In August, the BLS revised 2024 employment growth lower by 818k jobs in its preliminary revision of its Current Employment Statistics (CES). Despite the substantial revision, more reductions to the official employment data are likely to come next month. In January, the BLS will release its final benchmark revision. The preliminary and final revisions to BLS data are done annually. The revisions bridge the gap between the monthly BLS survey data used to report the initial data and data from each state’s unemployment insurance program. While the process produces more accurate results, it recently exposed the jobs market as weaker than investors appreciate.

In a report issued last week, the Philadelphia Fed warns that the 2024 final CES could result in even more downward revisions. As their chart below shows, all but eight states will contribute to lower revisions. Per their press release:

Estimates by the Federal Reserve Bank of Philadelphia indicate that the employment changes from March through June 2024 were significantly different in 27 states compared with preliminary state estimates from the Bureau of Labor Statistics’ (BLS) Current Employment Statistics (CES). Early benchmark (EB) estimates indicated lower changes in 25 states, higher changes in two states, and lesser changes in the remaining 23 states and the District of Columbia.

While the data revisions may not pique investors’ interest, they are important for asset prices. Simply, monetary policy has a significant influence on asset prices. Thus, weaker employment than initially thought gives the Fed more fodder to ease policy, which tends to feed liquidity and bolster asset prices.

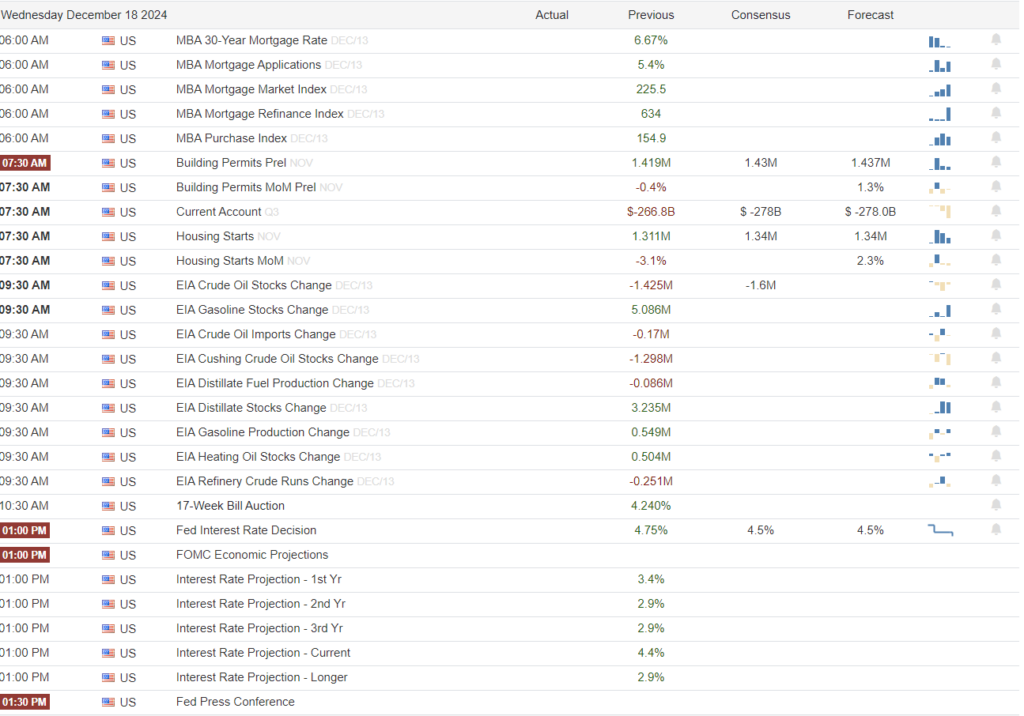

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

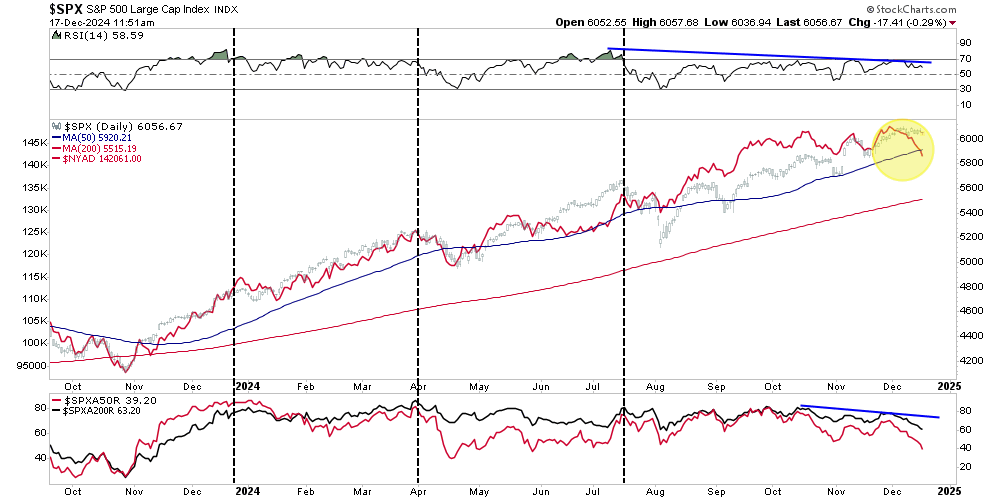

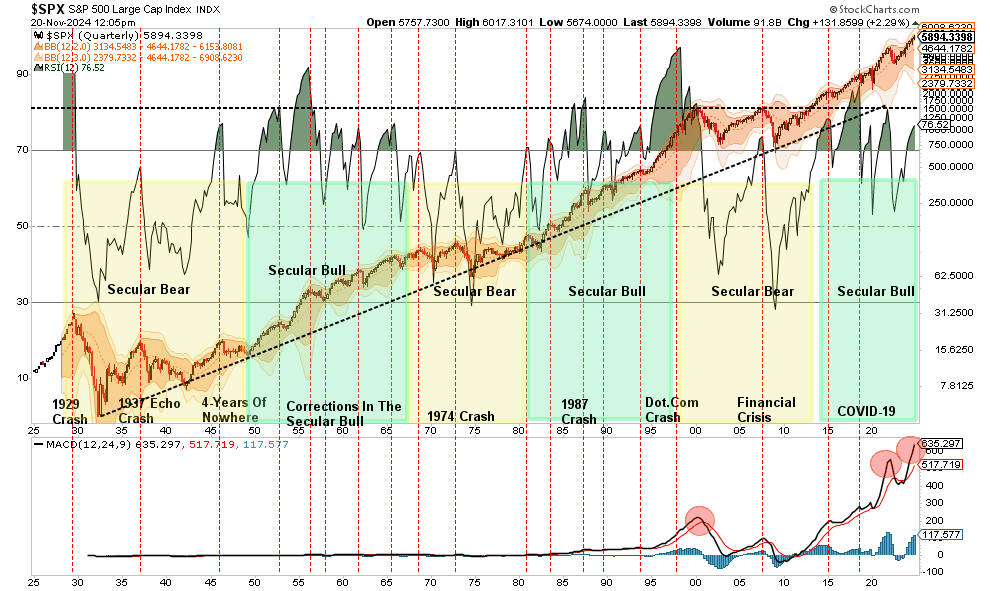

Market Trading Update

Yesterday, we noted that the market continues to trade sloppily heading into today’s FOMC meeting, and volatility is very low. The Fed is expected to cut rates by 25bps. The “surprise” factor could be a discussion of pausing further rate cuts into next year, which could impact short-term market sentiment. That is a risk given the more excessive bullishness on display, with investors piling into stocks heading into year-end.

However, there is a technical divergence worth noting. Breadth is rather dismal.

Despite the many optimistic assumptions, breadth has been deteriorating noticeably. From the NYSE Advance-Decline line to the percentage of stocks trading above their respective 50 and 200-DMA, overall participation is declining rapidly. While such does not mean a market crash is imminent, such previous deterioration has eventually coincided with short-term corrections and consolidations.

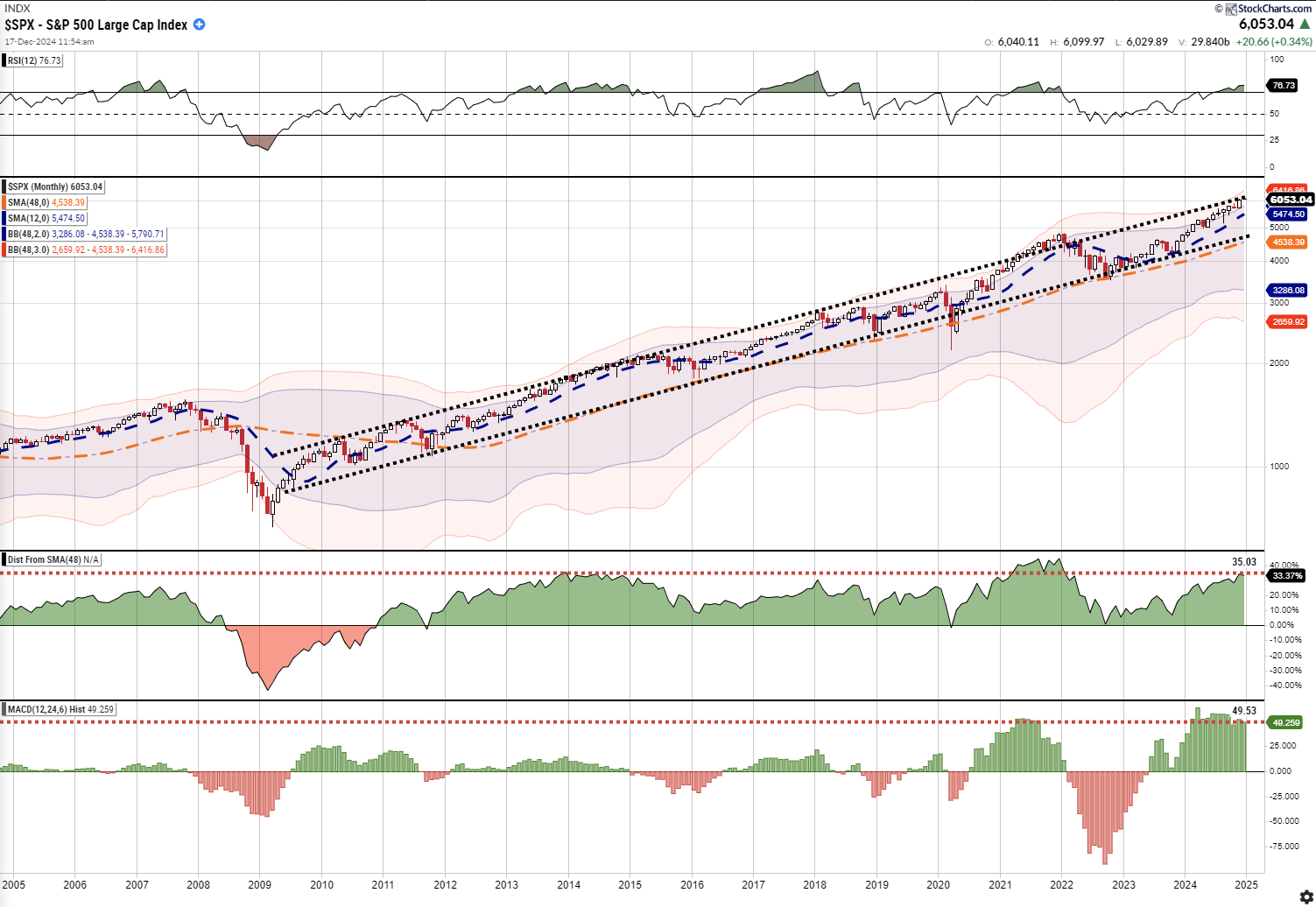

However, it isn’t just short-term market breadth that should provide investors some pause. The market is technically extended on many levels after the past two years of excess returns. The monthly market analysis shows the S&P 500 is significantly overbought on a relative strength basis, deviated from the long-term mean, and pushing well into the top of its bullish trend from the 2009 lows. While we discussed the same factors in the middle of 2021, it took several months before the market gave way and corrected the excesses in 2022. Given the market’s current momentum, we suspect the bullish run will likely last into the first half of next year.

(Click on image to enlarge)

What is crucial to understand is that these technical extremes are just the “kindling” for a correction. To “ignite” the correction, some event must provide the catalyst. That event is not anything you are currently thinking of. It will be an unexpected, exogenous event that causes a sudden shift in market expectations for earnings growth. As those earnings expectations are reversed, the market will decline to reduce valuations for a new reality.

Does any of this mean the market will correct with absolute certainty? Of course not. The one thing the market does well is doing precisely the opposite of what you would expect. Such has been mostly the case since 2022, when everyone expected a recession. Today, no one expects a recession or a market reversion, so we should probably pay attention to the risks we are taking.

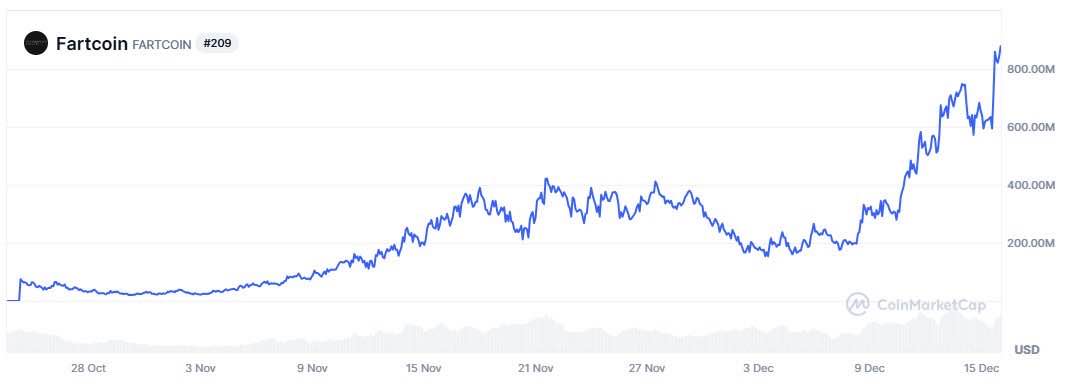

FartCoin And Hawk Tuah- Speculative Excesses On Full Display

Speculative fever is undoubtedly hitting the crypto market and spreading to companies linked to it, like MicroStrategy. Some reasonable justifications for owning Bitcoin may justify its soaring price. However, crypto investors must also consider crypto prices are being driven higher due to a speculative craze in the crypto market.

We share the graphs below for evidence. FartCoin is the latest cryptocurrency to make the headlines. The last one, Hawk Tuah, failed miserably. Since December 8th, FartCoin has risen fourfold and is approaching a $1 billion market cap. For context, consider that FartCoin is now larger than 38% of all American publicly traded companies.

Permabull? Hardly

Navigating the markets requires balancing optimism with caution and adaptability. While bull markets tend to dominate history, bear markets are sharp reminders of the risks of complacency. Labeling investors as “permabulls” or “permabears” oversimplifies the complexities of portfolio management, which requires responding to evolving market dynamics.

We’ve been bullish recently, but historical indicators and emerging risks—such as market exuberance, elevated profit margins, and potential fiscal tightening—suggest increased caution may be warranted in 2025. The goal is not to predict every market move but to prepare for shifts in risk and reward. This approach has helped us navigate past cycles, even if we’ve occasionally made missteps.

Investors should focus on maintaining a disciplined strategy, diversifying risk, and watching for signs of change. Being neither overly bullish nor bearish allows for greater flexibility in protecting and growing capital over the long term.

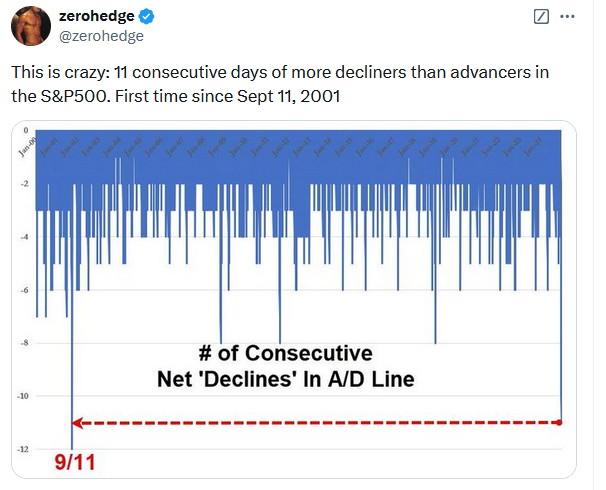

Tweet of the Day

More By This Author:

The Dollar And Domestic – International Relative Stock Returns

Permabull? Hardly

Britain And European Economic Growth Sputters

Comments

Log in or sign up to join the conversation.