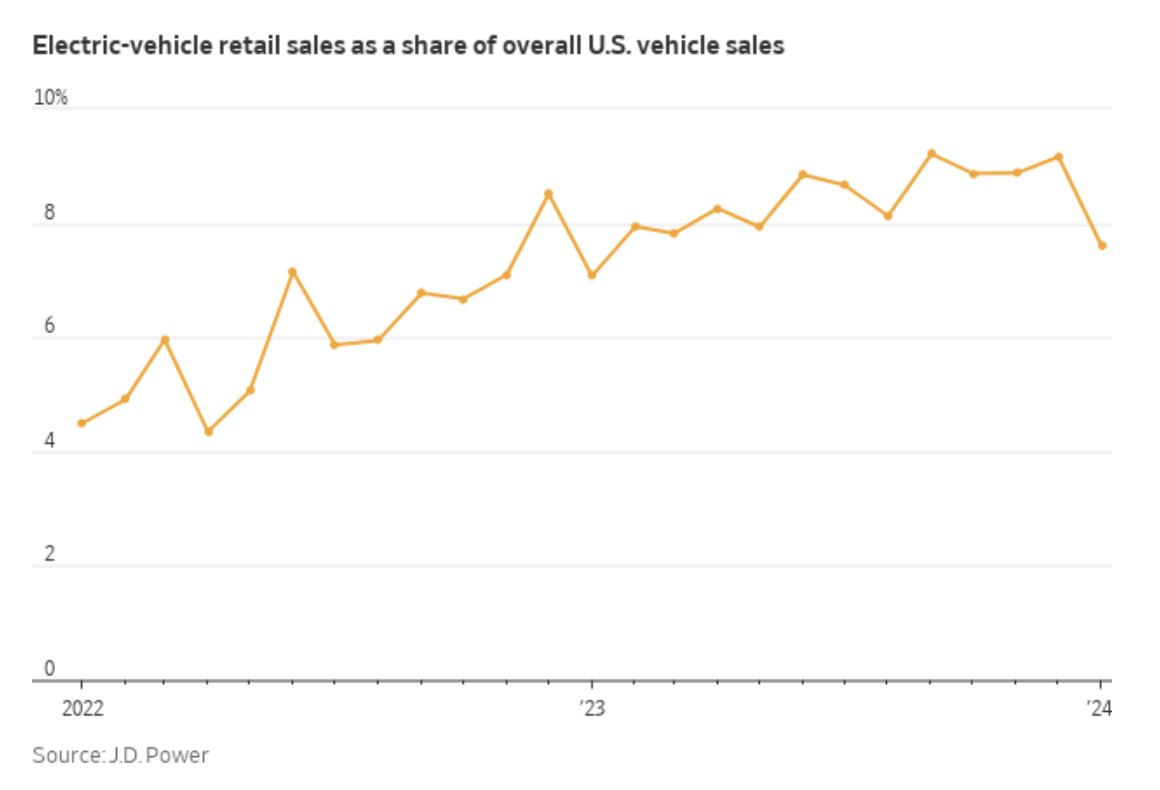

Yesterday’s Commentary discussed the fall of EV maker Fisker. After posting the article, Fisker shares were suspended from trading on the NYSE. Tesla, the world’s largest producer of EVs, has fared much better than Fisker, but it, too, is having problems. For example, Tesla’s revenue growth was only 3.5% in the fourth quarter. Competition from all automakers is a big problem. In particular, Tesla cut production in China as the country ramps up EV production of its vehicles. Tesla just posted its lowest sales in China since 2022. Demand for EVs is another problem. As shown below, the share of EVs to total vehicle sales slipped last month and fell below its trend. Other automakers like Ford and GM are backing off EV production estimates as they foresee weaker demand. As we noted in Is Toyota the Next Tesla, demand for hybrid cars is sapping EV sales as well.

The other problem facing Tesla shareholders is high valuations. Tesla’s largest competitor, Toyota, trades with a forward P/E of 11.2 and P/S of 1.1. Compare that to Tesla, with a forward P/E of 46 and P/S of 6.2. Tesla shares are pricing in significant growth, while Toyota and other automakers’ valuations imply that auto industry growth will be well below the broader market averages. Keep in mind that Tesla’s valuations, while elevated, are much lower than in 2021 when the stock was double today’s price. EVs are more than a fad, but it’s hard to know if EVs will continue to grow their market share at the rate it has over the past five years. Additionally, competition from hybrids, other automakers, and, ultimately, newer technologies pose significant risks to Tesla. While its stock has fallen 25% this year, it may not be time to buy the dip.

What To Watch Today

Earnings

Economy

- No notable economic releases

Market Trading Update

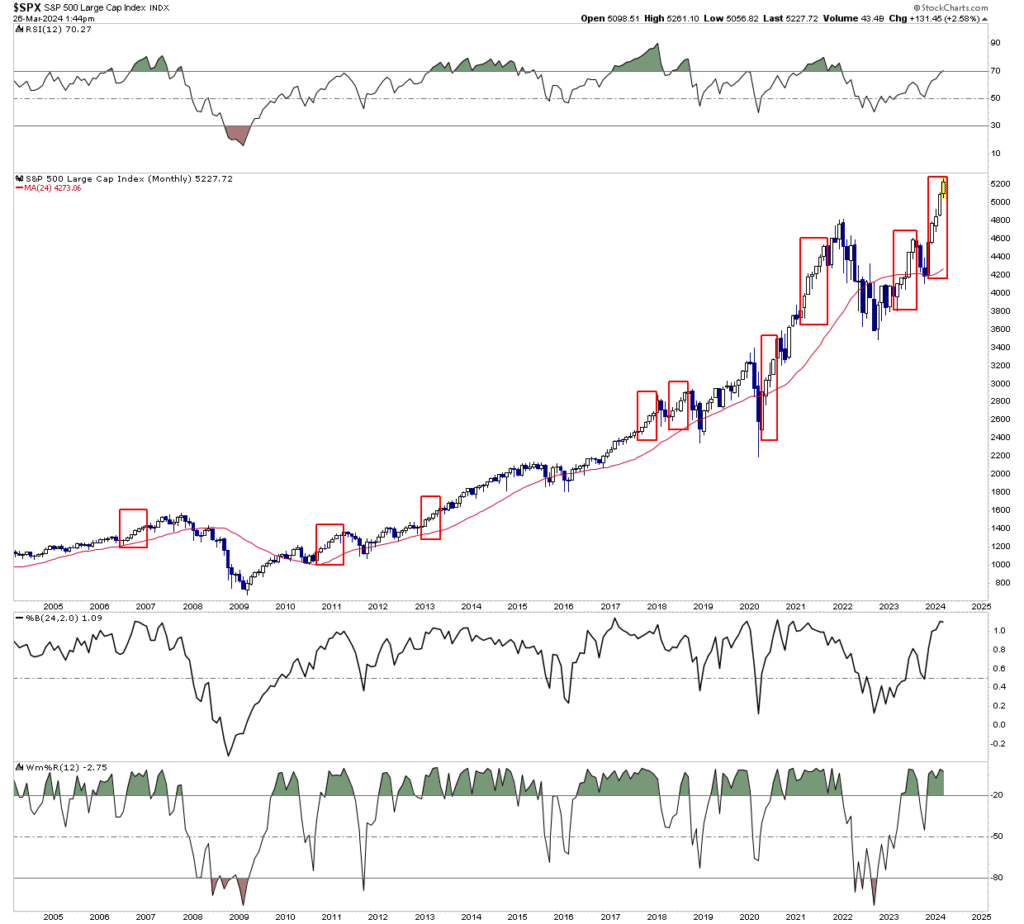

As we begin to close out the month of March, the S&P 500 will have posted 5-positive months in a row. Historically, such long stretches can occur but are often punctuated by either a month or two of declines or a bigger corrective phase. The monthly chart of the S&P shows that over the last 20 years, there have been 9 occasions where the market rallied 5 or more months in a row. While previous stretches did not always resolve into bigger corrective processes, there were at least a month or more of negative returns, which reduced the existing overbought conditions.

With the market trading well above the 2-year moving average and overbought on many levels, a corrective process will occur at some point. However, at the moment, there is little to undermine the bullish sentiment in the market. While we continue to suggest remaining long equity exposure currently, it will be important to maintain a nimble strategy to reduce exposures as and when needed.

The current advance is getting very long, and buyers are becoming exhausted. It is important to remember that the market is a pool of buyers and sellers. Currently, the price is increasing as buyers have to coax sellers into a higher-priced transaction. However, when sentiment shifts and the buyers want to sell, there will be few to take shares at current prices.

As the adage goes, “Sellers live higher. Buyers live lower.”

It is how markets work.

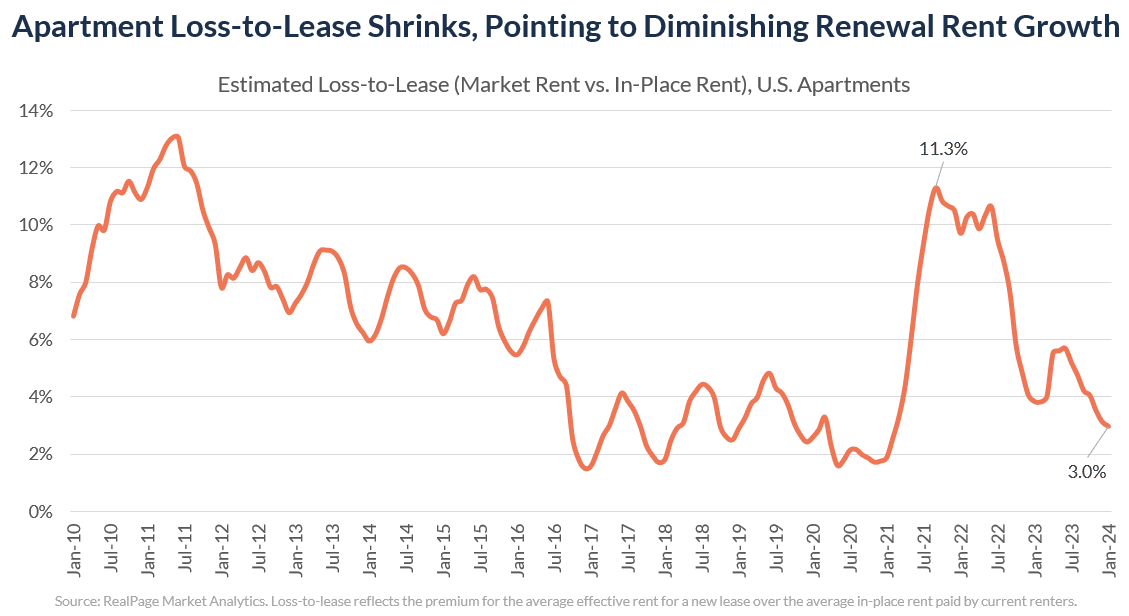

Apartment Loss-to-Lease Ratio Signals Lower Rent Inflation

CPI and other inflation data greatly influence how the Fed manages monetary policy. Rent and imputed rents account for 40% of CPI. Therefore, whatever happens with rental prices greatly affects the Fed, which is also a significant factor driving investor sentiment and, ultimately, markets. Yesterday’s Commentary shared data showing that the number of apartments that came onto the market in 2023 and those coming in 2024 will dwarf the annual amounts built over the last 30 years. On its own, that extra supply should weigh on rental prices.

The graph below shows the loss-to-lease ratio, courtesy of RealPage Analytics, pointing to another factor that should keep rental prices lower. The following is from Jay Parsons:

We measure this through what the industry calls “loss-to-lease” — the premium for a new lease asking rent versus what current renters actually pay today (the in-place rent). A high loss-to-lease number means that current renters are paying a lot less than a new renter walking in the front door. That means they’re likely to see larger renewal increases. A low loss-to-lease number means that current renters are already paying close to today’s market prices for new renters. That means they’re likely to see a small (if any) increase on renewal. As of Jan 2024, loss-to-lease came in at 3.0%. That is a 3-year low. And as renewals continue to inch up (modestly) while new leases are expected to be fairly flat, that’ll narrow the gap more.

Remember that landlords prefer to keep a renter in place to avoid having an empty apartment earning no rent. Accordingly, most rent renewal price increases will likely be much less than in the last few years.

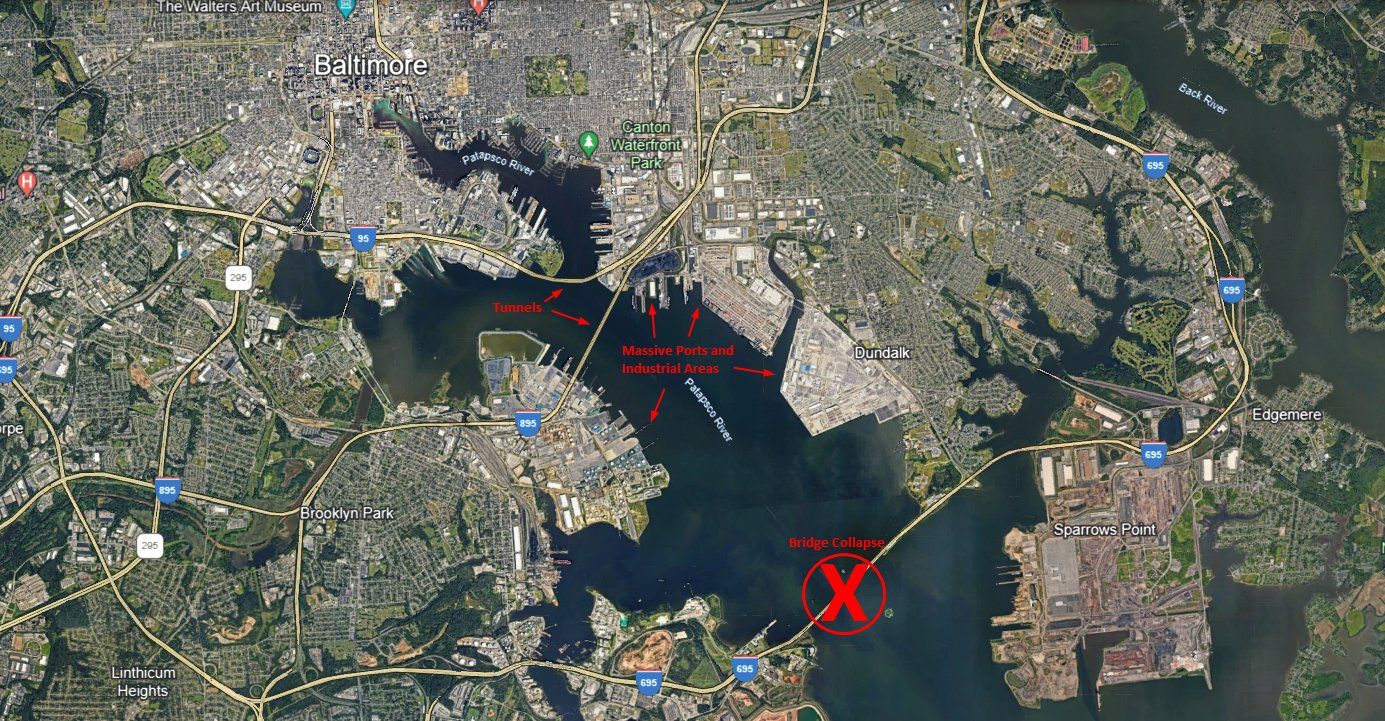

Baltimore Harbor Shuts Down

The collapse of the Francis Scott Key Bridge means that the Baltimore Port will be unusable for a while. The harbor is ranked the 17th largest in the U.S. based on total tonnage. However, it has led the nation’s ports in the import and export of new cars and trucks. The port also accounts for a lot of employment. Per the Maryland Daily Record:

A 2018 report detailed the economic impact of the port on the surrounding region. The report found that 37,300 jobs in Maryland are generated by port activity — 15,330 of which were direct jobs generated by cargo and vessel activities; 16,780 of which were “induced jobs,” supported by the local purchases of goods and services; and an estimated 5,190 indirect jobs.

The question for investors is what might the macroeconomic impact be, especially on prices. As Bloomberg notes,

“The worst thing that can happen for the Fed, the worst thing that can happen for the economy, are these kinds of supply side shocks because what they do is they reduce the productive capacity of the US economy boost inflation at the same time.”

The impact on the economy and inflation is yet to be known. Much of it depends on how long it takes to remove the debris and make the shipping lane viable. In the meantime, the ports of Newark, New Jersey, and Hampton Roads, Virginia, should be able to help accommodate the incoming and outgoing vessels. Employment related to the Baltimore port should be affected, but hopefully, it’s temporary.

We do not anticipate this will meaningfully affect the national economy or prices. However, our view may change as new information is released.

Tweet of the Day

More By This Author:

Apartment Supply Will Surge This YearTechnical Measures And Valuations; Does Any Of It Matter?

CRE Pain Is Just Getting Started

Comments

Log in or sign up to join the conversation.