Something Wicked This Way Comes: McDonald's – A Bear In A Bull Costume

As Halloween nears, kids are choosing costumes to transform themselves into witches, baseball players and anything else they can imagine. In the spirit of Halloween, we thought it might be an appropriate time to describe the most popular costume on Wall Street, one which many companies have been donning and fooling investors with terrific success.

Having gained over 65% in the last two years, the stock of McDonald’s Corporation (MCD) recently caught our attention. Given the sharp price increase for what is thought of as a low growth company, we assumed their new line of healthier menu items, mobile app ordering, and restaurant modernization must be having a positive effect on sales. Upon a deeper analysis of MCD’s financial data, we were quite stunned to learn that has not been the case. Utility-like in its economic growth, MCD is relying on stock buybacks and the popularity of passive investment styles to provide temporary costume as a high-flying growth company.

Stock Buybacks

We have written six articles on stock buybacks to date. While each discussed different themes including valuations, executive motivations, and corporate governance, they all arrived at the same conclusion; buybacks may boost the stock price in the short run but in the majority of cases they harm shareholder value in the long run. Data on MCD provides support for our conclusion.

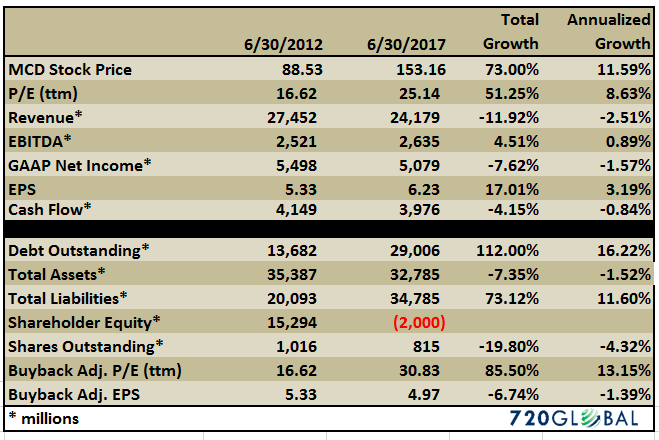

Since 2012, MCD’s revenue has declined by nearly 12% while its earnings per share (EPS) rose 17%. This discrepancy might lead one to conclude that MCD’s management has greatly improved operating efficiency and introduced massive cost-cutting measures. Not so. Similar to revenue, GAAP net income has declined almost 8% over the same period, which rules out the possibilities mentioned above.

To understand how earnings-per-share (EPS) can increase at a double-digit rate, while revenue and net income similarly decline and profit margins remain relatively flat, one must consider the effect of share buybacks. Currently, MCD has about 20% fewer shares outstanding than they did five years ago. The reduction in shares accounts for the warped EPS. As noted earlier, EPS is up 17% since 2012. When adjusted for the decline in shares, EPS declined 7%. Given the 12% decline in revenue and 8% drop in net income, this adjusted 7% decline in EPS makes more sense. MCD currently trades at a trailing twelve-month price to earnings ratio (P/E) of 25. If we use the adjusted EPS figure instead of the stated EPS, the P/E rises to 30, which is simply breathtaking for a company that is shrinking. It must also be noted that, since 2012, shareholder equity, or the difference between assets and liabilities, has gone from positive $15.2 billion to negative $2 billion. A summary of key financial data is shown later in this article.

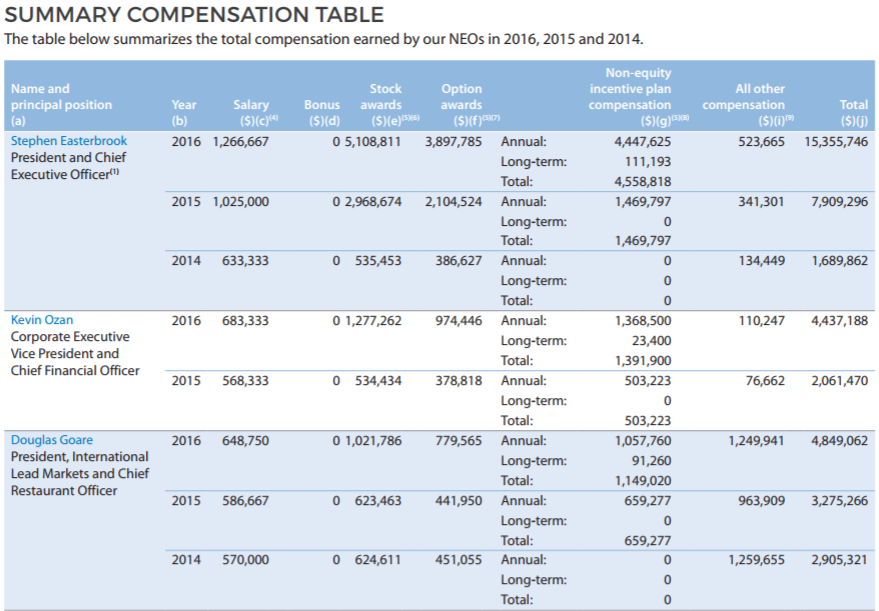

In addition to adjusting MCD’s earnings for buybacks, investors should also consider that to accomplish this financial wizardry, MCD relied on a 112% increase in their debt. Since 2012, MCD spent an estimated $23 billion on share buybacks. During the same period, debt increased by approximately $16 billion. Instead of repurchasing shares, MCD could have used debt and cash flow to expand into new markets, increase productivity and efficiency of its restaurants or purchase higher growth competitors. MCD executives instead manipulated EPS and ultimately the stock price. To their good fortune (quite literally), the Board of Directors and shareholders appear well-deceived by the costume of a healthy and profitable company. Over the last three years, as shown below, compensation for the top three executives has soared.

(Click on image to enlarge)

Source: MCD 2017 proxy statement (LINK)

The following table compares MCD’s fundamental data and buyback adjusted data from 2012 to their last reported earnings statement.

Data Source: Bloomberg and MCD Investor Relations

The graph below compares the sharp increase in the price of MCD to the decline in revenue over the last five years.

Data Courtesy: Bloomberg

Passive Influence

The share price of MCD has also benefited from the substantial increase in the use of passive investment strategies.

Active managers carefully evaluate fundamental trends and growth prospects of potential investments. They typically sell those investments which appear rich and overvalued while buying assets which they deem cheap or undervalued. When there is a proper balance among investing styles in a market, active investors act as a policeman of sorts, providing checks and balances on valuations and price discovery. Would an active investor buy into a fast food company with minimal growth prospects and rapidly rising debt, at a valuation well above that of the general market and long-term averages? Likely no, unless they knew of a greater fool willing to buy it at a higher price.

On the other hand, passive managers focus almost entirely on indexes and are typically less informed about the underlying stocks they are indirectly buying. They are indiscriminate in the deployment of capital allocating to match their index usually on the basis of market capitalization. Such a myopic style rewards those indexes exhibiting strong momentum. When investors buy indexes, the stocks comprising the index, good and bad, rise in unison. Would a passive investor buy into a fast food company with minimal growth prospects and rapidly rising debt at a valuation well above that of the general market and long-term averages? Yes, they have no choice because they manage to an index that includes that company.

When the marginal investors in a market are largely passive in nature, active managers are not able to effectively police valuations, and their influence is diminished. During such periods, indexes and their underlying stocks rise, regardless of the economic and earnings environment.As the saying goes “a rising tide lifts all boats,” even those that are less seaworthy, such as MCD.

Summary

We warn investors that, when the day after Halloween occurs for MCD and other stocks trading well above fair value, investors might find a rotten apple in their portfolio and not the chocolatey goodness they imagined.

Buybacks will continue to occur as long as executives reap the short-term benefits, stock prices rise, money is cheap, and investors remain clueless about the long-term harm buybacks inflict on value. We suspect passive strategies will also garner a larger than normal percentage of investment dollars as long as these blind momentum strategies work. That said, valuations will reach a tipping point and the masking of fundamental weakness will be exposed.

Building wealth on faulty underpinnings is a strategy ultimately destined for failure. We urge investors to understand what they are buying and not be mesmerized by past gains or what the “market” is doing. Simply, when a stock rises above fair valuations, future returns are sacrificed.

Disclaimer: Click here to read the full disclaimer.

McDonalds isn't the only company taking on debt to buyback shares and pay dividends. A huge amount are doing it and one can't blame them. This is what pays in the Federal Reserve's money game. Not investing in capital projects, hiring, or even growing. Debt and financial wizardry rules because capitalism has been distorted.

McDonalds is actually spending money improving their stores as of recent. For that I commend them. The author is right, all is not all roses under the hood, but McDonalds is far from the worst smelling zombie in the market.

$MCD has a long way to go, but their healthier menus is a step in the right direction.

#McDonalds definitely does not deserve to be up 65% in two years and the idea of stock buybacks and passive investing being responsible for most of the gains is interesting. I am curious how far the stock will fall when the current bull market ends. $MCD