Image: Bigstock

We get into the heart of the Q4 earnings season this week, with more than 250 companies on deck to report quarterly results, including 86 S&P 500 members.

By the end of this week, we will have seen quarterly results from about 28% of all S&P 500 members and will have a very good sense of whether the earnings-cliff narrative has started unfolding or been further pushed out.

This narrative suggests that the combined effects of softening demand resulting from the extraordinary Fed tightening and persistent cost pressures will prompt management teams across many industries to provide downbeat guidance. Related to this fear is the view that current earnings estimates remain elevated and need to get cut significantly to get in-sync with the unfolding economic ground reality.

Regular readers of our earnings commentary know that we don’t subscribe to this view. We see the ‘earnings-cliff’ type of world unfolding only in the backdrop of the U.S. economy heading towards a ‘hard landing’.

We see the risk of such a ‘hard landing’ as increasing if the Fed persists in its tightening policy beyond what the market has already priced in. But a hard landing for the U.S. economy isn’t our base case, which makes us a lot more sanguine in our earnings outlook given how much estimates have come down already.

We find the Q4 results thus far, admittedly a small sample that is weighted towards the Finance sector (11% of S&P 500 members have reported) as largely good enough, reassuring, and in-line with our overall view of corporate profitability.

We are starting to see some early signs of weakness in the consumer, with the Proctor & Gamble (PG - Free Report) ) report indicating some pushback to the company’s ability to keep raising prices and the Discover Financial (DFS - Free Report) ) report indicating that households may be starting to have difficulty paying back their bills.

Proctor & Gamble experienced -6% decline in sales volume, the biggest in years, even as the +10% price increase during the quarter helped offset the impact of softer unit sales. The -6% decline in sales volume in 2022 Q4 followed -3% decline in the preceding period and -1% decline in 2022 Q2.

For Q4, Proctor & Gamble’s earnings dropped by -6.9% from the year-earlier period on -0.9% lower revenues. Proctor’s numbers likely provide us with read-through for Kimberly Clark (KMB - Free Report) ), Johnson & Johnson (JNJ - Free Report) ), and others that are on deck to report results this week.

Discover Financial handily beat Q4 earnings and revenue estimates, but the card issuer offered disconcerting guidance for the net charge-off (NCO) rate for 2023. Broadly speaking, the charge-off rate is the proportion of the lender’s loan portfolio that it expects to be delinquent. Discover’s 2022 Q4 charge-off rate of 2.13% was up from 1.37% in the year-earlier period. Discover guided towards NCO rate in the range of 3.5% to 3.9% in 2023. It will be interesting to see if this week’s Synchrony Financial (SYF - Free Report) ) report will validate these credit-quality trends.

2022 Q4 Earnings Season Scorecard

Including results from all the banks, we now have Q4 results from 55 S&P 500 members, or 11% of the index’s total membership. Total earnings for these 55 index members are down -10.8% from the same period last year on +7.4% higher revenues, with 67.3% beating EPS estimates and an equal proportion beating revenue estimates.

With 86 index members on deck to report Q4 results this week, we will have seen results from 141 index members or 28% of the index’s total membership.

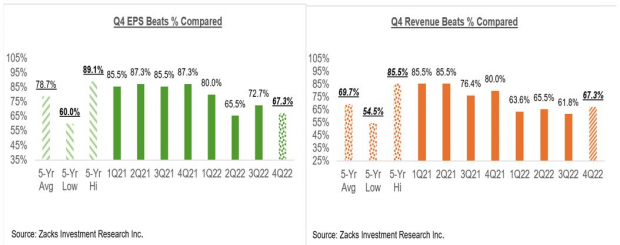

The comparison charts below put the EPS and revenue beats percentages in Q4 in a historical context.

Image Source: Zacks Investment Research

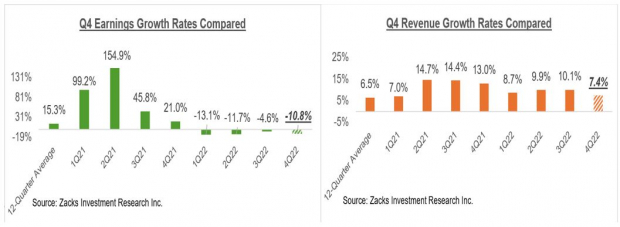

The comparison charts below put the earnings and revenue growth rates in Q4 in a historical context.

Image Source: Zacks Investment Research

The Earnings Big Picture

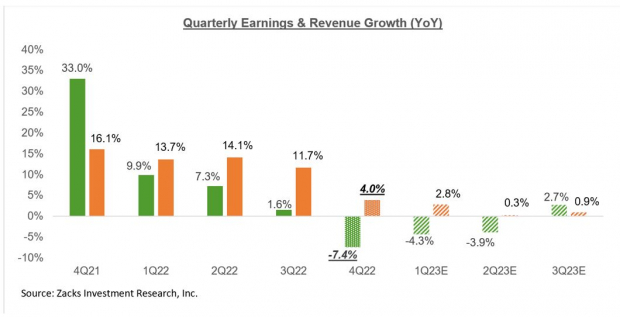

The chart below shows the expected 2022 Q4 earnings and revenue growth in the context of where growth has been in recent quarters and what is expected in the next few quarters.

Image Source: Zacks Investment Research

The chart below shows the overall earnings picture on an annual basis.

Image Source: Zacks Investment Research

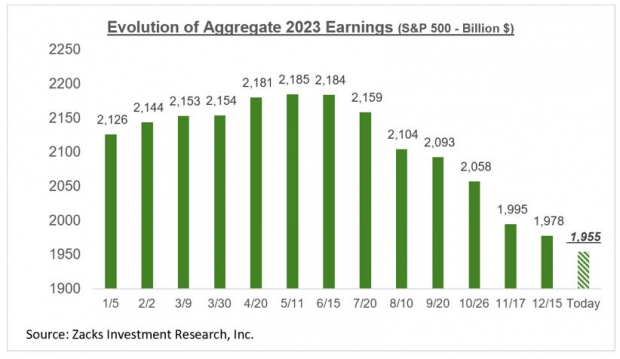

Estimates for 2023 have been steadily coming down, as we have been flagging for some time now. You can see this in the chart below that shows how the aggregate earnings total for the index has evolved since the start of 2022.

Image Source: Zacks Investment Research

Please note that the $1.955 trillion in expected aggregate earnings for the index in 2023 approximate to an index ‘EPS’ of $220.02, which compares to $216.89 in 2022.

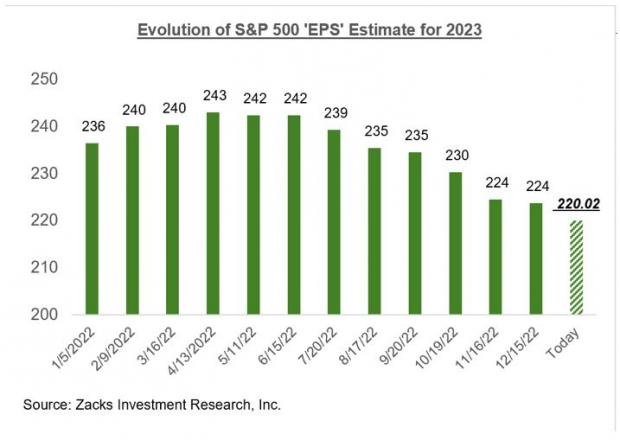

The chart below shows this index ‘EPS’ has evolved since the start of 2022.

Image Source: Zacks Investment Research

From their peak in mid-April 2022, S&P 500 earnings estimates have been revised down by -10.2% for the index as a whole and by -12.3% on an ex-Energy basis, with much bigger cuts to estimates for the Construction, Consumer Discretionary, Retail, Tech and Aerospace sectors.

More By This Author:

Plenty Of Positives In Big Bank Earnings: What's Next?

Have Earnings Estimates Come Down Enough?

Are We Headed For An Earnings Cliff?

Comments

Log in or sign up to join the conversation.