Image Source: Unsplash

“Nvidia takes a $1 billion stake in Nokia” reads a recent CNBC headline. As part of the agreement, Nokia commits to purchasing Nvidia’s AI chips and computer platforms. Additionally, the companies will collaborate to develop 6G cellular technology. Deals like this are becoming more common in the AI industry. Some view Nvidia’s recent investment in Nokia and other similar deals as a form of vendor financing. This common practice involves a producer of goods (Nvidia) extending credit (lending money) to a customer of theirs (Nokia) so the customer can purchase the producer’s products. Often, the producers’ goods serve as collateral for the deal. By striking the agreement, the producer aims to boost revenue.

Others, however, deem the agreement as round-tripping. While round-tripping, like vendor financing, aims to boost sales, it is not as straightforward. The funding is not nearly as specific about which goods are being funded or the amount of those goods. It is much more open-ended than vendor financing.

Round-tripping is defined as follows per ChatGPT:

Round-tripping (also called circular investment or recycling capital) is a financial practice where money is invested in a company with the explicit or implicit agreement that the recipient will use those funds to buy products or services from the investor—effectively returning the capital (or a large portion of it) back to the original investor. It creates the appearance of strong demand and revenue growth while masking the fact that the investor is indirectly funding its own sales.

To better understand how the AI industry is funding itself and the potential risks involved, we believe it is helpful to draw on historical context from the dotcom bubble, when similar deals were common amid a thriving technology sector.

Before going back in time, we offer a quick review of some of Nvidia’s financing and investment arrangements, as well as the complex web of financing deals involving Nvidia, OpenAI, and various other companies.

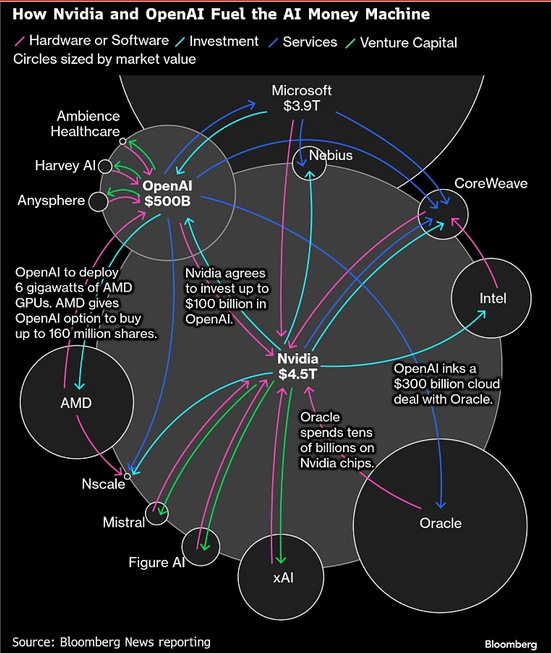

The AI Money Machine

In addition to the newly signed Nokia deal, below is a summary of a few of Nvidia’s most significant equity investments:

OpenAI: Nvidia has committed to investing $100 billion into OpenAI. OpenAI will use most of the capital to purchase Nvidia GPUs for its data centers. OpenAI’s CFO, Sarah Friar, acknowledges that “most of the money will go back to Nvidia.”

CoreWeave: Nvidia has a $3 billion equity position in CoreWeave. CoreWeave recently opened a $2.3 billion debt facility, collateralized with Nvidia chips, to fund the purchase of more Nvidia chips, data center investments, and operations.

xAI: Nvidia plans to invest up to $2 billion in xAI (Elon Musk’s X platform). In a recent CNBC interview, Elon Musk said that “xAI will deploy a million of Nvidia’s advanced Blackwell chips at a new facility near Memphis.”

The deals are similar in that Nvidia invests in the company, which then uses those funds to buy Nvidia GPUs and other equipment, and Nvidia earns additional revenue. With the new revenue and earnings, Nvidia may recycle the capital into the same or similar companies.

While Nvidia may be the most prolific investor in these circular deals, the web of similar financial arrangements within the AI industry includes many large public companies, in addition to OpenAI, as we share below.

Dot Com Roundtripping

To better appreciate what round-tripping deals are, we share a few examples from the telecom boom of the late 1990s and early 2000s. Like today, there were many financial deals between companies outside the traditional capital markets. Some were perfectly viable and worked out for all parties. However, some proved fraudulent and or extremely costly, as we share.

Lucent Technologies:

Lucent aggressively lent money to its own customers to enable them to purchase Lucent equipment. They then recorded the value of the loans as sales revenue on its income statement, even though the repayment risk remained with Lucent and the debt was held as an asset on its balance sheet. This accounting approach temporarily inflated Lucent’s reported revenues and helped drive its stock price higher during the late 1990s.

Lucent also made equity investments by acquiring companies that would buy its equipment. These acquisitions were typically paid for with Lucent stock, allowing them to use its surging stock as a currency to grow their revenues and market share.

The Lucent stock chart below shows everything about how the equity financing deals turned out. Lucent dropped from over $38 billion in revenue in 1999 to just $8 billion in 2006. They avoided likely bankruptcy by selling out to Alcatel for $3.01 per share.

Nortel Networks:

Like Lucent, Nortel boosted sales by using its own shares as financing for its customers. It is believed Nortel lent over $7 billion to help start-up telecom carriers buy its equipment. It was later discovered that many of the loans were interest-free, unsecured, and tied to future purchases.

Nortel tied its future to its customers. Not surprisingly, when the dot-com telecom bubble burst, its customers failed, ultimately forcing Nortel into bankruptcy. In July 2000, Nortel shares peaked at $86.75. In 2009, they were valued at 18 cents.

“From $398 billion to zero in under a decade.” — Financial Post, 2009

Global Crossing And Qwest

The examples above toe the line between vendor financing and round-tripping. The following round-tripping example is outright fraud committed by Global Crossing and Qwest.

- Global Crossing would “sell” fiber-optic network capacity to Qwest.

- Qwest would “sell” similar capacity back to Global Crossing for nearly the same amount.

- Both companies booked the deals as revenue.

The SEC found that this arrangement was a pre-arranged swap designed to inflate their sales figures, yet with no commercial purpose.

Both companies were charged by the SEC with fraud, paid penalties, and restated earnings. Global Crossing shares were worthless when they filed for bankruptcy in 2002. Qwest avoided bankruptcy, but its stock fell from a high of $52 in 2000 to $1.00 in 2002.

These were not arms-length transactions… they were prearranged swaps designed solely to inflate revenues.” — SEC Enforcement, 2002

“We swapped capacity like baseball cards.” – Leo V. Welter, a former senior executive at Qwest Communications International—congressional testimony 2002.

Summary: Understanding Nvidia’s Risk

There is a thin line between the definitions of round-tripping and vendor financing. Round-tripping is generally viewed as a financial gimmick—a pseudo-fraud—used to boost sales. Vendor financing, on the other hand, is a commonly accepted practice, albeit with the same result: increasing sales.

We are not accusing Nvidia, OpenAI, and other large tech companies of the round-tripping that Global Crossing and Qwest participated in. However, the experiences of Lucent and Nortel illustrate the risks of using equity and financing to promote sales. Essentially, these companies are tethering their financial prospects to those of their customers.

As we saw in 1999, the hype surrounding fast-moving technological advances blinded many executives and investors. Massive errors of judgment were made.

Today, shareholders in companies involved in these arrangements should closely monitor these deals and understand that it’s not just the company’s financial strength that matters, but also that of their customers and the AI industry. A failure of a large AI company could send ripples through the entire industry. Moreover, given the massive influence these AI leaders have on major stock indexes, the potential threats could also affect the broader market and economy.

More By This Author:

CAPE Valuations: Does Nvidia Overstate Its Ominous Warning?

Dollar Debasement: Reality Or A Dangerous Narrative?

SRF: The Fed’s Newest Liquidity Backstop In Action

Comments

Log in or sign up to join the conversation.