The month of December, 2024 compared to December, 2023:

| Type of Flow |

2024 |

2023 |

| Net-transfer (daily average) | +$62B |

+$63B |

| Nominal-spending (daily average) | $584B | $541B |

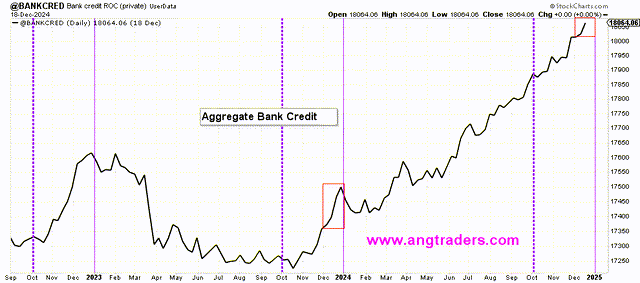

| Change in bank credit | +48B |

+$109B |

The net money-creation was lower this December than December 2023 (+$117B compared to +$178B). This was due to last December's bank credit increase (chart below).

The fiscal-2025 Q1, compared to the fiscal-2024 Q1:

| Type of Flow |

Fiscal-2025 |

Fiscal-2024 |

| Net-transfer (annualized) | +$620B (+$2,481B) |

+$394B (+1,576B) |

| Nominal-spending (annualized) | $1,891B ($7,564B) | $1,676B ($6,704B) |

| Change in bank credit | +$214B | +$231B |

Compared to fiscal-2024 Q1:

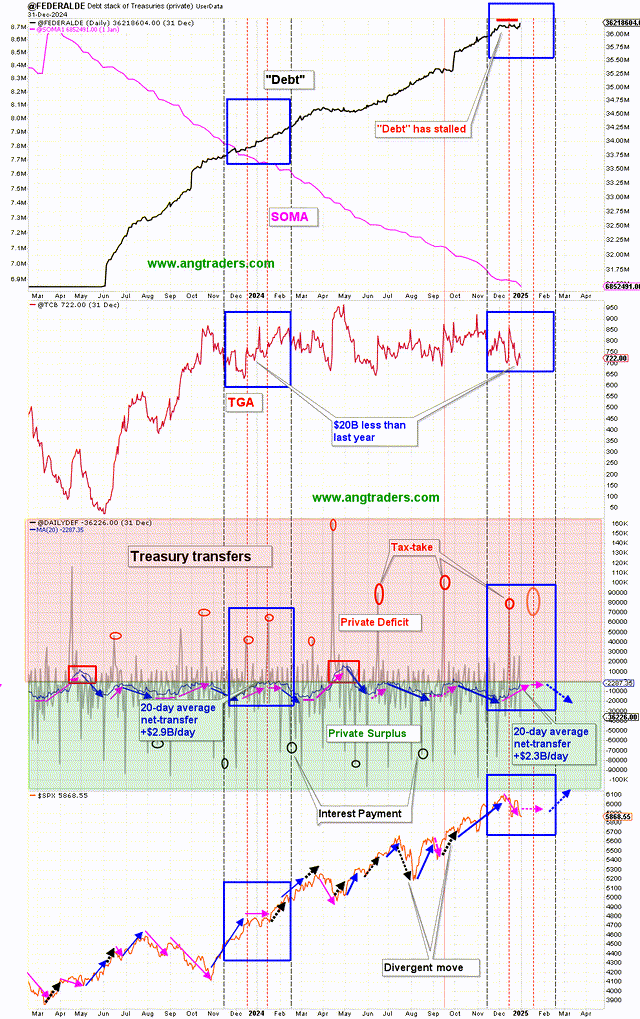

- The Treasury net-transfer is $226B higher than in fiscal-2024. (Nominal-spending is $215B higher.)

- The change in bank credit is $17B lower than last year.

- The Fed's IOR (interest on reserves) has paid $16.6B so far, which is $10B lower than last year (it was $26.4B last year).

- Total net money-creation is +$199B more than last year which continues to explain the SPX rally, but which has been decreasing during the month of December.

The average net-transfer (from the Treasury to the private sector) is decreasing according to the seasonal pattern (pink arrows inside the blue boxes). This tendency (lower net-transfer) should last until the mid-January tax-take. The SPX is likely to be in a trading-range until then.

More By This Author:

Dazed And Confused... About Money

Why The Bull Market Continues

Republican And Democratic Presidents, Which Is Better For The Economy And Stock Market?

Comments

Log in or sign up to join the conversation.