Goldman Sachs has been vocal over the last week or two, making a good case for the Fed to cut rates as soon as the July 31st FOMC meeting. Goldman Sachs strategist Jan Hitzius was quoted as follows:

While September remains our baseline, we see a solid rationale for already cutting in July. If the case for a cut is clear, why wait another seven weeks before delivering it?

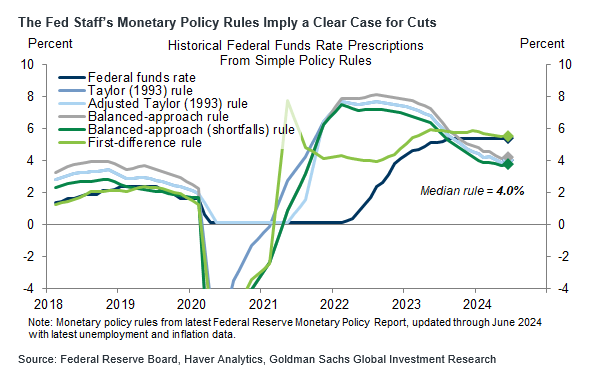

The graph below also from Goldman Sachs shows that many monetary policy rules the Fed tracks imply that Fed Funds are, on average, about 1.25-1.50% too high. Moody’s seems to agree with Goldman Sachs. In a recent statement, they say:

The Fed could begin policy easing with a 25 basis point cut as early as in the upcoming 30-31 July meeting.

While we believe there is a good case for rate cuts, it still appears the Fed wants to wait for more economic data. Thus, a September hike is the most likely date for the first rate cut. However, history shows the Fed can change its mind quickly. In June 2019, the Fed said it would not cut rates until 2020. They lowered the Fed Funds rate in the following month (July).

What To Watch Today

Earnings

Economy

Market Trading Update

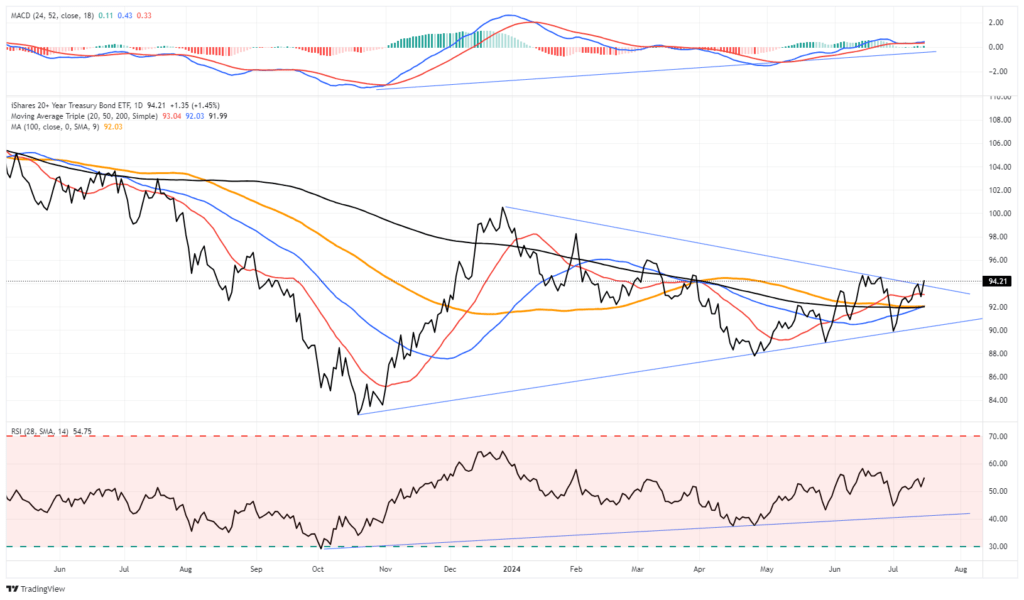

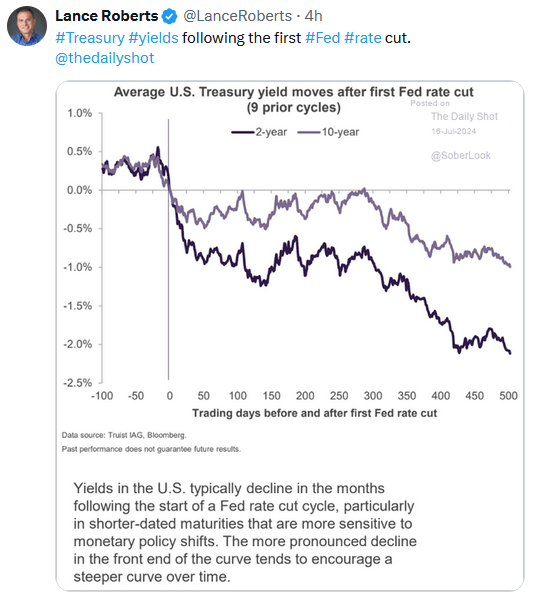

Yesterday, we discussed the small and mid-cap trade, which has become very extended and overbought very quickly. That performance rotation from large caps to the Russell 2000 index continued yesterday, spurred by a decline in interest rates.

The bond market has continued to improve technically for quite some time now. In contrast, many market participants continue to shun longer-duration bonds due to misguided information on how the bond market works. On a technical basis, the price action since October has been solidly bullish. Higher bottoms in price and a rising trend in relative strength suggest buyers are accumulating positions. Most notably, bond prices have cleared all their major moving averages and are trying to break above the current downtrend line.

(Click on image to enlarge)

As discussed yesterday, with expectations rising, the Federal Reserve will cut rates; the reduction of rates on the front end of the curve, along with slowing economic growth, historically precedes a decline in longer-duration bond yields.

While bond volatility has not ended, the bullish trend in bonds is beginning to take shape. As discussed in that article, the risk to investors may lie with the stock market as Fed rate cuts historically collide with slower economic activity and a reduction in earnings growth.

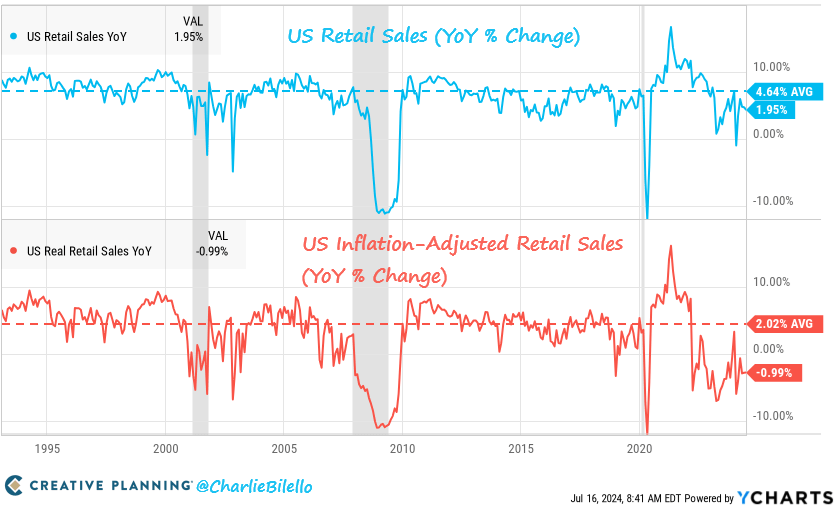

Retail Sales Are Weaker Than It Appears

Retail sales came in at 0.0%, which aligns with the consensus. Additionally, last month’s figure was revised from 0.1% to 0.3%. The data continue to point to weak personal consumption. The graph below from Charlie Bilello shows that retail sales are tracking well below the historical average. Further, they are down 1% on an inflation-adjusted basis. More troubling is the following quote from David Rosenberg:

If you were rubbing your eyes as I was over that retail sales report, I think I found the answer. A very generous seasonal adjustment factor was at play. The raw NSA data actually showed retail sales plunging -5.6% MoM in June, the worst drubbing in a decade and tied for the steepest plunge since the series began in 1992! Lies, damned lies, and statistics.

Advice From Howard Marks, A Value Investor

Passive investing is the rage these days, but active investment strategies exist and will likely thrive one day. As such, we thought we would share some of the logic of Howard Marks, one of the most successful value investors. Marks is the chairman and one of the founders of Oaktree Capital Management. Over his 40 years of investing experience, he has had much success. Furthermore, he shares his market and economic thoughts with the public. You can find 35 years of his archived Memos HERE.

The following are a few choice quotes from his book The Most Important Thing:

If we avoid the losers, the winners take care of themselves.

Understand the psychology of the investor- greed, fear, ego, biases, and envy.

The investor’s job is to take risks intelligently. Doing it well separates the good investor from the rest.

Markets swing like pendulums.

Without an accurate estimate of intrinsic value, any hope for consistent success as an investor is just that: HOPE.

Investment success doesn’t come from “buying good things,” but rather from “buying things well.”

Tweet of the Day

More By This Author:

The UM Sentiment Survey Confirms Consumer JittersFed Rate Cuts – A Signal To Sell Stocks And Buy Bonds?

The Credit Widening In The Coal Mine

Comments

Log in or sign up to join the conversation.