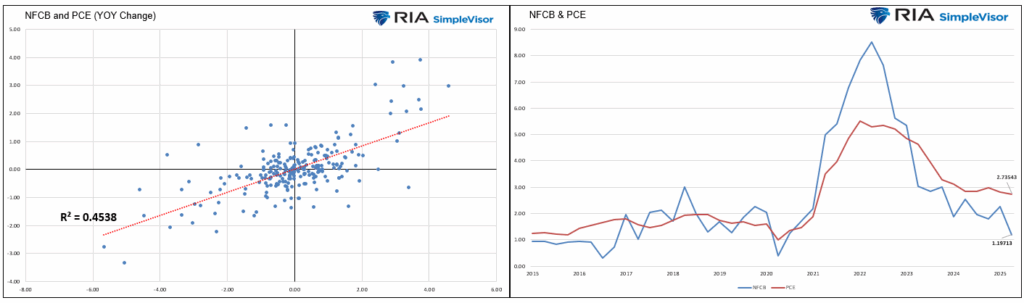

The following discussion is courtesy of Paul Mortimer Lee, as provided by Albert Edwards of Societe Generale. Paul makes an interesting case that PCE prices, the Fed’s primary gauge of inflation, are likely to decline. Supporting his view is a relatively wide and growing gap between the prices witnessed by the non-financial corporate business sector, also known as NFCB, and the personal consumption expenditures (PCE) price gauge. The NFCB measures the change in prices experienced by the corporate sector. As shown below on the right side, NFCB is running at 1.19%, well below PCE prices.

NFCB tends to lead PCE because shifts in corporate investment, hiring, and prices usually reflect management’s expectations about future demand. Given that corporate executives tend to be more aware of business cycles, economic changes, and price trends than consumers, their actions often occur well before the average consumer alters their spending patterns.

Paul explains that NFCB and core PCE inflation “normally move closely together,” indicating that when one rises or falls, the other tends to follow suit. The graph on the left confirms the existence of a statistically significant correlation, supporting Paul’s logic. It’s worth noting that the current gap supports the fact that corporate profit margins are larger than usual, as corporate price inflation is less than consumer price inflation. However, if weakness in personal consumption persists, it will likely compel companies to reduce prices, thus sacrificing profit margins to help maintain revenue and market share. Such actions, in aggregate, would likely reduce or eliminate the corporate versus consumer price gap, as Paul theorizes.

Paul’s conclusion is as follows:

Inflation generated by the non-financial business sector has stabilized at a level significantly below the 2% target, and we should expect the rate of increase in the core PCE to converge on that target over time.

What To Watch Today

Earnings

(Click on image to enlarge)

![]()

Economy

- No economic releases today.

Market Trading Update

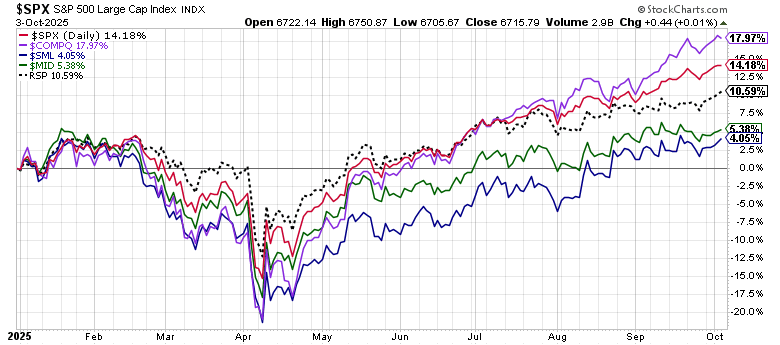

Entering October’s first complete trading week, markets remain perched near all-time highs despite stretched internal signals and a thinning data environment. The S&P 500 closed at ~6,715 on Friday, with the front-end resistance zone holding firm at ~6750 and the upper end of that band. Its 50-day and 200-day moving averages lie well below, anchoring the bullish trend and underscoring how far the price has diverged from its trend base.

(Click on image to enlarge)

Volatility has begun to stir. The VIX has climbed into the mid-teens to near 17 range, departing from the ultra-low complacency levels of recent months. That uptick suggests increasing demand for hedges, even before a sustained pullback emerges. Momentum indicators, including RSI and MACD, remain in a negative divergence from rising prices, which is also a classic sign that upside is becoming harder to sustain.

Breadth remains a concern. The rally is narrow: gains are concentrated among mega-cap and tech/momentum names, while mid- and small-cap segments lag. The equal-weight index underperformance versus cap-weighted benchmarks continues to warn of structural fragility. Meanwhile, due to the government shutdown, the lack of fresh macro data gives technical levels and sentiment flows more influence than usual.

In this environment, support and resistance zones are of oversized importance. Near-term support is established in the 6,570-6,627 range (a zone where past pullbacks found buyers). If sentiment sours, more support is potentially down toward ~6,500 (the 50-DMA). Resistance remains at this past week’s highs at ~6,750. A sustained break below support would invite more aggressive downside targeting. However, a move above recent highs will keep speculative activity alive.

Outlook: Bullishly Cautious. The trend is still intact, but the margin for error has narrowed. Given the confluence of valuation stress, narrow leadership, rising volatility, and a data blackout from the shutdown, we should expect more frequent and sharper intraweek swings. Any technical breach, especially a breakdown through support zones, would likely catalyze larger moves given the stretched state of positioning. Caution and tighter risk control are prudent as the market navigates this tension zone.

The Week Ahead

It could be a quiet week if the government remains closed and no government economic data is released. However, if Congress reaches a resolution, we can expect the BLS report to be released within a few days of the agreement being reached. On Wednesday, the FOMC will release its minutes from its meeting three weeks ago. We will be interested in seeing if there was much debate regarding raising rates by 25 basis points versus 50 basis points. The Treasury will auction ten-year notes on Wednesday and 30-year bonds on Thursday. Expect some volatility in the Treasury market leading up to the two actions.

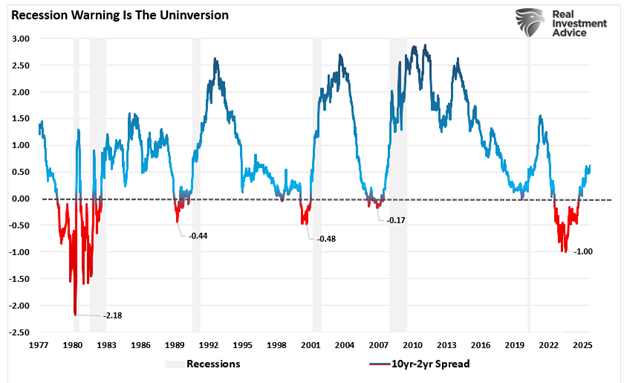

Promised Recession: So Where Is It?

Over the past three years, the economic conversation has been a “promised recession.” If you read the headlines, tracked economist surveys, or even listened to Wall Street strategists, you would have assumed a downturn was imminent. Many investors, bloggers, and YouTubers have had a “parade of horribles” promising a recession is just on the horizon.The logic was simple enough. The Federal Reserve aggressively hiked rates from near zero, inflation spiked to four-decade highs, the yield curve inverted for the longest stretch on record, manufacturing surveys collapsed, and stocks entered a bear market in 2022. Historically, those conditions have been reliable precursors to economic pain.

And yet, here we are, late into 2025, and the U.S. economy is still standing. Not only standing, but GDP remains broadly positive, unemployment is relatively low, and equity markets sit at record highs. If the “promised recession” were near, none of that would be the case, and for many investors, the “recession that never came” has been one of the great surprises of this cycle.

But does that mean we’ve escaped it altogether? Or is the downturn still lurking, delayed by policy distortions and fiscal largesse?

Tweet of the Day

More By This Author:

Bear Market Losses – A Dangerous IllusionBubble In AI: Echoes Of The Past, Lessons For The Present

Eli Lilly And Its Competitors Pop On The Pfizer News

Comments

Log in or sign up to join the conversation.