Image Source: Unsplash

Historically, the period from November to April has shown the best returns. But that doesn't mean that May to October has been down in these 6 months!

In fact, looking back over the past 25 years, the S&P 500 has gained an average of about 2% from May through October. From November through April, it has averaged closer to 7%.

But before you rush to sell, is it worth being out of the market in the event that this year the market will still be up? (And maybe up as much or more than the November to April average. Remember, these are just averages over time.)

For this reason, rather than sell in May, I am expanding the "defensive" share of our model portfolio. Technology, Consumer Discretionary, and sometimes Industrials and Materials have, over the past 25 years, outperformed the rest of the market from November through April -- but defensive sectors like Health care, Consumer Staples, and Financials have performed better than the S&P 500 average from May through October!

The flaw with the "Sell in May" theory is that it implies that you are better off sitting on the sidelines for six months - which means, in many years, underperformance. That often results in jumping back into the market at the wrong time. (Remember, using the average of many years, these months are still up, just not as much as in the November to April period.)

What "is" true is that sector rotation becomes more important in the usual May to October period. If this is the time that Tech and Discretionary -- and to a lesser degree, Industrials and Materials -- often take a breather, it is also the time when Health, Staples, and Financials rise to the fore.

I will not be selling everything and placing it in cash, even though money market funds sound good right now. The crux of this statement is the "right now" part of that sentence. There is no guarantee that current high money market fund rates will stay at this level over the summer and fall.

Why not exchange some of those funds on the sidelines with quality dividend-yielding companies that pay nearly as much, as much, or sometimes even more? (And, if well-selected, will continue paying for a longer time going forward.)

But here is yet another reason I will be using my normal trailing stop orders for the highflyers, but I will *not* be selling them outright simply because the calendar has turned a month: this is an election year.

The May-October window over the past few elections has been more favorable for the stock market than the average for all years would indicate. Looking at this more granular information, 90% of presidential election years have had positive returns.

Any given year could be an outlier, but I am now buying more defensive sectors like Health Care, Financials, and Consumer Staples firms. No sudden selling, no massive moving, but a more subtle move to be a bit more defensive while still keeping ourselves in the game.

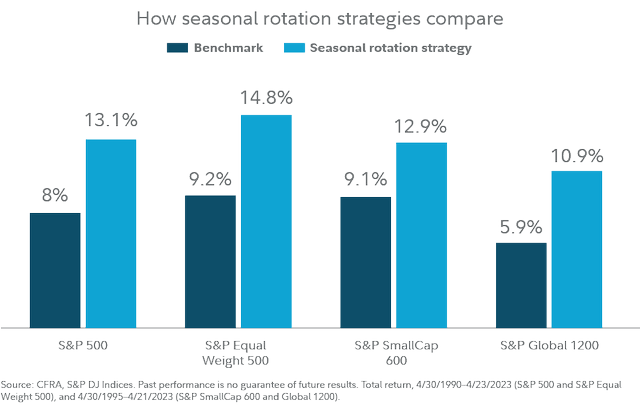

Here is a chart from the Center for Financial Research and Analysis (CFRA) that reflects how (again, on average!) using sector rotation like this, versus just staying in the market with the same stocks that might very well have gotten ahead of themselves, would have performed for an even longer period - the 33 years from April 1990 to April 2023.

CFRA

With that said, all this history is merely "indicative." Each year will be different based on considerations that go well beyond simplistic timing methods. Factors like the economy, inflation, where we are in the business cycle, capital formation, and government intrusions to juice the economy in a presidential election year can all affect the outcome.

So, should you sell in May and go away? If it makes you feel better or safer to sit on the sidelines, then certainly. But don't cry crocodile tears if the market roars ahead at a higher level than the average. There are even now many great companies in these defensive sectors that have barely moved over the past few months of AI mania. It might just be their turn to shine.

Here is just one example of a company I have recently added to our Growth & Value portfolio that I believe fits this strategy well:

Tesco (OTCPK: TSCDY) is the UK's largest grocery store chain, with a commanding 27.4% share in grocery and general merchandise retail sales for this nation of 67 million. It also has a 23.1% share in neighboring Ireland.

Grocery stores are the poster child for defensive companies. People will continue to eat no matter how difficult the times. They may drastically reduce their restaurant visits, but they are unlikely to drastically reduce their food consumption.

Tesco has moved from selling only food as Amazon (AMZN) has moved into selling food. Just as Amazon started selling books, then electronics, toys, clothing, etc., Tesco started with groceries but has now added books, clothing, and toys -- as well as financial services, telecom sales, and internet service. Becoming a one-stop place to fill many needs, big and small, makes sense.

Rather than depend on the steady, but sometimes razor-thin, profit margins of a grocery store, Tesco has concluded, like Walmart (WMT) and Costco (COST), that once a consumer is in the store, they may as well keep them there as they buy non-perishables first, then move onto frozen and fresh foods. The idea in all cases is to have enough offerings to keep the customer in their store rather than see them travel somewhere else.

For Amazon, of course, that means selling so many items that buyers tend to at least "check the prices" at Amazon before moving to a different online site.

Speaking of which, Tesco was an early adopter of selling online and still leads its competitors in so doing -- including for food items.

Tesco has been an early mover in another area, as well: using their loyalty cards to not only give reductions in price as a thank you for your loyalty, but also to use the data of which brands you are buying and providing it to the companies that make the things you are buying. As long as this is done with your permission, it makes for more targeted marketing by the companies that make electronics, toys, clothing, food, etc.

That means, for these companies whose products are in Tesco stores, their advertising expense will likely decline. After all, they do not need to cover the world with ads that most people may not be interested in or respond to. In a perfect world, this might even mean better prices to keep those most loyal.

Who has better data on what is being bought and sold on everyday staples and how many splurge on treats than a grocery store? And who has better data for targeted marketing than those supermarkets with loyalty cards? Costco does it. Safeway does it. And Tesco does it. The difference is that in the UK and Ireland, the competition has not made the same strides as Tesco.

Boring old supermarkets with this trove of data are moving quickly into the forefront. The deepest pockets of them are likely to have the greatest opportunity in this area.

Tesco is also using its handheld customer scanners (to find items or prices) as an advertising medium. It also uses in-store advertising to move more items. It may be subtle but seeing an in-store sign like the one below might move a customer to say, "Hey, that is such a great price I may as well stock up now."

Most of Europe, and an ever-increasing number of nations elsewhere, are making it easier and easier for consumers to reject the cookies that for years traced our buying and viewing habits. Using loyalty cards (again, with permission) allows supermarkets to offer similar data for advertisers. Those cookies gave customers nothing in return; the loyalty cards give discounts in exchange for data.

Tesco has more than 21 million customers using its loyalty cards. That means a lot of discounts -- but also a lot of data. Goldman Sachs expects this UK retail media market to be worth £2bn this year. ($2.54b USD)

As for the stores themselves, I just visited a Tesco Extra store and was surprised at how different it was from my last visit just a little over a year ago. It was huge -- and carried, I am guessing, virtually every one of Tesco's and its providers' food products as well as a wide swath of non-food items. I also had the chance to see an old-fashioned Tesco being remodeled in a smaller town and to shop in a couple of "Tesco'One Stop" shops. (Think convenience stores but with better lighting and much neater. It is Great Britain, after all.)

Tesco is not without competition. But the biggest source thereof is not from Sainsbury's or Morrison's but from Lidl and Aldi, two discount chains from Germany. While they might undercut Tesco on price a good part of the time, they are more "barebones" stores and do not have 21 million loyalty card customers who are benefiting from discounts very close to what these two German discounters offer.

Since I am not often in agreement with SA's Quant ratings, I was surprised to see the chart below. I was initially looking for the three or four deepest-pocketed grocery chains. Given the changes coming to this industry, I wanted to make sure Tesco was as high as I thought it was in terms of market capitalization, revenue, etc. No surprise there, but I see that among the biggest of the big, Tesco is the only one of the three which is ranked as B- or higher across all five of the Seeking Alpha primary ranking measures.

Seeking Alpha

Tesco only pays a 3.79% dividend (semi-annually), still higher than most of its competitors. As with any large company, we can always expect to see labor issues in the future.

Beyond these two items, I do not see any other problems in the immediate future. Even inflation is not the bugaboo in this business. They and we would rather see lower inflation, but with inflation high or low, we are still going to eat.

More By This Author:

Boeing: 1, 2, 3 Strikes, You're Out

Why Lithium Stocks Are Plunging Like Niagara

The Last Fallen Angel For 2024

Comments

Log in or sign up to join the conversation.