Image Source: Pexels

Intel (Nasdaq: INTC) is back in the headlines. In just a few weeks, the company has attracted major attention: SoftBank invested $2B at $23 per share, and Bloomberg reported the U.S. government may even take a 10% stake.

These moves, paired with Intel’s push to reset its strategy, have investors asking – are we seeing the start of a comeback, or just another chapter of volatility for a company that has stumbled before?

Intel is no longer positioning itself as just a PC and server chipmaker. It wants to be a full stack player in semiconductors, AI, and foundry manufacturing, key areas tied to U.S. national security and chip independence. SoftBank’s backing and possible U.S. government involvement suggest Intel’s role could extend far beyond competing with AMD and Nvidia (NVDA).

Still, the excitement comes with caveats. Intel is financially strained, carrying heavy debt, negative free cash flow in recent years, and profitability that trails its peers. The stock’s depressed valuation means upside could be large if execution improves – but that’s a big “if”.

Investors should keep three risks in mind. First, execution: Intel has a history of delays, and delivering its 18A node on time is critical. Second, competition: AMD, ARM, and Nvidia are all stronger than ever in their respective markets. Third, politics: government support looks positive now but could change quickly with shifting leadership or policy. These risks explain why, despite the surge, many investors are asking if it’s still too early to buy.

So where does this leave investors today? Let’s map it using the IDDA (Capital, Intentional, Fundamental, Sentimental, Technical).

IDDA Point 1 & 2: Capital & Intentional

Before investing in INTC, ask yourself:

Do you want exposure to one of the largest chipmakers in the world, with strong PC/server share and potential government backing?

Do you believe Intel’s foundry reset, Panther Lake launch, and push into AI can restore credibility and create new revenue streams?

Are you comfortable with Intel’s current financial weakness, betting that external support (SoftBank, government) plus execution can drive a turnaround?

Intel’s history has been defined by volatility. It fell behind competitors due to missteps, losing credibility with investors and customers. Today, it trades at depressed valuations where its P/S ratio is far below the sector average, and expectations are already very low. That creates an asymmetric setup: limited downside since failure is priced in, but large upside if Intel proves it can execute.

If you buy into Intel’s “strategic national asset” thesis, the risk/reward could be compelling. But if your tolerance for political drama, execution delays, and competition is low, the safer choice may be to watch from the sidelines until Intel shows consistent progress.

IDDA Point 3: Fundamentals

Intel is still financially weak. Its foundry business, which makes chips for other companies, has shrunk to only about 1% of the market. By comparison, TSMC holds a massive 67%. Years of poor management, delays in new chip technology, and building too much capacity have left Intel with unused factories, shrinking profit margins, and recent losses of over $20B in the past year. Its gross profit margin is just 33%, far below the industry average of around 50%. In simple terms, Intel looks more like a struggling chipmaker than a strong competitor to AMD or Nvidia.

Intel is in a tough financial spot, with $22.1B in cash but $50B in debt and no free cash flow since 2022, after once generating over $10B annually. To cope, it cut its dividend, sold off noncore businesses, and is leaning on partners and potential government incentives to help fund its heavy investments in new chip manufacturing. While this investment phase will likely keep pressure on its finances in the near term, a successful execution of its manufacturing plans could help Intel recover within the next two to three years.

However, the stock’s low valuation creates an opportunity. Intel trades at a P/S (price-to-sales) ratio of 1.78, much lower than its historical average of 2.42 and the tech sector median of 3.13. This means a lot of bad news is already priced in. If Intel can show even small improvements, the stock could rise significantly.

To turn things around, Intel has set three big goals: rebuilding its foundry business, launching its new Panther Lake processors on the 18A chip node, and moving into full-stack AI solutions. If these work, Intel could become important not just in chips, but also in AI, defense, and national security.

The foundry reset is key. Intel is now only expanding production when it has signed contracts from customers. This reduces the risk of overbuilding and helps rebuild trust in its reliability. Panther Lake, expected later this year, will be the first processor built on the 18A node. This advanced chip design could also be used in defense and government projects, making it even more valuable. On top of that, Intel is expanding into AI software and systems, which could improve profit margins by up to 30% and make customers more likely to stay with Intel long term.

Finally, Intel has gained a powerful backer. SoftBank recently invested $2B into Intel, which strengthens its finances and gives it more money to spend on its ambitious projects. This partnership also connects Intel to SoftBank’s wide network in AI and new technologies, further supporting Intel’s role as a long-term player in advanced computing.

Fundamental Risk: High

IDDA Point 4: Sentimental

Strengths

Intel is still one of the largest chipmakers, with strong positions in PCs and servers.

Its Products division remains profitable and innovative, and using TSMC for production could help stop market share losses.

Intel Foundry is one of only three companies capable of making cutting-edge chips, and extra financial support could make it a serious player.

Risks

Intel may fail to deliver on key manufacturing goals like the 18A chip in 2025.

AMD is now a stronger chip designer, and ARM-based CPUs are becoming a bigger threat.

Nvidia dominates AI chips, and Intel is unlikely to gain meaningful share in this fast-growing market.

Investor sentiment around Intel has been swinging back and forth. President Trump first criticized CEO Lip Bu Tan, then praised him days later, showing how unpredictable political support can be. Reports that the U.S. government may take a 10% stake have fueled optimism, suggesting Intel could be seen as too important to fail, similar to past government backing of MP Materials.

On top of that, SoftBank’s $2B investment, framed as a vote of confidence in U.S. tech leadership, sent shares up 5.3% after hours and boosted investor confidence. Still, unlike government deals with commodities, Intel must prove it can actually deliver advanced chips, meaning any failure in execution could quickly erase these sentiment-driven gains.

Sentimental Risk: High

IDDA Point 5: Technical

On the monthly chart:

Intel has been in a long-term downtrend since 2021, with sharp rebounds of up to 78% in between.

The future cloud remains wide and bearish, reinforcing the overall downward trend.

Candlesticks sit below the cloud, which continues to act as a resistance zone. This was tested in January 2024 when the stock rebounded but failed to break through, signaling that downward momentum is still in play.

Intel has been in a long-term downtrend since 2021, with sharp rebounds of up to 78% along the way. The stock remains below the Ichimoku cloud, which continues to act as a strong resistance zone. The future cloud is wide and bearish, reinforcing the weak long-term trend.

This was tested in January 2024, when Intel rebounded but failed to break above the cloud, signaling that downward momentum is still in play. The RSI is improving from oversold levels but hasn’t yet turned fully bullish.

(Click on image to enlarge)

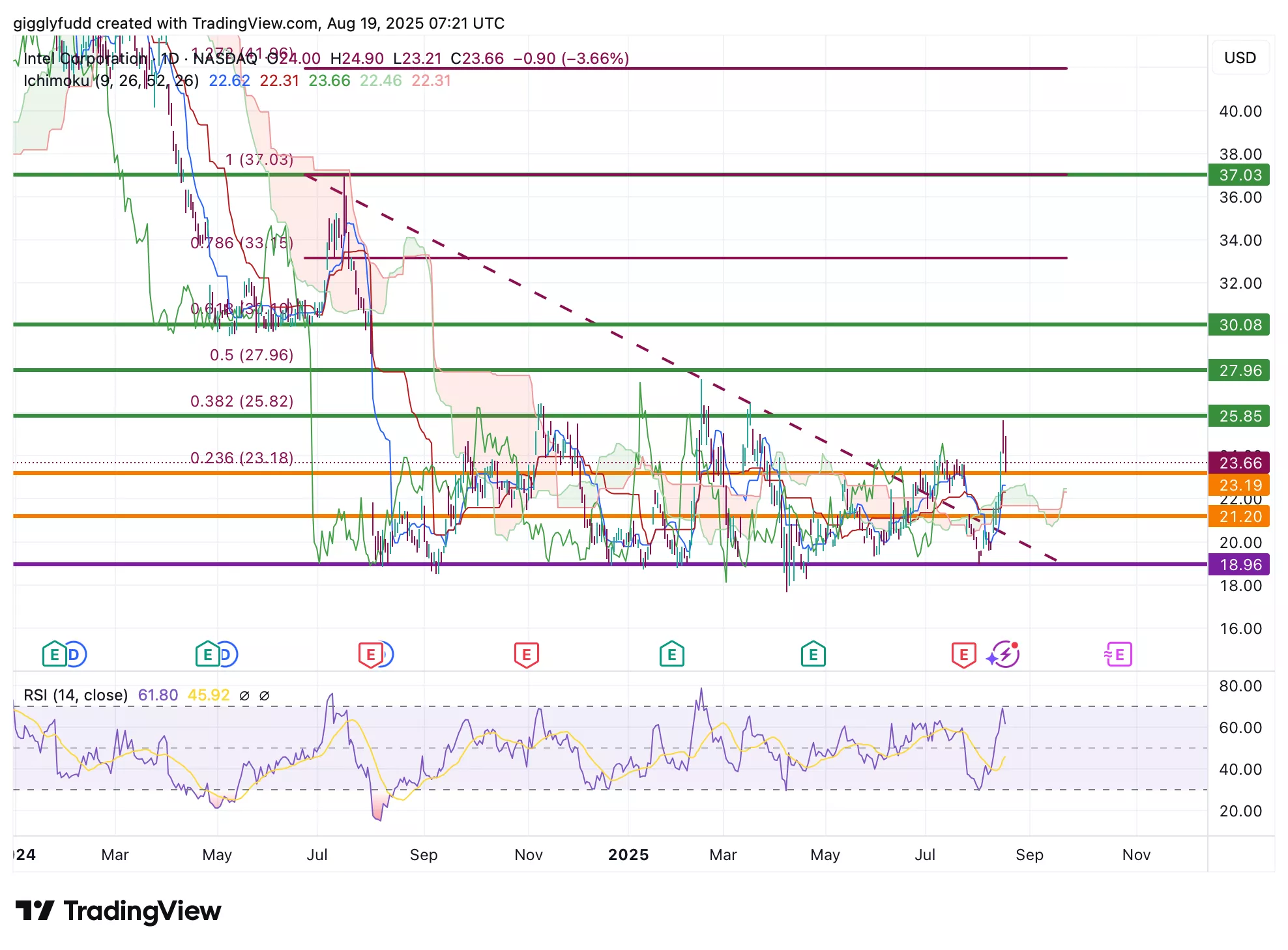

On the daily chart:

The pattern has been consolidating since the August 2024 plunge following a weak Q2 earnings report, with no clear signs of recovery.

Recent candlesticks are trading above the cloud, showing positive sentiment and momentum, with the future cloud turning slightly bullish but remaining flat.

RSI is near overbought at 61.80, suggesting a possible short-term pullback.

Intel’s daily chart shows the stock has been consolidating since its sharp drop in August 2024 after a weak Q2 earnings report, with recovery still uncertain.

Recently, the candlesticks have climbed above the cloud, showing improving sentiment and momentum, although the future cloud is still flat and only slightly bullish. The stock continues to move sideways in a range between $18 and $26. The RSI is currently near 62, pointing to positive momentum but also edging toward overbought territory, which could lead to a short term pullback.

Overall, Intel remains stuck in its range: holding above $22 keeps buyers in control, but a breakout above $26 would be needed to confirm a move higher toward $28 – 30. If there’s no breakout, then consolidation is likely to continue.

(Click on image to enlarge)

Investors looking to get into INTC can consider these Buy Limit Entries:

23.19 (High Risk)

21.20 (Medium Risk)

18.96 (Low Risk)

Investors looking to take profit can consider these Sell Limit Levels:

25.85 (Short term)

27.96 (Medium term)

30.08 (Long term)

Here are the Invest Diva ‘Confidence Compass’ questions to ask yourself before buying at each level:

- If I buy at this price and the price drops by another 50%, how would I feel? Would I panic, or would I buy more to dollar-cost average at lower prices? (hint: this question also reveals your CONFIDENCE in the asset you’re planning to invest in).

- If I don’t buy at this price and the stock suddenly turns around and starts going up again, will I beat myself up for not having bought at this level?

Remember: Investing is personal, and what is right for me might not be right for you. Always do your own due diligence. You should ONLY invest based on your own risk tolerance and your timeframe for reaching your portfolio goals

Technical Risk: High

Final Thoughts on Intel (INTC)

Intel is working to reinvent itself from a traditional PC and server chipmaker into a full-stack player in semiconductors, AI, and foundry manufacturing. Backing from SoftBank and potential U.S. government support position it as a strategic asset for America’s chip independence, but challenges remain with weak margins, past execution issues, and strong competition.

Still, the stock trades at a discount, and its core CPU business underpins much of its value, meaning progress in foundry or AI could create meaningful upside. Technically, the stock is still in a downtrend, consolidating in a range with resistance above and support below, showing signs of improving sentiment but not yet confirming a full reversal.

Key Takeaways:

Intel is a high risk, high reward opportunity. Support from SoftBank and potential U.S. government involvement provide some safety, but the company’s ability to execute will determine whether this becomes a genuine turnaround or just another setback. For investors willing to take on more risk, Intel appears undervalued with limited downside, but patience and confidence are essential, as a true recovery will only be confirmed once the stock can break through its major resistance levels.

Overall Stock Risk: High

More By This Author:

3 Things Investors Are Missing About Shopify Stock Right Now

UnitedHealth Stocks Biggest Test Yet: Why Buffett’s $1.57B Bet Might Prove The Market Wrong

MNDY Stock: The Truth Behind The Crash & What The Street Got Wrong

Comments

Log in or sign up to join the conversation.