Over the past few months, we have witnessed a decided deterioration in consumer spending. For instance, first-quarter sales from many large retailers showed little to no growth. Economic data like Q1 GDP and the recent retail sales report further confirm that personal consumption is slowing. Last Friday, the University of Michigan Consumer Sentiment Survey followed suit as it was much weaker than expected. In particular, as shown below, the University of Michigan’s current economic conditions survey fell sharply and is not far from record lows. Current conditions are 62.5. That compares to a prior reading of 69.6. Furthermore, the expectation was for the index to increase to 72.2. According to the University of Michigan, the average since 1951 has been 95.31.

With the boost in pandemic-related savings largely depleted, credit usage soaring, and irregular post-pandemic consumption behaviors finally normalizing, consumers no longer have the means or desire to overspend. While one’s financial situation plays a vital role in spending, sentiment is also a function of politics and inflation. The rate of inflation has come down, but the price of goods is still rising—and, importantly, they remain well above what consumers are used to. Regarding politics, other surveys have shown significant differences between what Republicans and Democrats think on economic issues. Because the election is nearing, some of those surveyed by the University of Michigan may be swayed by their politics.

What To Watch Today

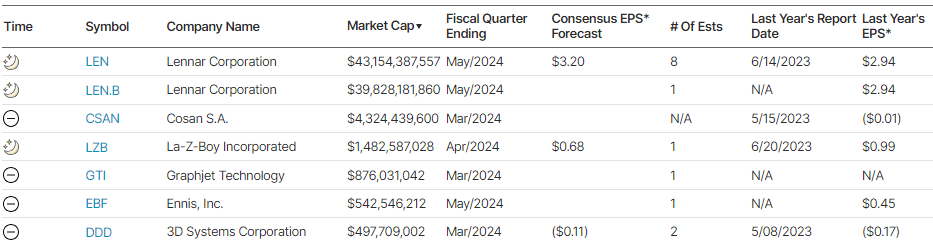

Earnings

Economy

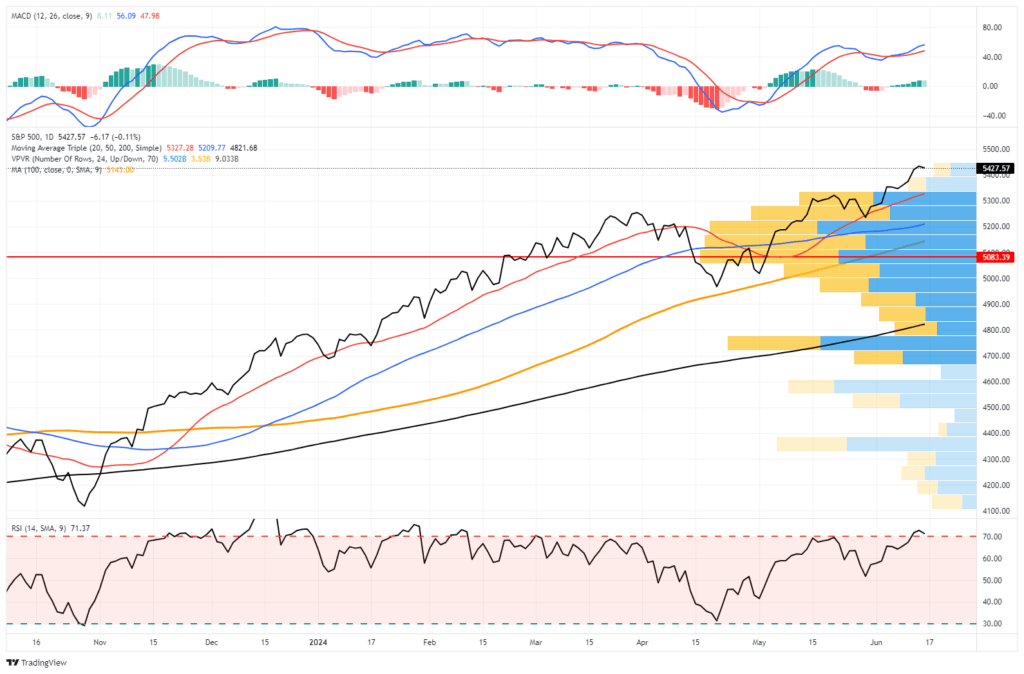

Market Trading Update

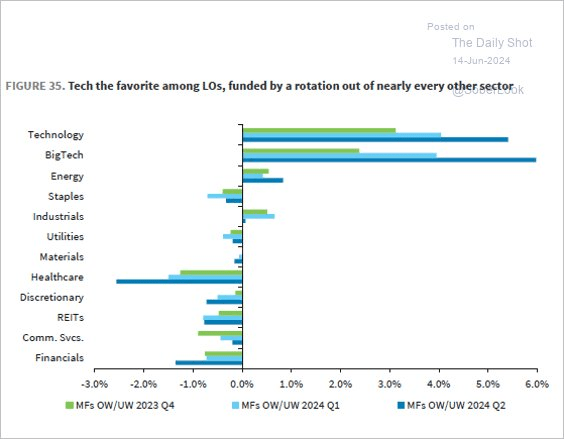

As noted on Friday, market breadth remains weak even as the market continues to push higher. Furthermore, investors are now primarily going “all in” on Technology and selling everything else. This kind of behavior has historically ended poorly, but irrational behavior can last much longer than logic predicts.

The economic data shows signs of weakness, which will likely feed into the Fed’s outlook for rate cuts over the next few months. While the market remains oblivious to the diversion between economic realities and Wall Street exuberance, such will eventually reconnect. However, for now, as we enter a new trading week, there is little standing in the way of the bulls momentarily. The market remains on a buy signal, and while short-term overbought, corrections should be contained by the 20-DMA. For investors, adding risk exposure on dips remains a logical strategy. However, that will eventually change.

The Week Ahead

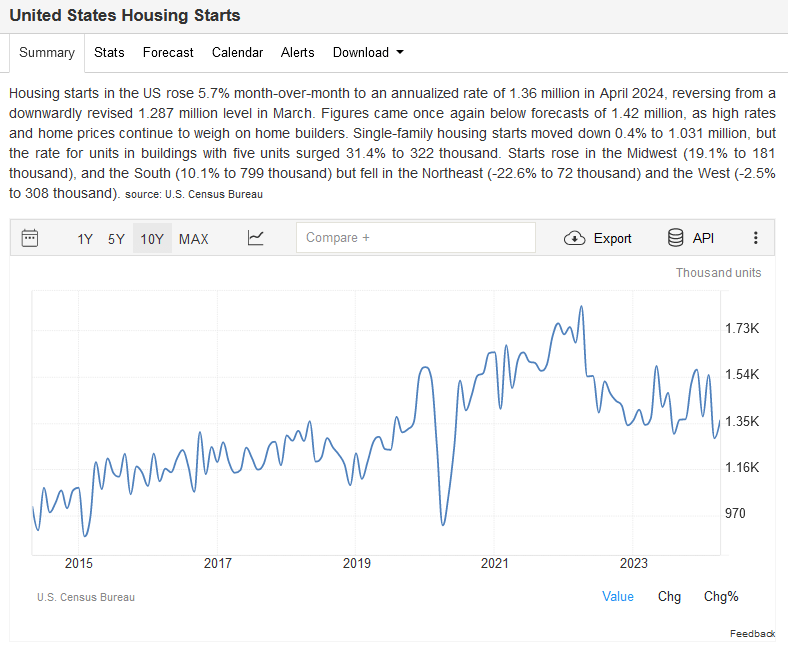

Retail sales kick off the economic calendar on Tuesday. As we led this commentary, will it show that consumers are retrenching? The current estimate is for a gain of 0.3% versus 0.0% last month. Building permits and housing starts will likely show that new construction of homes and multifamily properties is slowing rapidly. The graph below shows that housing starts have been trending lower for two years and are back to the peak of the pre-pandemic era. Building permits are now slightly below the 2019 highs.

With the FOMC meeting past, Fed members will be on the speaking circuit. It will be interesting to hear their views on recent data and if they are reconsidering the potential for a rate cut in July.

Many companies will enter buyback blackout windows as we are about a month away from Q2 earnings reports.

Macron’s Gamble Is Blowing Up Alongside French Markets

After Marine Le Pen and other right-wing parties pulled off stunning and decisive victories in the European Union elections a week ago, French President Emmanuel Macron made a bold political gamble. He dissolved France’s National Assembly and held snap elections. With the first round of voting occurring in only three weeks, he didn’t think there was enough time for his opponents to form alliances. Hence, they would struggle to win enough votes to advance to the July 7th runoff election. His plan, if successful, helps him secure the backing of a large block of voters in the National Assembly. It appears his plan is backfiring.

The most recent polls show Le Pen could garner about 270 seats in the 577-seat National Assembly. That would make Le Pen’s party, the National Rally, the biggest party in the lower chamber. Furthermore, it gives Le Pen a decent chance to become the next President in 2027 when Macron’s term ends and term limits preclude him from running again. Markets are uneasy with Le Pen’s victory. While Macron vows to hold on to his seat, markets are betting that his powers will be much more limited.

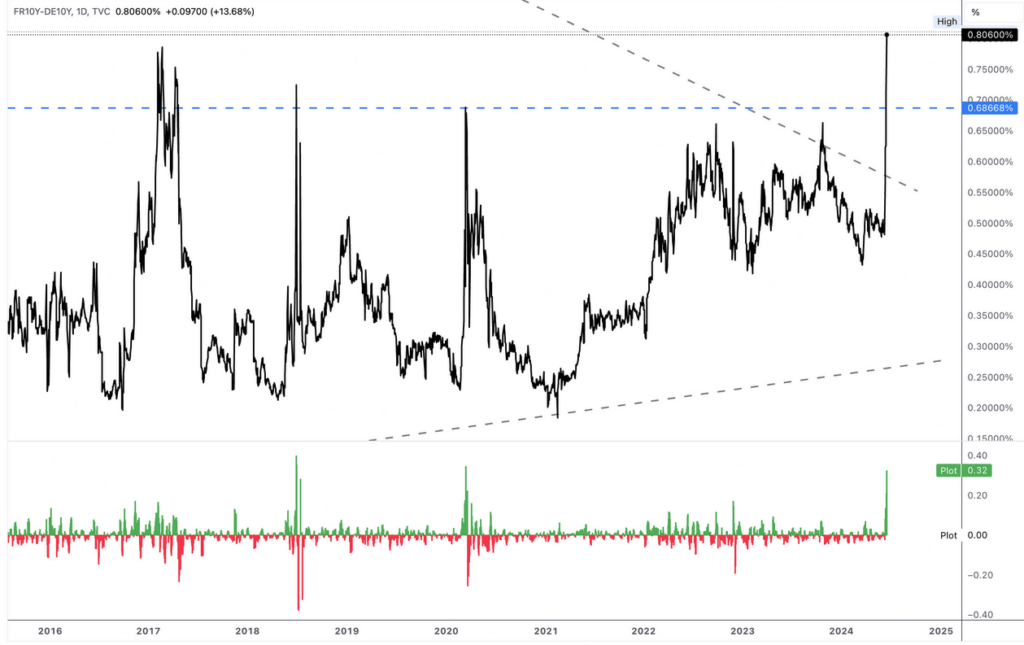

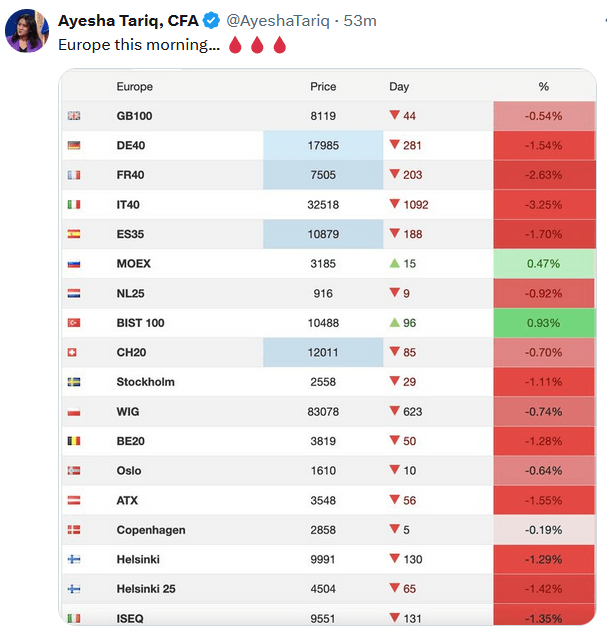

The first graph below, courtesy of SimpleVisor, shares information on EWQ, the U.S. ETF representing the primary French stock index, the CAC 40. It has fallen by about 8% in the last week while the S&P 500 continues to rally. The second graph shows that the yield on French bonds recently rose about 30bps versus German bonds. Lastly, as a result of right-wing gains in France and Germany, volatility in many European stock markets is increasing.

Tweet of the Day

More By This Author:

Cooler Inflation Print Sends Stocks And Bonds HigherGrant: Rates Are Going Much Higher. Is He Right?

Bad Market Breadth

Comments

Log in or sign up to join the conversation.