I never thought someone would label me a “Permabull.” This is particularly true of the numerous articles I wrote over the years about the risks of excess valuations, monetary interventions, and artificially suppressed interest rates. However, here we are.

“Lance, you are just another permabull talking your book. When this market crashes you will still be telling people to buy all the way down.”

I get it. We have been bullish over the last couple of years, but suggesting that we will always be bullish is a misstatement. For example, in January 2020, we wrote two articles explaining why we were reducing risk.

“When you sit down with your portfolio management team, and the first comment made is “this is nuts,” it’s probably time to think about your overall portfolio risk. On Friday, that was how the investment committee both started and ended – “this is nuts.” We have been discussing the overbought, extended, and complacent market over the last couple of weeks, but on Friday, I tweeted out a couple of charts that illustrated the excess.”

The first chart compared the Nasdaq to the S&P 500 index. Both indices pushed 2 standard deviations above the 200-week moving average. with two things jumping out immediately:

- Near-vertical price acceleration in the markets has been a historical hallmark of late-stage cycle advances, also known as a “melt-up” phase.

- When markets get more than 2 standard deviations above their long-term moving average, reversions to the mean have tended to follow shortly after that.

At that time, we met both conditions. However, we needed more.

“If it were only price acceleration, we would just be mildly concerned. However, investor complacency has also reached more extreme levels with PUT/CALL ratio now hitting historically high levels. (The put/call ratio is the ratio of “put options” being bought on the S&P 500 (theoretically to hedge risk) versus the number of “call” options purchased to “lever up” risk.)”

Here is that chart of the Put/Call ratio versus the market in January 2020.

As we concluded at that time:

“While none of this means the market will “crash,” it does suggest the risk/reward ratio is not in favor of the bulls short-term. Yes, “this is nuts,” which is why we took profits out of portfolios on Friday.

I then wrote a post the following week. That post addressed the multiple emails chastising us for “bailing on the bull market, which is clearly going higher.”

While many thought we were being overly “bearish ” at the time, we reduced exposures again in February. Then, in March, the market declined by roughly 35% as the economy was shuttered.

I want to point out that we are not “permabulls.” In reality, we are neither “bullish nor bearish.” We analyze the market for opportunities or risks and adjust our portfolios accordingly. Since November 2022, we have been bullish on the market following the mean-reversion that started in January.

However, while we remain bullish through the end of 2024, there are increasing risks to the market heading into 2025.

Neither Permabulls Or Permabears

There are certainly many “permabulls” in the financial markets today. From Ed Yardeni to Jim Cramer, there are many Wall Street analysts consistently forecasting higher markets. One reason is that being a “permabull” is more profitable than being bearish. This is because financial markets rise much more often than they fall. Such was a point we discussed in “Market Declines And The Problem Of Time:”

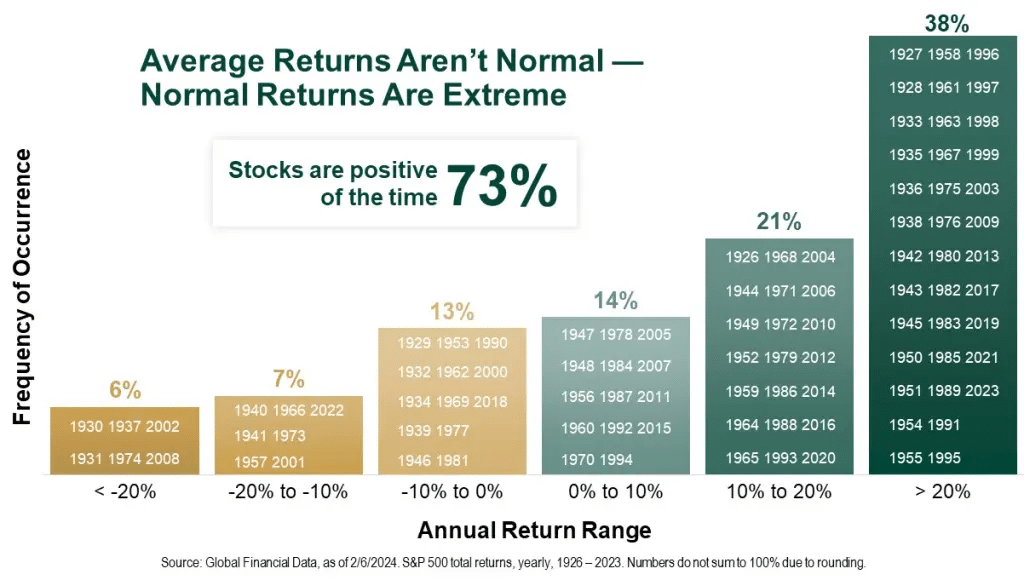

Since 1900, the stock market has “averaged” an 8% annualized rate of return. However, this does NOT mean the market returns 8% every year. As we discussed recently, several key facts about markets should be understood. Stocks rise more often than they fall: Historically, the stock market increases about 73% of the time. The other 27% of the time, market corrections reverse the excesses of previous advances. The table below shows the dispersion of returns over time.”

For analysts, being permanently “bullish” leads to a 73% success rate on market calls. Furthermore, while there are events that precede the other 27% of outcomes, human psychology prompts us to forget painful events. Therefore, market participants only tend to remember the calls to “buy stocks” that came near market bottoms. Such is despite the same analyst saying to “buy stocks” during the entire corrective cycle.

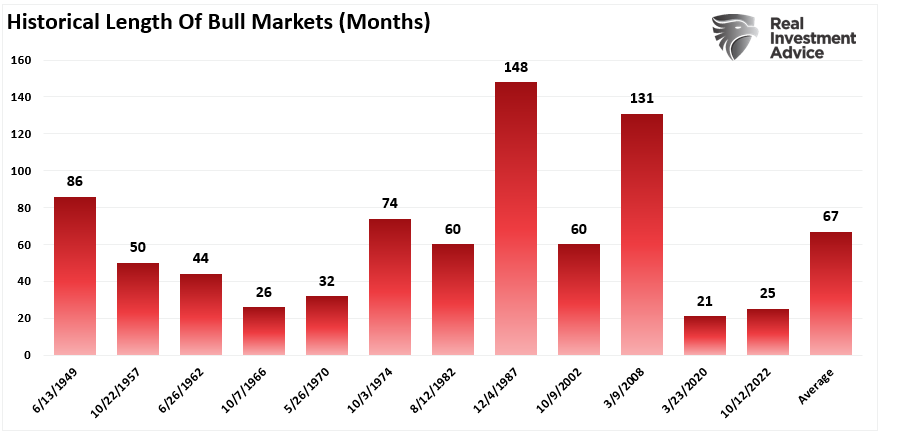

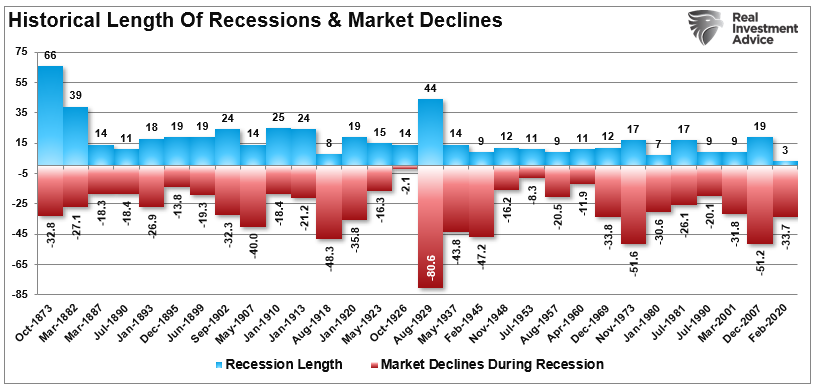

Given that historical bull markets are generally lengthy, being a “permabull” tends to be right more often than not. The chart below shows the length of previous bull markets throughout history, with the average length of bull markets running about 5 1/2 years.

While the long duration of bull markets tends to favor the bulls, the problem is the eventual ending, which always occurs. As shown, bear markets and, generally, the ensuing recessions tend to be very short in length. The majority of bear markets last less than 18 months, and while they are painful experiences, they tend to be quickly forgotten when bullish price action returns.

For investors, the problem with “permabullish” views is the destruction of capital during bear market declines. As is always the case, getting back to even is not the same as making money. This is why navigating market cycles over the long term is both difficult and necessary.

Yes, we have been bullish over the last two years, but we are not “permabulls.” While we made the right call in early 2020, we were also wrong by remaining underweight equities until July 2020, which penalized our performance that year. Our mistake was focusing on the economic and earnings impact caused by a shuttered economy. (Hardly a “permabull” position.) Our failure was to accurately assess the impact of sending checks to households, billions in monthly QE, and zero interest rates fueling an immediate return to market exuberance.

The rapid reversal of “panic” to “FOMO” was something we had never experienced before and was not factored into our risk-management models. However, that was a lesson learned about the impact of monetary and fiscal interventions on the financial markets. In December 2021, we warned that “exuberance” had once again returned to the markets and that we needed to become more cautious.

“This type of market activity is an indication that markets have returned their ‘enthusiasm’ stage. Such is characterized by:“

- High optimism

- Easy credit (too easy, with loose terms)

- A rush of initial and secondary offerings

- Risky stocks outperforming

- Stretched valuations”

Unsurprisingly, the market peaked in January 2022 and began a correction that lasted into late October as Russia invaded Ukraine and the Federal Reserve aggressively hiked interest rates. We remained bearish and underweight equities throughout the year, and then, in January 2023, we wrote that the “Pain Trade For The Market Was Higher.”

“With everyone extremely bearish and confident of a recession, such puts the markets into a position where there are few buyers and an overwhelming number of sellers. From a contrarian investment view, that is an ideal setup for a “pain trade” higher, which we have discussed as a rising possibility.”

We have remained primarily bullish on the markets since then.

However, we may be getting closer to turning tactically more bearish on the markets in 2025.

From Bullish To Bearish – Eventually

While there is little reason not to remain bullish on the markets currently, there are three (3) primary reasons that tilting for “bearish” in 2025 may be necessary.

Market Exuberance And Risk-Taking

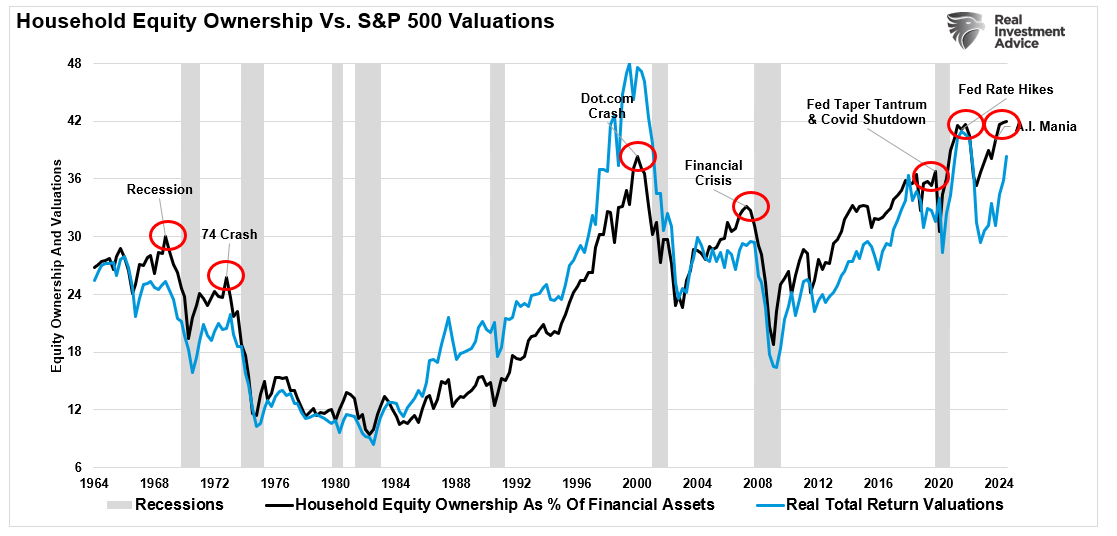

As noted above, in early 2020, we noted that market exuberance and risk-taking were reaching extremes. We are seeing evidence of the same again as investors pile into some of the most illiquid and highly leveraged investments to take on additional speculative risk. However, it isn’t just speculative assets, it is essentially all equities as households now hold a record allocation to equities combined with high valuations. While valuations are a terrible market timing device, when combined with excess household equity allocations, such have provided the ingredients for a reversal.

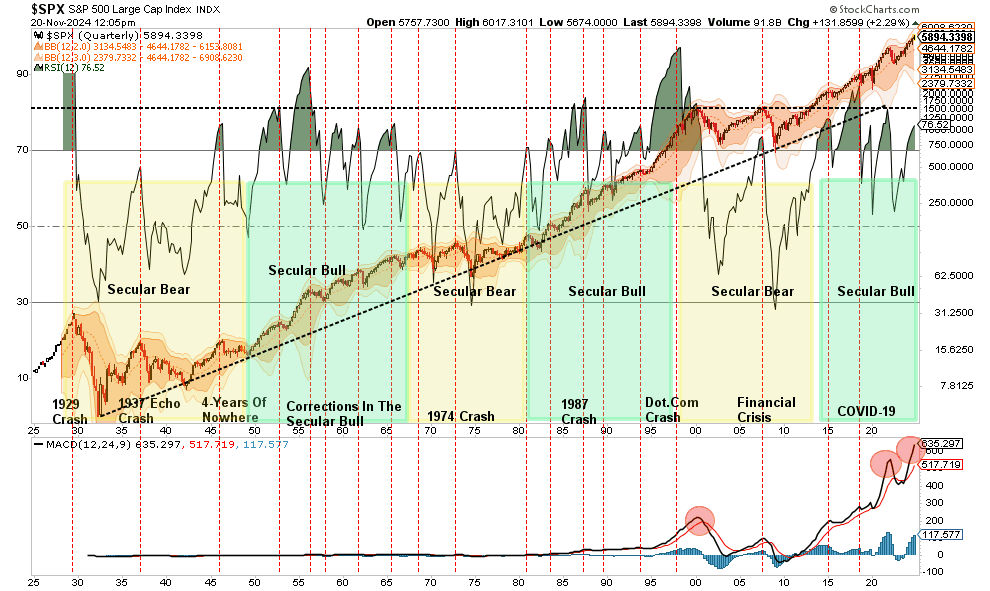

Furthermore, the technical backdrop is also very similar to previous market peaks. While the “permabulls” and Wall Street analysts are rushing to “out-predict” the other guys, it is worth noting:

- Markets are pushing historic levels of extreme overbought conditions,

- 2nd highest level of valuation on record,

- Extreme deviations from long-term growth trend lines,

- Investor sentiment and confidence pushing extreme bullishness, and

- Investors fully committed to the market with low levels of cash.

In other words, after 15 straight years of a bull market advance, The “risk” of something derailing continued optimistic expectations has risen significantly.

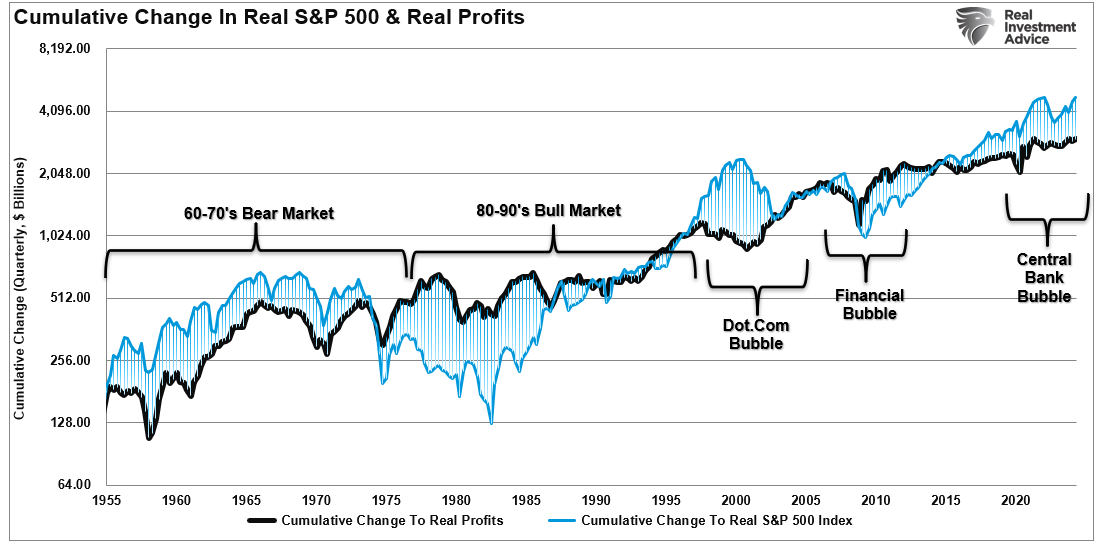

Corporate Profits As A Percent Of GDP

Secondly, as discussed recently in the Kalecki Profit Equation, corporate profits are extremely elevated as a percentage of GDP. As noted in that article:

“Valuations are high, partly because investors assume elevated profit margins will persist. However, the cumulative change of the inflation-adjusted price of the market significantly exceeds the profits being generated. Previous such deviations have not ended well for investors, and that is was the Kalecki equation suggests.”

If economic conditions worsen or fiscal policies tighten, we could see a significant reset. Earnings projections would likely be revised downward, dragging down equity prices. As James Montier suggested, long-term returns for U.S. equities look grim even under optimistic assumptions. He noted that price-to-earnings ratios reflect these outsized profit margins, leaving little room for error.

However, as stated, those profit margins rely on the government’s continued running of deficits, which brings us to our third point.

A Focus On Deficit Reductions

The new Trump administration is focused on deficit reductions, from the Department of Government Efficiency (DOGE) to the nomination of Scott Bessent as Treasury Secretary, who is a fiscal hawk. Both of these actions look to cut roughly $2 trillion from the deficit, which, while helping to provide long-term economic stability, will not come without short-term pain.

For the markets, “Government savings,” as discussed in the linked article on profits above, negatively affect corporate profitability. Those cuts will lead to higher unemployment and slower economic growth.

The offset will be the Federal Reserve working with the Treasury Department to restart “Quantitative Easing” and cutting interest rates dramatically lower as economic growth and inflation fall, pushing toward a recession.

Conclusion

Navigating the markets requires balancing optimism with caution and adaptability. While bull markets tend to dominate history, bear markets are sharp reminders of the risks of complacency. Labeling investors as “permabulls” or “permabears” oversimplifies the complexities of portfolio management, which requires responding to evolving market dynamics.

We’ve been bullish recently, but historical indicators and emerging risks—such as market exuberance, elevated profit margins, and potential fiscal tightening—suggest increased caution may be warranted in 2025. The goal is not to predict every market move but to prepare for shifts in risk and reward. This approach has helped us navigate past cycles, even if we’ve occasionally made missteps.

Investors should focus on maintaining a disciplined strategy, diversifying risk, and watching for signs of change. Being neither overly bullish nor bearish allows for greater flexibility in protecting and growing capital over the long term.

More By This Author:

Britain And European Economic Growth Sputters

Trump Election Sends NFIB Optimism Surging

Economic Indicators And The Trajectory Of Earnings

Comments

Log in or sign up to join the conversation.