MARKETS

The S&P 500 surged Tuesday as traders geared up for the high-stakes U.S. presidential election showdown. The broad market index gained nearly 1%, the Nasdaq Composite advanced 1.1%, and the Dow Jones Industrial Average climbed by 332 points (or about 0.8%). With former President Donald Trump and Vice President Kamala Harris in a tight race, all eyes are also on Congress. Control here could bring sweeping spending or tax policy shifts. Still, congressional gridlock could be the ultimate volatility suppressor.

Whoever wins will inherit a relatively strong economy. The service sector, for instance, is thriving, expanding at its fastest pace in over two years thanks to a hiring boost, even as new orders and business activity show slight signs of slowing. And with the Fed standing by with rate cuts to support the labour market, the economic foundation is solid.

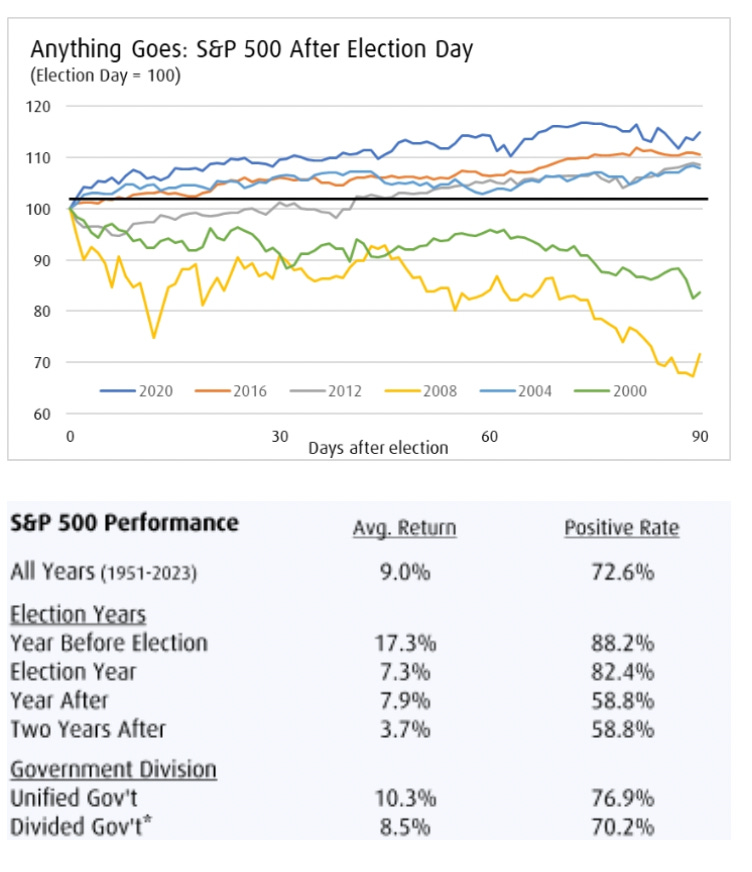

When it comes to elections, however, the equity market’s reaction tends to be less theatrical than many expect. Historically, markets show a muted immediate response; since 2000, post-election performance hasn’t leaned consistently positive or negative. I think using recency bias is a better election temperature check. On a broader scale, the S&P 500 has averaged an annual return of 10.3% under a unified government versus 8.5% with a divided government. Yet, that difference could reflect timing, as unified governments have often aligned with substantial early-cycle recoveries, such as in 2003 and 2009.

Interestingly, a recurring trend emerges in the lead-up and aftermath of elections. The year before the election often delivers a performance pop, averaging a robust 17% return (and 88% of those years were positive), while the mid-cycle, two years after an election, has been more muted, averaging just a 3.7% annualized return (with a 59% positive rate). If the pattern holds, we might see a boost tempered by slower growth by 2026.

Ultimately, the real drivers of the market aren’t found in any election result but in the state of the economy and the monetary policy cycle. Elections may make for dramatic headlines, but it’s the macroeconomic backdrop and Fed policy that set the true course for market performance.

After all, the sugar high for American consumers is still going strong, thanks to rising employment, incomes, and wealth. With the Fed poised to cut rates this week, I expect shoppers to stay energized and keep the momentum going for some time.

OUTCOMES

Under a Harris administration backed by a Democrat-led Congress, we’d likely see a steady flow of deficit spending paired with expanded tax credits, giving the economy a moderate lift. However, this could be tempered by less corporate investment, as higher taxes weigh on business sentiment.

In contrast, a Trump White House with a Republican-led Congress could bring a growth surge fueled by tax cuts, deregulation, and big spending—though we’d also likely see higher inflation, steeper interest rates, and a tilt towards trade protectionism. Equities and the dollar would likely rally at first, driven by optimism around corporate earnings.

If Harris takes the presidency but Congress remains split, expect more of the status quo. With fewer bold moves, we’d see minimal economic or market impact. Meanwhile, a Trump win with a divided Congress could introduce a shaky path forward: trade tensions ramp up without the offsetting benefits of fresh tax cuts, adding a layer of uncertainty for equity markets.

In short, the election outcomes offer distinct paths, each shaping markets with its own mix of fiscal and trade policies. This time around, all eyes are on Congress as much as the White House!

FOREX MARKETS

A Trump victory with a full "Red Sweep" is likely the worst-case scenario for Emerging Markets and G-10 currencies, as it would give the USD more fuel to strengthen, driven by expectations of higher trade tariffs and a looser fiscal stance. While we still anticipate a modest 25bps rate cut from the Fed at this week’s FOMC meeting, a Red Sweep would likely trim expectations for any significant rate cuts in the years ahead.

Put simply, unless Trump pulls off a surprising Red Sweep, the runway for the U.S. dollar rally might not be as long as some hope. In FX circles, the general feeling is that only a full Red Sweep has the power to add serious upside for the dollar. Anything short of that, and the greenback might find itself hitting turbulence. Hence, the rationale for a pullback in the US dollar as the Fed also gets ready to deliver a rate cut.

Conversely, a Harris win with a divided Congress would likely boost emerging markets and G-10 currencies as market participants breathe a sigh of relief, pricing out the risks tied to a potentially disruptive Trump second term. Initially, this outcome could bring a sense of stability to the FX landscape, easing concerns around aggressive trade policies and lifting sentiment across Asia and Europe. Also, it's a tail risk some might see worth getting hedged today.

More By This Author:

As We Shift From FiveThirtyEight To Election Mode, Markets Remain Gridlocked

U.S. Election Betting Pools Tighten Ahead Of A Coin-Flip Race

A Tale Of Ever-Deeper Deficit Spending

Comments

Log in or sign up to join the conversation.