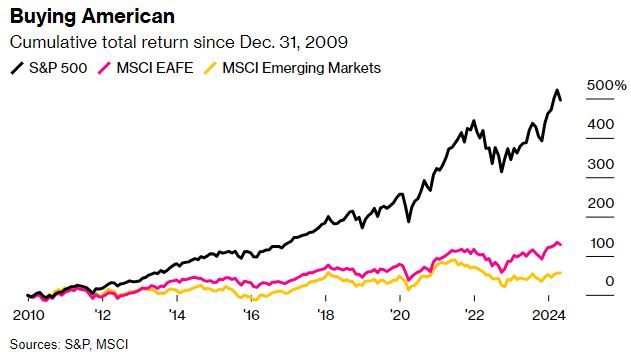

The chart below suggests that global diversification could be dead. The S&P 500 notched a total return of 13.3% annually over the past 15 years, while the MSCI EAFE and MSCI Emerging Markets indices returned 5.9% and 3.2% per annum respectively. The performance gap primarily stems from differences in earnings growth. S&P 500 earnings grew 14.1% annually over the past 15 years, while developed international and emerging markets grew earnings of 10.6% and 2.9% per annum, respectively. In addition, the global market has afforded the S&P 500 higher P/E multiples since the global financial crisis- a reflection of both more confidence and higher growth expectations.

But is Global Diversification really dead? It hasn’t worked in over a decade, but a recent Bloomberg article postulates that the lack of global diversification in the post-GFC period is an exception rather than a new norm. From 1973 to 2009, earnings growth was 5.7% annually for both EAFE and the S&P 500. Valuation multiples grew at 0.9% annually in EAFE compared to 0.5% for the S&P 500. There used to be a semblance of parity between domestic and international stocks.

On top of that, since 2015, a handful of US companies have driven a large share of S&P 500 earnings growth. The Bloomberg Magnificent Seven Index has seen annual earnings growth of 36% since 2015, while the rest of the S&P 500 grew earnings by roughly 6% annually. Ultimately, the Author’s idea is that a mean reversion is likely. It’s certainly possible that global diversification isn’t dead, but it doesn’t mean the US is bound for underperformance. It could simply mean the S&P 500’s days of drastic outperformance are numbered.

(Click on image to enlarge)

What To Watch Today

Earnings

- No notable earnings releases today.

Economy

- The market is closed for Juneteenth. No data releases today.

Market Trading Update

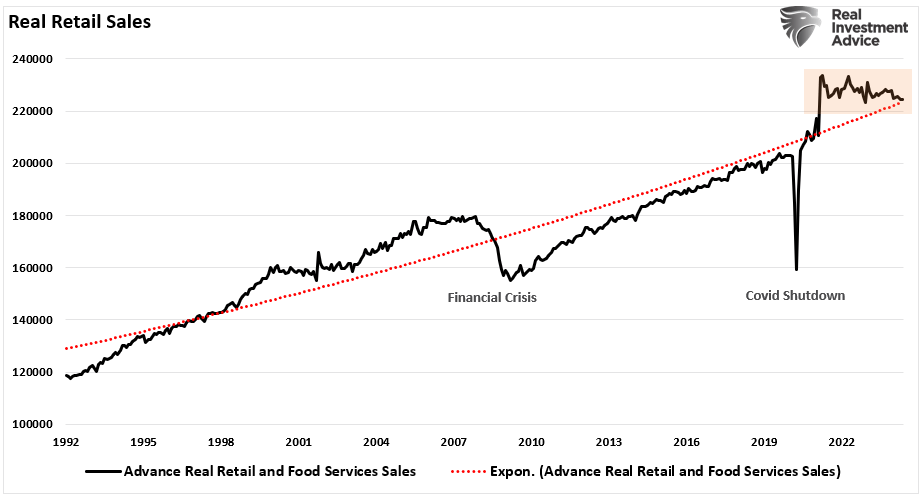

Tuesday, the market held somewhat firm despite a retail sales report that suggests the consumer is slowing down. Furthermore, the already weak April retail sales data was revised lower. Such is not surprising given some of the recent reports from retailers like Walmart.

(Click on image to enlarge)

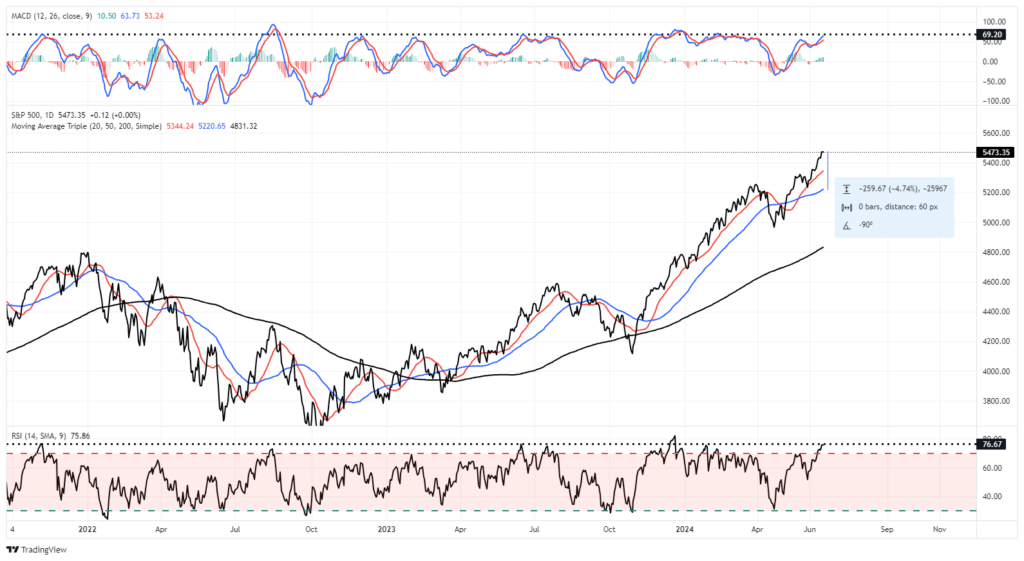

However, while weak economic data has been causing rather strong market rallies lately, increasing hope for Fed rate cuts, such was not the case yesterday. The reason is that following Monday’s rally, the market deviation from the 50-DMA is getting extreme. Furthermore, the market is very overbought, which limits the upside further. The Relative Strength Index is pushing limits that have previously marked short-term market peaks. A retracement to the 50-DMA would entail a roughly 4.5% decline, which, while not significant, will “feel” much worse given the high level of complacency. This is likely a good point to take profits, rebalance positions to target, and raise some cash as needed heading into quarter-end rebalancing.

(Click on image to enlarge)

More By This Author:

Mega Cap Valuations Are Dwarfed By Tesla

Consumer Survey Shows Rising Bullishness

Michigan Survey Shows Consumer Concerns

Comments

Log in or sign up to join the conversation.