Bloomberg recently published “Wall Street Grapples With A New Risk: A European Buyers Strike.” The article notes that stock indexes in Europe, Japan, Canada, and South Korea are all beating US equities in both nominal and dollar terms. As a result, some European pension funds and other foreign buyers are trimming their exposure to US stocks. While US valuations are generally higher than in most other countries, the article also highlights rising geopolitical risk and concern over the “weaponization” of the dollar, prompting European and Asian buyers to rebalance away from US stocks. The two quotes below from the article are from European buyers:

“The problem stems from the US seemingly abandoning the rules-based international order it has previously supported, which means investors can’t trust the US dollar or investments going forward.”

— Lars Christensen, CEO, Paice

“This is really an environment where you don’t want to be all exposed to US equities or US assets, especially not the dollar.”

— Mathieu Racheter, Head of Equity Strategy, Julius Baer

While we have no doubt that tariffs, politics, and valuations are pushing some European buyers away from US equities, we want to stress that almost all investors’ first objective is to seek the best returns. So, in this light, consider the dollar index depreciated by 10% last year and gave up 14% against the euro. The graph below shows the stark difference in S&P 500 returns in dollars versus euros.

Last year, European and Asian buyers were better served in their domestic markets, which avoided losses on the dollar component of US-based assets. However, if the dollar starts appreciating and US equity indexes outperform global stocks, we suspect European buyers will be gung-ho to invest in the US, regardless of their political views.

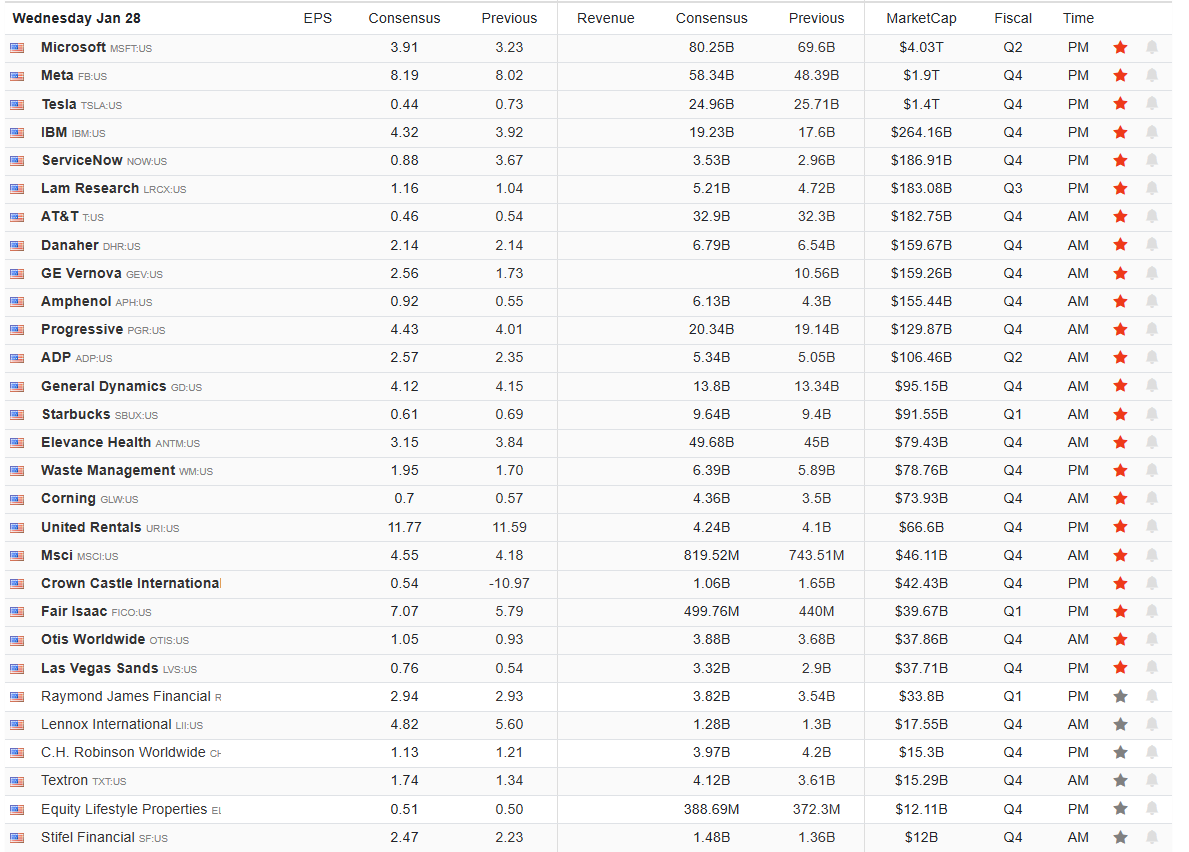

What To Watch Today

Earnings

Economy

(Click on image to enlarge)

Market Trading Update

Yesterday, we discussed the recent trades we made in the All-Weather Portfolio as part of an ongoing risk management process. Today, we get the first batch of mega-cap companies reporting earnings, with Microsoft, Meta, and Tesla reporting after the bell. On top of that news, the Federal Reserve will announce its latest policy actions, and the following press conference will provide clues for the market about further policy actions. In other words, there are plenty of things happening today that could well induce volatility risk tomorrow, so trade carefully.

The good news is that after today’s earnings announcements, the corporate share buyback window begins to reopen, which will provide additional support for the market. As noted yesterday, since 2011, corporate share buybacks have accounted for 27% of the S&P 500 index’s returns. Rather than the market trading near 7,000, it would be closer to 5,200, where total return would align more closely with the long-term averages.

Yes, buybacks are that important.

As John Authers pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting massive liquidity into the financial markets and corporations buying back their shares, there have been no other real buyers in the market.

More notably, while the media touts the strong earnings growth in the recent reporting periods, that growth would not have been possible without the surge in buybacks. The result is not surprising, given that the majority of earnings growth in the quarter came from the companies most aggressive with share repurchases. However, given current valuation levels, it should make one question precisely what you are paying for.

Lastly, many argue that buybacks have little to do with market movements; however, the high correlation between the 4-week percentage change in buybacks versus the stock market suggests otherwise. More importantly, since the act of share repurchases provides a buyer for those shares, the .85 correlation between the two suggests this is more than just a casual relationship.

With corporate buybacks on track to set a new record this year, approaching $1.2 trillion, stock support remains strong. The solid bars represent confirmed data, while the lighter-colored bars indicate forecasts for 2025 and 2026. As shown, the trend is steadily upward, with a record $982 billion in shares repurchased in 2024. This amount is expected to be surpassed in 2025 and 2026.

With valuations already elevated and earnings expectations very high, buybacks could be a very important support to keeping markets elevated this year. Of course, if anything happens to slow or reverse those buybacks, then outcomes could be very different.

While we remain bullishly biased and allocated to equities, we are certainly aware of the risks ahead. However, the importance of buybacks to overall market performance should not be dismissed, in either direction.

Health Insurers Fall On Medicare Payments And Earnings

The largest health insurers, including Humana (HUM), UnitedHealth (UNH), and CVS (CVS), fell sharply after the Center for Medicare and Medicaid Services (CMS) proposed holding payments to private Medicare plans flat next year. Per CMS administrator Mehmet Oz:

These proposed payment policies are about making sure Medicare Advantage works better for the people it serves

Given that President Trump has been increasingly facing criticism for affordability issues, this action should not have been totally unexpected. Moreover, on numerous occasions, Trump has noted how much money insurance companies are making.

Further pressuring health insurance stocks were UnitedHealth’s (UNH) earnings. They are forecasting a decline in 2026 revenue, the first annual decline in more than three decades. The company reported better-than-expected earnings, but according to Bloomberg: “the company’s medical-loss ratio, a closely watched gauge of care expenses, was slightly worse than Wall Street expectations.” The weak outlook, coupled with the CMS decision, makes the road ahead for UNH murky. As we share below, the stock opened 18% lower on the news.

(Click on image to enlarge)

Tweet of the Day

More By This Author:

Do Sentiment Trends Boost Reflation OddsThe Bullish And Bearish Case For 2026

The Reflation Narrative Stumbles Out Of The Gate

Comments

Log in or sign up to join the conversation.