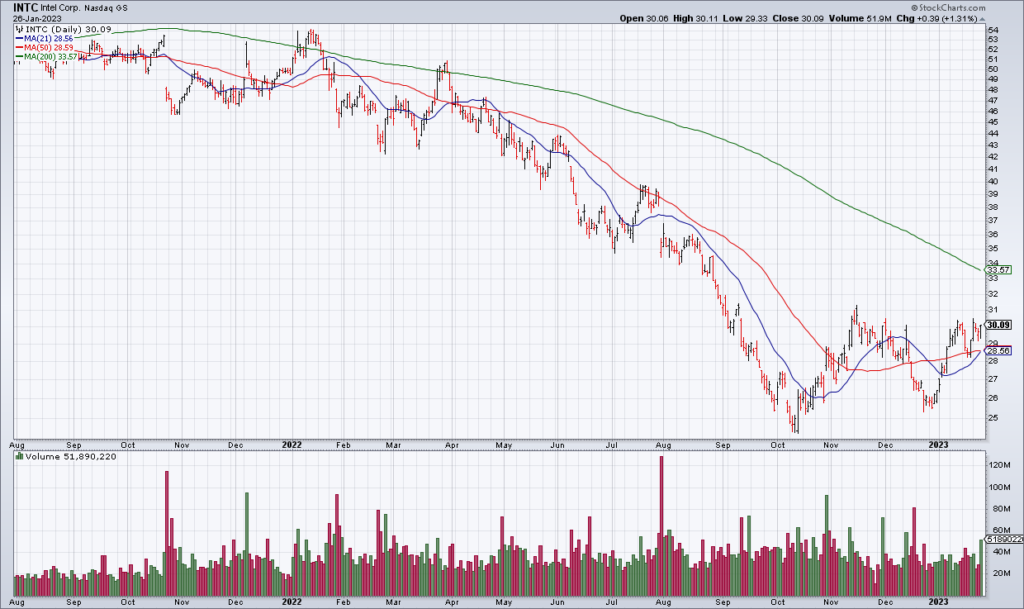

(Click on image to enlarge)

Intel (INTC) just reported a brutal 4Q22. Revenue was -28%, Gross Margin decreased by 1200 basis points and EPS was off 92% to 10 cents. And things are going to get worse. INTC guided 1Q23 revenue to $10.5-$11.5 billion – down 40% at the midpoint year over year. Gross Margin of 39% would be off 1410 basis points. And they are expecting a 15-cent EPS loss.

As a result, shares are currently -10% in the after-hours. Clearly, I was too early when I recommended INTC earlier this month. Thankfully I sold the small position I bought for clients and myself last week.

More By This Author:

KMB’s War For ‘Poop Superiority’, NOC Earnings

COF Confirms Consumer Credit Stress

Stocks Run Up Into Earnings Season As The Fed Considers Pausing

Comments

Log in or sign up to join the conversation.