Indices are poised to hit new highs, but market activity slowed on Wednesday despite additional positive Q1 earnings reports.

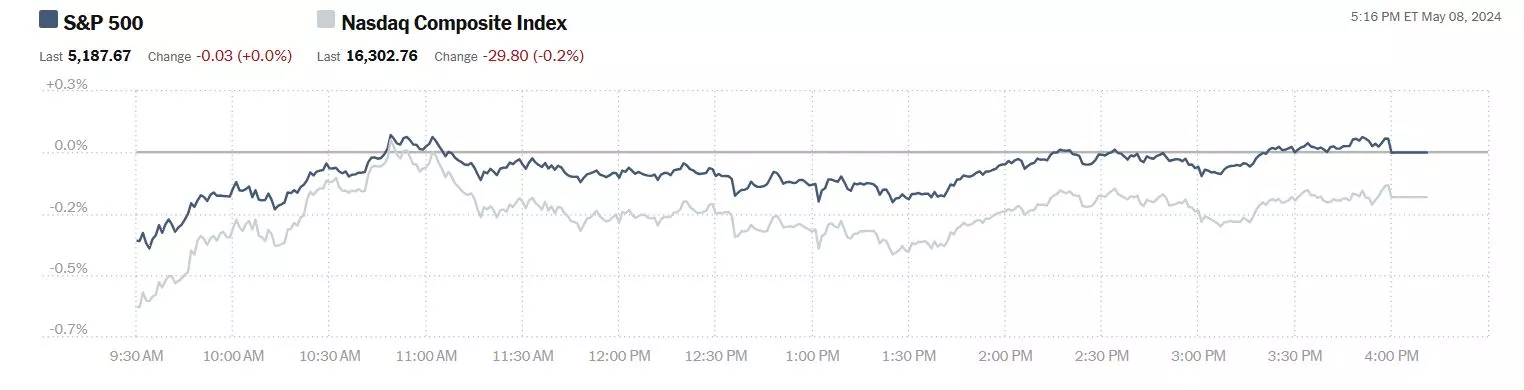

Yesterday the S&P 500 was unchanged at 5,188 points, the Dow closed up 172 points at 39,056 and the Nasdaq Composite closed at 16,303, down 30 points.

Chart: The New York Times

Most actives were led by Uber (UBER), down 5.7% followed by Tesla (TSLA), down 1.7% and Intel (INTC). down 2.2%.

Chart: The New York Times

In morning futures S&P 500 market futures are down 14 points, Dow market futures are down 91 points and Nasdaq 100 market futures are down 62 points.

TalkMarkets contributor Patrick Munnelly gives us his Daily Market Outlook For Thursday, May 9.

"The Asia-Pacific equity markets are showing mixed performance today. China's trade surplus for April increased by less than anticipated, mainly due to a notable rise in imports. Asian bond prices fell, following the sell-off in US Treasuries. Chinese stocks increased due to positive trade data and indications of property market support. Benchmark rates in Japan rose, while US government bond rates also increased after a lukewarm response to a $42 billion offer of 10-year notes. Japanese rates went up after the central bank made a hawkish statement about its April meeting, discussing the potential reduction of bond purchases and the path for future rate hikes.

In the UK, the most recent RECS survey on the labor market indicates a continued decline in both recruitment activity and unfilled vacancies, although the rate of decrease appears to be slowing down. The Bank of England is widely expected to maintain its policy interest rates at 5.25% for the sixth consecutive meeting in today's update. However, the focus lies on the signals regarding potential future policy adjustments, particularly regarding the timing and extent of rate cuts. Similar to trends in other regions, financial markets have tempered their expectations for a rate cut in the UK. There is now a 50% probability assigned to a reduction in June, and while the likelihood of an initial cut by August is high, the total number of expected cuts for the year has decreased to around two, down from six at the beginning of the year. This shift is partly in response to adjustments in expectations for US interest rates and also reflects domestic uncertainties. Some members of the Monetary Policy Committee remain concerned about persistent domestic inflationary pressures, such as wage growth and service prices. However, with headline inflation expected to approach the 2% target in April and interest rates considered to be in restrictive territory, there may be room for signaling that current market expectations on rates could be overly pessimistic. There are several avenues for potential signaling, including a change in policy guidance, although this is unlikely to go beyond indicating the BoE's readiness to lower rates pending economic data. Another avenue is the MPC vote split, which has recently leaned more dovish. While markets anticipate the vote split to likely remain unchanged, there is a risk of additional members favoring a reduction. Additionally, the MPC's updated economic forecast, based on the higher interest rate path currently factored into markets, may suggest inflation undershooting its target for much of the forecast period, potentially hinting at more rate cuts than currently anticipated by markets.

Other than these developments, today's data docket is light. The US weekly jobless claims data will offer insights into the labor market, and the BoE will release the results of its latest Decision Maker Panel survey."

Contributors Warren Patterson and Ewa Manthey update The Commodities Feed: US Crude Inventories Edge Lower.

"Having been under pressure for much of the trading day, oil prices recovered in the latter part of the trading session yesterday and settled higher. However, the broader weakness in the market will likely add further noise around OPEC+ output policy ahead of the next Joint Ministerial Monitoring Committee meeting. OPEC+ members will also become uncomfortable if Brent starts flirting with $80/bbl, a level that is not too far away. As we have mentioned previously, price weakness increases the likelihood that OPEC+ members will fully rollover their 2.2m b/d of additional voluntary cuts into the second half of the year, which risks overtightening the market later in 2024, assuming no downside surprises on the demand side.

The Energy Information Administration’s (EIA) weekly inventory report aided the recovery in oil prices yesterday, which contradicted previously released API crude oil inventory numbers. EIA data shows that US commercial crude oil inventories fell by 1.36m barrels over the last week, different to the 500k barrel build the API reported. The decline in crude oil stocks was driven by stronger exports, which increased by 550kk b/d WoW to 4.47m b/d, and stronger refinery activity. Refinery run rates increased by 1pp over the week to 88.5%, which saw crude oil inputs grow 307k b/d WoW. Stronger refinery activity meant gasoline and distillate inventories increased by 915k barrels and 560k barrels respectively, which were still lower than the builds the API reported this week. A recent concern for the oil market has been weaker than usual US gasoline demand. While demand increased over the week, the 4-week average implied gasoline demand is still at its lowest level since 2014 for this stage of the year at 8.63m b/d (excluding 2020 due to COVID). Concerns over gasoline demand have seen the prompt RBOB gasoline crack trade to its lowest level since February.

In Asia, weaker refinery margins will also be a concern and in recent weeks there have been reports of some refiners in the region cutting or set to cut run rates given the weakness. There will probably not be any respite for margins in the short term, particularly after China recently released its second batch of refined product export quotas for the year, totaling 14m tonnes. This takes total quota releases for 2024 to 33m tons, 18% higher than the first two batches of last year."

TM contributor Mark Vickery says Another Flat Day With Big Afternoon Earnings: ARM, ABNB & More.

"Markets were flat again this Hump Day. Over the past week or so of trading, the major indices have been treading water. For the past month, the Dow and the Nasdaq are marginally in the green, while the S&P 500 is marginally in the red and the small-cap Russell 2000 is -0.9%. For today’s session, the Dow scraped together +172 points, +0.44%, while the S&P was exactly 0.00%. The Nasdaq dipped a tad, -0.18%, while the Russell dropped -0.46%. For the Dow, it’s currently on the most tepid six-day winning streak ever.

Wholesale Inventories for March dropped to -0.4%, the lowest level since -0.5% in June of last year, and swinging to a negative month over month from the downwardly revised +0.2% for February. Lower inventory reads aren’t dire economic prints; in fact, they represent some of the worst growth an economy can have (once inventories are built up, if they do not sell right away, they must be rolled off over time). We’ve only had two positive Wholesale reads in the past year, averaging -2.6% over the past 12 months.

After today’s close, Arm Holdings (ARM - Free Report) reported fiscal Q4 earnings results. The recently re-publicly traded semiconductor design producer outperformed expectations on both top and bottom lines: earnings of 36 cents per share outpaced the Zacks consensus by 6 cents, while top-line sales of $928 million easily surpassed the $885 million analysts were looking for. Next-quarter guidance has been rasied to 32-36 cents per share from 31 cents previously, while full-year revenues of between $875-925 million has a higher median than the $882.5 million estimate. Yet shares are selling off -6% in late trading; that’s something that can happen when you’re +54% year to date: “sell the news.”

Airbnb (ABNB - Free Report) shares are also selling off following its quarterly results. Earnings of 43 cents per share on $2.14 billion in revenues shone past the 23 cents per share and $2.07 billion analysts were looking for. But revenues estimates for the current quarter came in $2.68-2.74 billion, below the previous target of $2.76 billion in the Zacks consensus. It marks the twelfth-straight earnings outperformance for the home-stay experiences provider, but shares are still sliding -8% in late trading."

Contributor Michael J. Kramer writes Indicators Are Suggesting A Stock Market Reversal May Be Coming.

"Stocks were pretty flat today, and we were in a boring sideways session. There is little to say besides that the index is hitting resistance around the 78% retracement level and the 5,198 gap has been filled. A trend line that runs across the tops of the end of April also appears to be serving as resistance. So, at this point, it would appear that all gaps have been filled since the high seen on April 1. There are no open gaps remaining.

The 1-week 50 delta S&P 500 options Implied volatility rose sharply today, with the CPI report next Wednesday. These shorter-term dated measures of IV are likely to continue to climb as we head into the CPI report next week. With the Fed now leaning on data dependence more than ever, every inflation and job report is going to be a high IV event, most likely, and next week has the PPI, CPI, and retail sales all back to back to back.

High-yield spreads also increased today, and those spreads can trade with some of these shorter-dated IV levels. So if we continue to see IV rise, I would think there is a good chance that spreads will widen some more as well."

Contributor Sheraz Mian notes Earnings Growth Poised To Accelerate.

- Total earnings for the 440 S&P 500 members that have reported Q1 results are up +5.0% from the same period last year on +4.2% higher revenues, with 78.0% beating EPS estimates and 60.9% beating revenue estimates.

- The earnings and revenue growth pace for these 440 index members represents a modest acceleration from what we had seen in other recent periods. The +5% earnings growth pace improves to +11.9% once the Energy sector and Bristol Myers’s one-time charge are accounted for.

- For 2024 Q2, S&P 500 earnings are expected to be up +9.2% from the same period last year on +4.5% higher revenues. Estimates have been increasing since the start of April, with the current +9.2% earnings growth pace up from +8.7% on April 3rd.

- Looking at the calendar year picture, total S&P 500 earnings are expected to grow by +8.9% this year after last year’s modest decline. Excluding the hefty Tech sector contribution, whose 2024 earnings are expected to be up +15.9%, earnings for the rest of the index would be up only +6.3%.

"We have consistently flagged signs of improvement in the overall revisions trend in recent weeks, with estimates starting to go modestly up. We are seeing this trend for the current period (2024 Q2) as well as for full-year 2024 estimates.

This new development has roughly coincided with the start of the Q1 earnings season. That said, several sectors, including Tech and Retail, had already been enjoying positive estimate revisions for quite some time. At present, half of the 16 Zacks sectors have higher aggregate earnings estimates than expected at the start of the year.

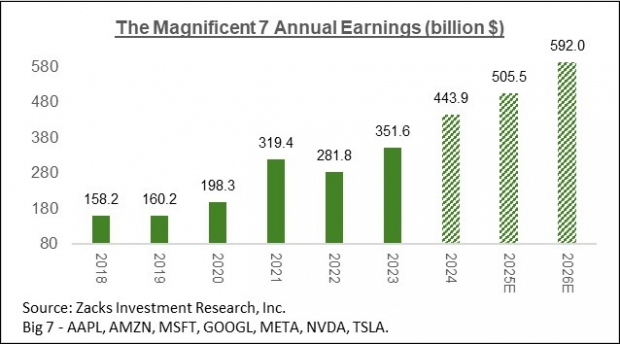

We have recently highlighted the favorable revisions trend for the Energy sector in this space. This week, we will discuss the evolving earnings outlook for the ‘Magnificent 7’ stocks.

The chart below shows aggregate earnings totals for the group on an annual basis.

Image Source: Zacks Investment Research

Please note that the $443.9 billion the group is currently expected to earn in 2024 is up from $438.1 billion last week and $428.2 billion the week prior to that.

We all know that the revisions trend for Tesla (TSLA - Free Report) has been negative for a while now, while the same for Apple (AAPL - Free Report) is also negative, though the magnitude of negative revisions for Apple is far less severe.

The revisions trend for the remaining five members of this group is positive enough to more than offset the Tesla and Apple effects...

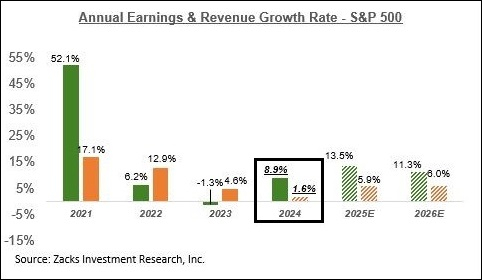

Below, we show the overall earnings picture for the S&P 500 index on an annual basis.

Image Source: Zacks Investment Research

A big part of this year’s earnings growth is expected to come from margins reversing last year’s declines and starting to expand again. The expectation is that aggregate net margins this year get back to the 2022 level, with the Tech sector driving most of the gains."

Contributor Cullen Roche looks at The Outlook For Rate Cuts & The Risks To Markets.

"Here’s an interview I did with Oliver Renick on the Schwab Network from Wednesday discussing the macro outlook and the risks in the coming 12 months.

My baseline assumption is that growth will continue to moderate in the 2-3% RGDP range and the disinflationary trend will persist thru year-end, albeit at a lower rate than we saw last year. I expected Core PCE to end the year around 2.3%. But the tricky part in all of this is the election...

I expect Core PCE to be about 2.55% in June. The Fed likely wants inflation below 2.5% and perhaps well below it before they start cutting. So this means we won’t get cuts at the June and July meetings. The next meeting is in September that’s just a few week before the Presidential election so I think that cut is off the table because the Fed can’t risk looking politically motivated. That leaves us with a November baseline for the first cut. And that might also end up being too close to the election if the election is remotely close.

The reason this is especially interesting is because that means the Fed Funds Rate will still be at 5% if they cut in November. The Taylor Rule (which you can always find at our Macro Dashboard) says the FFR should be 5% right now. So now we’re getting into the really interesting phase of the interest rate cycle where the risk of staying too high for too long becomes elevated. We could potentially get well into 2025 with a Fed Funds Rate of over 4.5%. And that makes this whole environment very interesting for risky assets.

Of course, I like to think of the stock market as a 15-20 year instrument that yields about 6.25% right now so it’s not a great idea to think of the stock market across 12 months, but I would certainly argue that the next 12 months pose some elevated risks. At the same time, bonds look increasingly attractive and savers clipping T-Bill rates over 5% will continue to be in hog heaven."

That's a wrap for today.

Take care and be careful out in the markets.

Peace.

More By This Author:

Tuesday Talk: Still Flying

Thoughts For Thursday: Lingering Inflation

Tuesday Talk: Market Stays Up Awaiting FOMC Meeting

Comments

Log in or sign up to join the conversation.