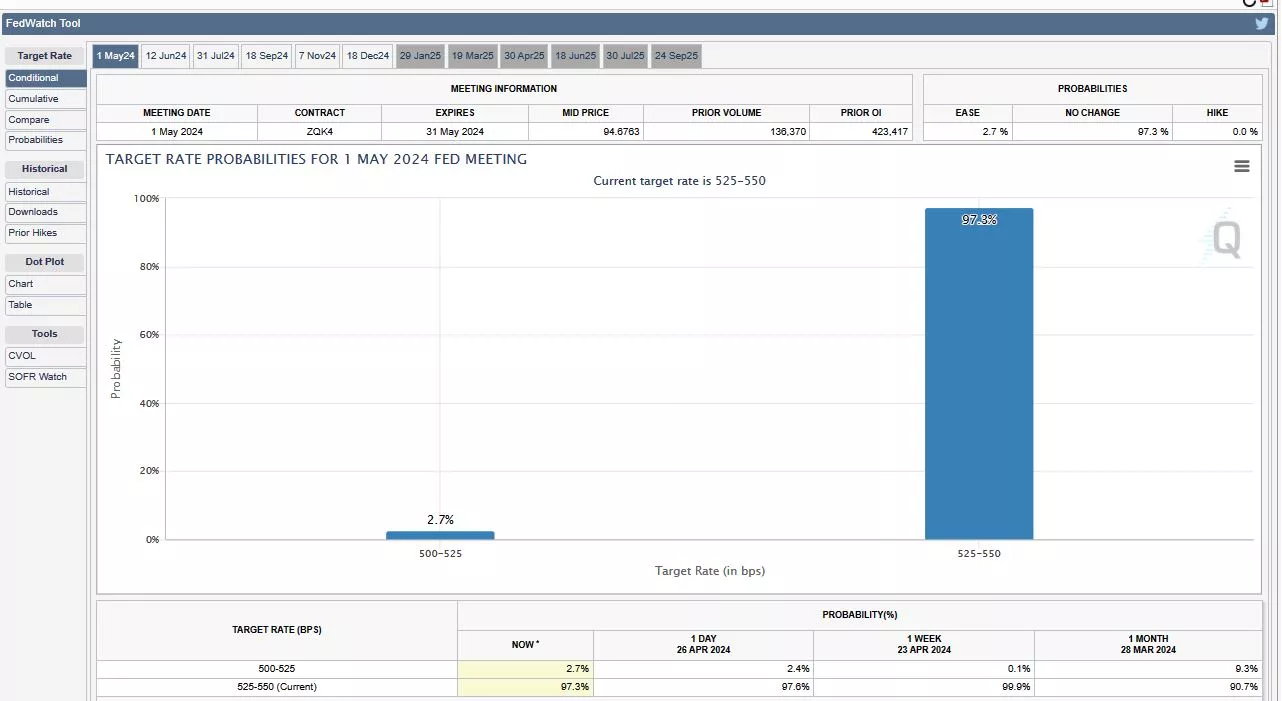

The likelihood of any reduction in interest rates is low as the market awaits the commencement of the upcoming FOMC meeting. CME data shows that 97.3% of respondents believe that rates will stay the same.

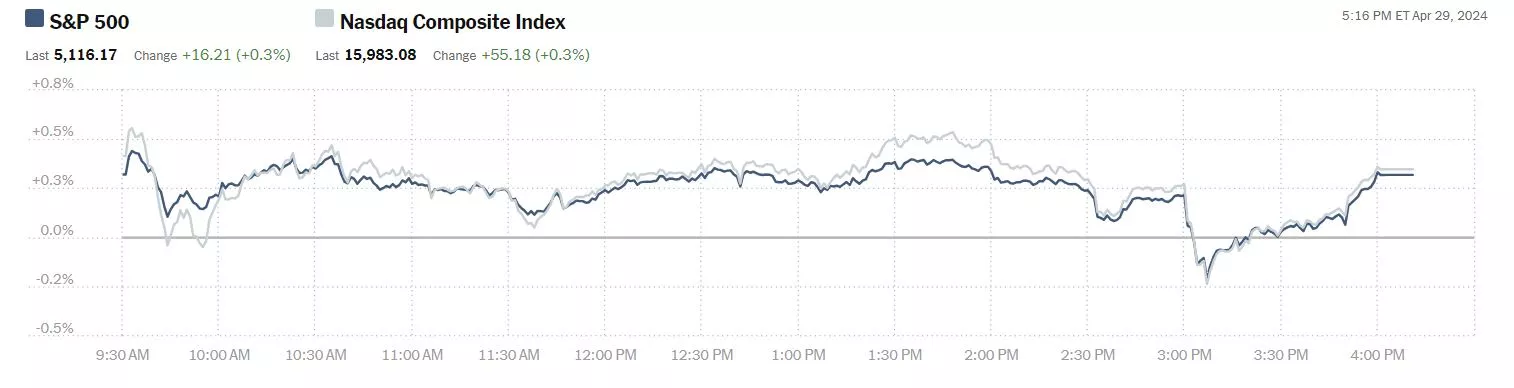

On Monday the S&P 500 closed at 5,116, up 16 points, the Dow closed at 38,386, up 146 points, and the Nasdaq Composite closed at 15,983, up 55 points.

Chart: The New York Times

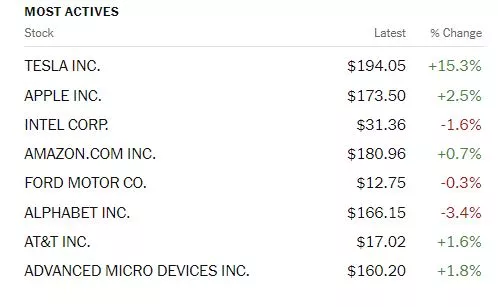

Most actives were led by Tesla (TSLA), up 15.3%, on its new deals in China, followed by Apple (AAPL), up 2.5% and Intel (INTC), down 1.6%.

Chart: The New York Times

In morning futures trading S&P 500 market futures are down 10 points, Dow market futures are down 49 points, and Nasdaq 100 market futures are down 31 points.

TM contributor Mark Vickery reports Markets Up On Tesla, Q1 Earnings; Q1 Beats After The Bell.

"Market indices finished in the green across the board this Monday. It’s now the third straight day higher going back to Thursday of last week, and recovered from a quick drop into the red (mostly) roughly a half-hour prior to today’s close...

Tesla (TSLA - Free Report) saw its strongest single day of trading in three years: +15%. This came on the news that CEO Elon Musk was in China, looking successful in his attempt to expand its autonomous drive technology, Full Self Driving (FSD), software. Many drivers in the U.S. subscribe to this feature, but the Chinese driving public putting the smart technology to work on a wide scale will help the technology inform itself multi-fold. And a newly-purposed Musk is always a welcome sight for Tesla investors.

Paramount Global (PARA - Free Report) earnings are out the same day as a change in the top brass. Long-time CEO Bob Bakish will be stepping down, pending the company’s merger with Skydance Media, and replaced by a triumvirate in the CEO office of three current corporate executives. Meanwhile, earnings of 62 cents per share rallied well ahead of the anticipated 37 cents (and another orbit from the 9 cents per share reported a year ago), while revenues of $7.69 billion were a hair ahead of the $7.68 billion in the Zacks consensus. Shares are up +1.3% at this hour in the after-market.

NXP Semiconductor (NXPI - Free Report) also beat earnings estimates after today’s close. A headline of $3.24 per share outpaced expectations by a sold nickel, while revenues came in dead even with estimates, $3.13 billion. Cautious optimism guides the higher earnings guidance for next quarter, helping send shares up +5% in late trading. Its mobile units outperformed expectations, offset somewhat by downtrends in autos and industrials. The Dutch chipmaker only has one miss on earnings in the past five years...

Today a Q1 Employment Cost Index, April Consumer Confidence, and Case-Shiller home prices for February bring us a wide swath of data. Will the markets keep their buoyant tone amid so much new information?"

Contributor Tajinder Dhillon has a S&P 500 Earnings Dashboard 24Q1 as of Monday, April 29.

"S&P 500 Aggregate Estimates and Revisions

- The 24Q1 Y/Y adjusted blended earnings growth estimate is 8.7%. If the energy sector is excluded, the growth rate for the index is 8.6%. Please note that the 24Q1 year-over-year growth rate for Bristol Myers Squibb reflects an approximate $12 billion one-time charge related to its acquisition of Karuna Therapeutics. When including this one-time item, the S&P 500 24Q1 earnings growth rate declines to 5.6%.

- Of the 233 companies in the S&P 500 that have reported earnings to date for 24Q1, 78.1% reported above analyst expectations. This compares to a long-term average of 66%.

- The 24Q1 Y/Y blended revenue growth estimate is 3.8%. If the energy sector is excluded, the growth rate for the index is 4.4%."

TalkMarkets contributor Derek Lewis highlights 3 Tech Stocks Suited For Dividend-Focused Investors.

"Interestingly enough, several tech stocks – Microsoft (MSFT - Free Report), Dell Technologies (DELL - Free Report), and Qualcomm (QCOM - Free Report) – reward their shareholders with quarterly payouts...

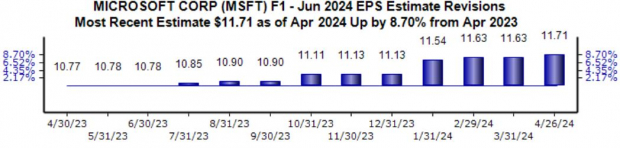

Microsoft

Tech heavyweight Microsoft is coming off a recent double beat, with the company exceeding the Zacks Consensus EPS estimate by nearly 5% and posting sales 2% ahead of expectations. Both items saw considerable growth from the year-ago period, with shares seeing buying pressure post-earnings.

Analysts have positively revised their earnings expectations across the board, with the trend notably bullish for its current fiscal year, up nearly 9% to $11.71 over the last year.

Image Source: Zacks Investment Research

The company has increasingly rewarded its shareholders, boasting a sizable 10.5% five-year annualized dividend growth rate...

Dell Technologies

DELL shares have been considerably strong year-to-date, up more than 60% and crushing the S&P 500’s performance. Positive quarterly results have led the surge, with shares melting higher following its latest quarterly release...

Shares currently yield 1.4% annually, nicely above that of the Zacks Computer & Technology sector average. It’s worth noting that shares have become more expensive amid hopes of growth tailwinds from AI, currently trading at a 15.7X forward 12-month earnings multiple.

Image Source: Zacks Investment Research

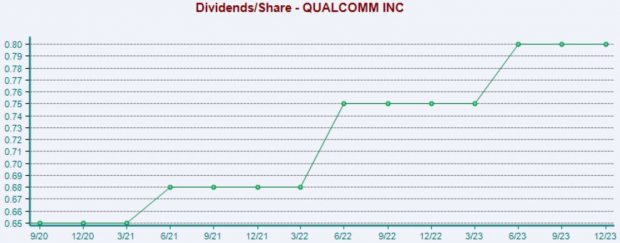

Qualcomm

Qualcomm, a current Zacks Rank #2 (Buy), has seen its shares perform nicely year-to-date, up 17% compared to the S&P 500’s 8% gain.

QCOM shares pay investors nicely, currently yielding 1.9% annually. The company has shown a commitment to increasingly rewarding shareholders, as reflected by its 6.3% five-year annualized dividend growth rate.

Image Source: Zacks Investment Research

...For those interested in gaining exposure to the sector paired with quarterly payouts, all three stocks above – Microsoft, Dell Technologies, and Qualcomm – fit the criteria nicely."

The run-up in Cocoa futures seems to have fallen flat. Contributor Tyler Durden writes, Cocoa Crash Unfolds As "Liquidity Evaporates".

"Cocoa futures in New York crashed Monday in their biggest daily drawdown on record, driven mostly by improved weather forecasts and sliding liquidity.

"Cocoa prices are melting down. New York and London cocoa futures are down ~15% today (that's, by far, the largest one-day % drop in data going back nearly 65 years)," Bloomberg's Javier Blas wrote on X.

Futures fell 15% to $8,931 a ton, having hit a record high of $11,722 on April 19.

On April 9, during the surge from $9,000 to nearly $12,000, Blas warned: "Liquidity in cocoa markets is quickly evaporating."

Saxo Bank's head of commodity strategy, Ole Hansen, explained to Dow Jones Newswires that today's selloff was triggered by an improving weather forecast for rain in West Africa, the mecca of cocoa farming. This will only boost the bean outlook for mid-season crops. He also noted that the front contract showed strong signs of 'buyer fatigue.' "

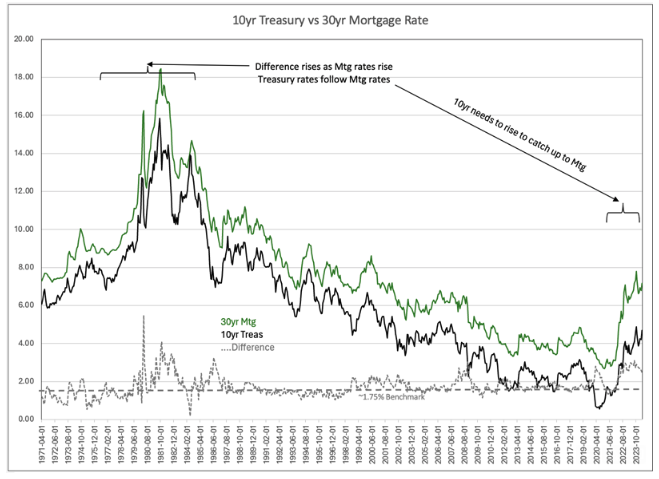

In the housing market, contributor Todd Sullivan writes 10yr/Mortgage Ratio Implies Market Rise Coming.

"Looking at the long-term relationship between the 10yr Treasury vs 30yr Mortgage rates which are generally considered in lockstep, shows they tend to track closely with Mtg rates on average 1.75% higher (labeled as the ~1.75% Benchmark in the chart). The history from Aug 1976 thru Aug 1987 (large bracket) is a period of rapid rate rise. The most interesting aspect of this chart is that the Difference between the 30yr Mtg rate minus the 10yr Treasury rate rises when there is a rapid rise in Mtg rates. In other words, the 30yr Mtg rate leads and the 10yr Treasury rate follows with a lag during rapid rate rises.

Mortgage bankers raise and lower rates as they perceive the Real rate of return they need to achieve. The 30yr Mtg rate generally follows the formula:

% inflation + 3% Real return + x% premium = 30yr Mtg% range

The 3% Real rate of return concept roughly matches the Real GDP average over decades. The premium is adjusted by the perceived credit worthiness of the borrower but heavily influenced by the economic risk profile perceived at the time, which is usually wrong. Knut Wicksell identified in 1898 that a long-term ‘Natural Rate’ for investors operated over multiple business cycles.

Today, with rates rising and Mtg rates already at 7.5% range (small bracket), it is the institutional buyers of Treasuries who are out of sync with the rest of the market and need to catch up. Currently, there is an 88% expectation of lower rates in the near term by institutions per the recent Bank of America Fund Manager Survey. They remain rooted in expecting a recession."

Something to chew on, on the way out. TalkMarkets contributor Julien Chevalier ponders The Impossible Equation Of Global Debt.

"Global debt has reached an all-time high of over $300 trillion. If this amount explains so many things, it is above all the driving force behind a boundless ideology in a world of risks and stakes of all kinds. At a time of revolutionizing interest rates, economic agents are seeking to reduce their debt in order to remain solvent. The financial system not only needs growth to be sustainable, but also scarcity.... Global deleveraging is unrealistic, however...

From the health crisis to the war in Ukraine and the many economic and social issues at stake, global debt has continued to rise.

Global growth, for its part, has remained very weak, despite catching up in 2021, and is gradually slowing as global balances are reconfigured. De-globalization and geopolitical conflicts are further obstacles, with the exception of certain specific zones such as Africa and East Asia, where demographic power is a growth driver. Finally, at a time when inequalities are reaching record levels, governments are maintaining very high levels of spending, preventing them from returning to a budget surplus...

While government debt represents 97% of global GDP, household debt accounts for almost 70%, non-financial companies for around 100%, and banking and financial institutions for 80%. This situation is untenable for households and businesses, the overwhelming majority of which cannot roll over their debt like a state can, nor operate with negative equity like a central bank. The increase in business bankruptcies bears witness to these challenges.

The question then arises: is it possible, today, to carry out a major debt reduction? Looking at recent history, the years following the 2008 financial crisis have shown that it is not...

For many countries, the exponential trajectory of debt means that interest payments are one of the first items on their budget, the main solution is for central banks to lower interest rates. This would stimulate the economy and thus growth, while reducing debt servicing costs in the medium term. The most heavily indebted countries, such as Italy, France and the UK, would still have room to maneuver for some time before they were truly strangled by their debt repayments. But the risk of such a measure, in a period of rising prices, is that it could trigger an inflationary spiral, accentuated by ongoing geopolitical tensions and successive energy crises. This situation, which is inconceivable for central bankers, would require them to keep interest rates sufficiently high until inflation is definitively contained, at the cost of a major social, economic and financial crisis...

The world is taking a tragic path, represented by the global rise in military budgets. As the economist Margrit Kennedy rightly explained: "Military production is the only area where the ‘saturation’ point can be postponed indefinitely." Put another way, war makes it possible to destroy and rebuild, thus creating growth at a time when growth is scarce, and reducing debt levels. In 2023, military spending on all continents will reach a peak of over $2.3 trillion, fuelled by war in Ukraine and the Middle East, as well as other "cold" conflicts in Taiwan, North Korea, Syria, Kashmir and the Balkans.

To halt this trend, a radical reform of the financial and monetary system is urgently needed. Gold's particular appeal in these times, and its historic role as a currency, also testifies to the more or less conscious understanding that the contemporary financial model is reaching its limits. And that tomorrow's model will have to be based on real wealth."

That's a wrap for today.

Have a good one.

Peace.

More By This Author:

Thoughts For Thursday: Stock Indices Stay Steady Amid Corrections

Thoughts For Thursday: Earnings In Earnest

Tuesday Talk: Money And War Go Together Like...

Comments

Log in or sign up to join the conversation.