on assets, equity, and invested capital declined for a period but are now improving—another positive sign.

When compared with peers like Visa and Mastercard, GPN trades at a fraction of their multiples. Visa, for instance, commands a blended P/E near 29; GPN trades closer to 7. For a business with strong growth prospects and industry tailwinds, Chuck sees this as a case of mispricing.

Growth Drivers and Opportunities

Chuck outlines several reasons why GPN’s future looks promising:

- Digital Payments Boom – E-commerce, mobile, and contactless payments are expanding rapidly, fueling transaction growth.

- Worldpay Acquisition – A transformative deal that broadens scale and market reach, despite near-term integration risks.

- Cost Savings Program – A $650 million efficiency initiative designed to boost margins.

- Technology Innovation – Investments in AI and new platforms like Genesis to enhance fraud detection and streamline operations.

- International Expansion – Growth in under-penetrated markets across Europe and Asia-Pacific.

- Industry Tailwinds – The payment processing market is projected to grow at double-digit rates, reaching over $147 billion by 2032.

Despite its smaller market share (about 6.7% compared to Visa’s 26% and Mastercard’s 21%), GPN differentiates itself through integrated merchant solutions and diversified revenue streams.

Risks and Market Perception

No investment is risk-free, and Chuck doesn’t ignore the negatives. GPN faces challenges such as:

- Integration risks with Worldpay.

- Regulatory pressures and compliance costs.

- Competition from fintech disruptors and established giants.

- Security and fraud prevention challenges.

Still, Chuck believes these risks are already priced into the stock. Investor fear has created a wide margin of safety. Even if growth slows, valuation is so low that upside potential remains significant.

Valuation and Scenarios

FAST Graphs allows investors to test different assumptions. If GPN grows earnings at 12% and reverts to a P/E of 15, annualized returns could exceed 50%. Even under more conservative assumptions (8% growth, lower multiples), the returns remain attractive.

Chuck stresses that the key isn’t predicting perfectly but weighing risk versus reward. With GPN, the potential reward far outweighs the risks at current prices.

Lessons for Investors

The video closes with several timeless takeaways:

- Forecasting is essential: Investing without a forward view is gambling.

- Valuation matters: Great companies can be poor investments if overvalued, and mediocre companies can be great investments if undervalued.

- Analyst estimates are useful starting points: Not flawless, but reliable enough when combined with independent research.

- Patience pays: Stocks can remain undervalued or overvalued for years, but eventually earnings dictate price.

- Margin of safety is critical: Buying undervalued companies reduces risk and increases potential reward.

General Dynamics shows why even strong businesses aren’t worth chasing at high valuations. Global Payments illustrates how market pessimism can create opportunities for disciplined investors.

Final Thoughts

Chuck reminds viewers that the only certainty about the future is its uncertainty. That’s why continuous monitoring is required. If fundamentals deteriorate, forecasts must be adjusted. But as things stand, GPN represents a classic case of a high-quality company trading at a deep discount.

He ends with encouragement to investors: use tools like FAST Graphs to cut through the noise, focus on earnings and valuation, and remember that patience is the investor’s best friend.

“Forecasting is not optional—it’s the key to investing success.”

Video Length: 00:37:48

More By This Author:

Dissecting The S&P 500 – Should You Invest?

Can Managed-Healthcare Stocks Prescribe A Cure For Their Ailing Earnings?

Why Buying Overvalued Stocks Is Risky: Invest Smart, Buy Low Instead

Comments

Log in or sign up to join the conversation.