Image Source: Pexels

Market Recap

Despite the continued lack of clarity regarding the current state of tariffs and a whole bunch of other macro warning signals, markets closed higher yesterday. Small caps led the way as the Russell 2000 gained 1.11%. Both the Dow and the S&P 500 rose just under 0.80%, and the Nasdaq Composite closed 0.64% higher. Sectors were up across the board, with leadership coming from Real Estate (2.21%), followed by Utilities (1.80%) and Consumer Staples (1.71%). The remaining sectors saw results ranging from 1.22% (Health Care) to 0.29% (Consumer Discretionary).

The advance/decline line for holdings of the SPDR S&P 500 ETF Trust (SPY) was a healthy 433/70 and while the top 10 contributors to return included 2 Mag 7 names Apple (AAPL), Alphabet (GOOG, GOOGL) we saw a good mix of consumer and healthcare companies, including Eli Lilly (LLY), AbbVie (ABBV), Walmart (WMT), and Costco Wholesale (COST). The balance of Mag 7 names detracted from SPY performance along with names like JP Morgan JPM), UnitedHealth Group (UNH), Booking Holdings (BKNG), and Southwest Airlines (LUV).

While Goldman Sachs (GS) is calling for gold to hit $3,700/oz by the end of 2025, we saw gold trade off from Friday’s all-time high to $3,207.50 by yesterday’s market close. Also easing was the Cboe Market Volatility Index (VIX), which fell almost 18% to 30.89. A reminder that VIX at a 30 handle is preferable to seeing it in the 40s, but a truly normalized expectation of volatility would see this indicator in the mid-teens.

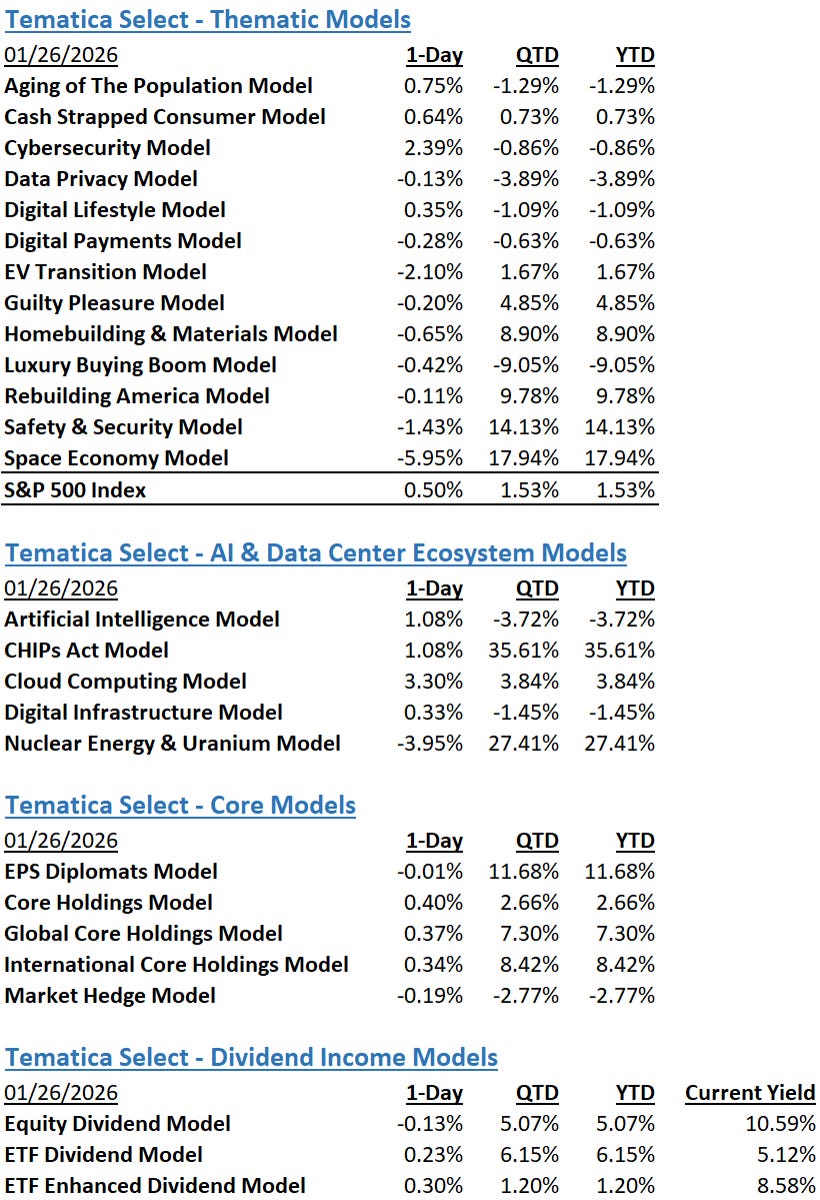

The Tematica Select Model Suite had an overall positive day with leadership coming from EPS Diplomats, Cash Strapped Consumer, and Safety & Security. Lagging strategies included Space Economy, Luxury Buying Boom, and EV Transition. Market Hedge gave back some YTD gains but overall, this strategy continues to outperform the S&P 500 considerably, by more than 24% as of yesterday’s close.

China’s Evolving Trade Playbook, Trump’s Chip Move, and Investor Gloom

Futures point to a positive start when US equity markets open later this morning, but we will have several developments between now and the opening bell that could alter that expectation. On the economic front, coming off disappointing quarterly results from LVMH Moet Hennessy Louis Vuitton SA (LVMUY), investors may revisit expectations for tomorrow’s March Retail Sales report. That update should provide more insight into where consumers are spending and help frame March quarter expectations for the likes of Amazon (AMZN), Starbucks (SBUX), Walmart (WMT), and others. Also bringing more insight into the vector and velocity of the economy and consumers, we have quarterly results this morning from Albertsons (ACI), Bank of America (BAC), and Citigroup (C), followed by United Airlines (UAL) and JB Hunt (JBHT) this afternoon.

As folks digest those comments and revised outlooks, they will continue to update their thinking for the latest trade developments. For example, over the weekend, China altered the trade playbook from one focused on tariffs by halting rare earth exports. Earlier today, China directed its airlines to suspend deliveries of Boeing (BA) jets as well as directed its airlines to stop buying aircraft components from US suppliers.

Lest you think that means the emphasis is off tariffs, President Trump’s administration pressed forward with plans to impose tariffs on semiconductor and pharmaceutical imports by initiating trade probes led by the Commerce Department. The filings set to be published on Wednesday set a 21-day deadline from that date for the submission of public comment on the issue and indicate the administration intends to pursue the levies under authority granted by Section 232 of the Trade Expansion Act of 1962. Such section 232 probes need to be completed within 270 days after being announced. The Trump administration has started similar initiatives on copper and lumber imports and over the weekend, Trump said he would be announcing a tariff rate on imported semiconductors over the next week.

In response to that chip uncertainty, South Korea increased its aid package for the semiconductor industry to 33 trillion won (~ $23.25 billion), up from the 26 trillion won package introduced last year. We’ll also be very interested in comments about current and future capital spending plans when Taiwan Semiconductor (TSM) reports its quarterly results on Thursday. With an eye toward our various models (see more below), we’ll also be digging into its end market mix for the quarter as well as its expectations for the current one.

If you’re thinking all of this paints an uncertain if not gloomy picture, the findings from Bank of America’s April 2025 fund manager survey should not surprise you. Fund managers are extremely gloomy, with 82% of respondents to BofA’s monthly survey expecting the global economy to weaken and 42% saying a recession is likely. Those findings and others in the report support BofA’s call that the stock market’s April lows will hold in the near term and that “big upside needs big tariff easing, big Fed rate cuts, and/or economic data resilience.”

We agree with those three potential catalysts to drive the market higher. However, our view that business and tariff uncertainty as well as slowing consumer spending and China’s evolving playbook, will lead companies to issue below consensus expectations for the current quarter and potentially 2H 2025 remains unchanged.

More By This Author:

A Reprieve, Of Sorts

Trump: How You Like Me Know?

Tariff Clarity? Earnings Pre- Announcements?

Comments

Log in or sign up to join the conversation.