Image Source: Pexels

Market Wrap/Today’s Outlook

So, who knew postponing Tariff-ageddon would lead to one of the best one day rallies in US market history? A relief to be sure but Nasdaq Composite up 12.16%, S&P 500 adding 9.52%, Russell 2000 jumping 8.85%, and the Dow closing 7.87%? To be clear, yesterday was not in anyone’s cards. Still, sectors were up across the board, led by Technology (13.43%) and Consumer Discretionary (10.89%) which were buoyed by their Mag 7 constituents contributing to 43% and 48% of sector results, respectively. Remaining sectors posted gains ranging from 3.88% (Consumer Staples) to 8.88% (Industrials).

The Cboe Market Volatility index (VIX) fell 36% which is another relief but yesterday’s close still sees the VIX at a 33 handle, just over double its long-term average. As far as volatility is concerned, a 90-day reprieve is just that, a reprieve.

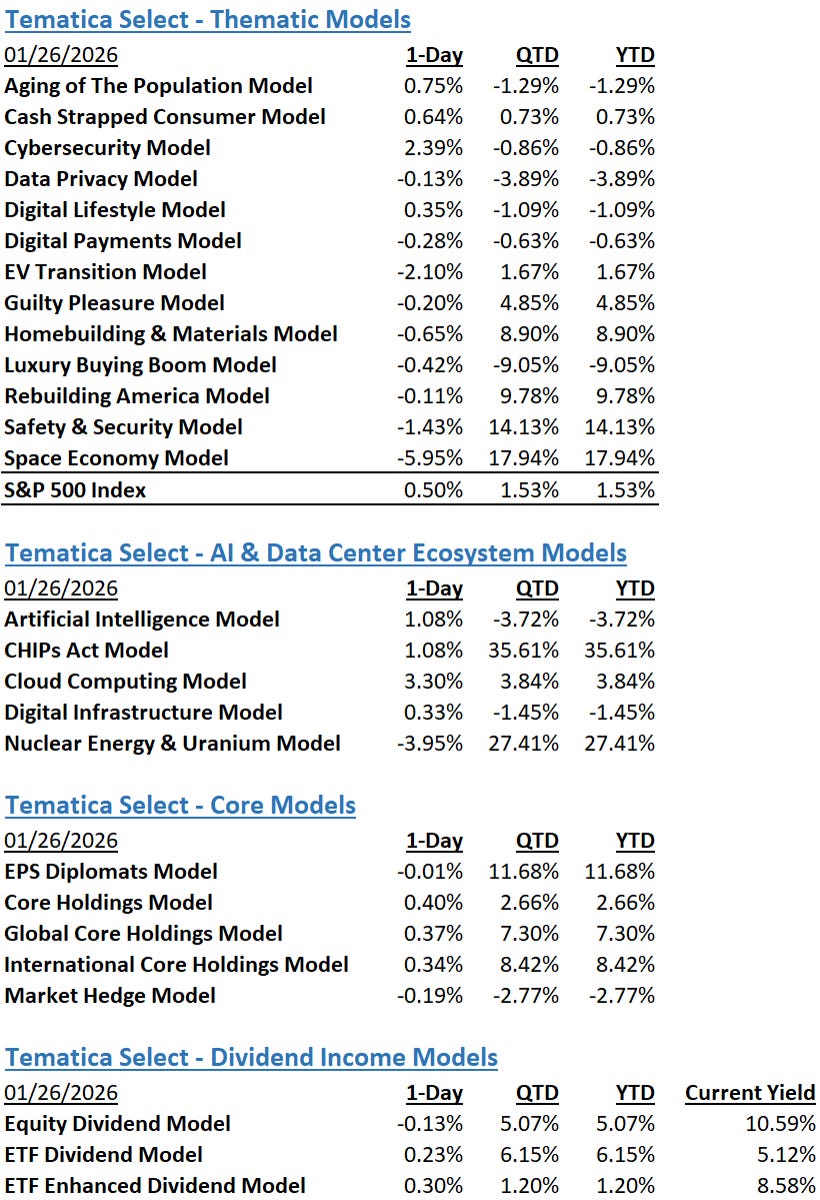

Needless to say, the Tematica Select Model Suite had a stellar day. We saw Market Hedge give back about a third of it’s YTD returns which leaves that strategy “only” 22% above the S&P 500. Similarly, double digit single day returns for roughly half of our targeted exposure strategies were great to see but didn’t erase the YTD underperformance we’ve seen so far in 2025. Some final caveats about sounding the “all-clear” come from Goldman Sachs (GS), who rescinded their 65% chance of a recession in 2025 call but only took it back to their previous 45% chance, and JP Morgan (JPM) who maintains their 60% chance of a US recession, which also includes provisions for Trump easing pressure on China.

So far this morning, futures have resumed their trend of downward pressure. It seems like some of yesterday’s price action may be attributed to short covering and ultimately any fundamental rationale for the recent meltdown has only shifted further out but not really changed. This morning we’ll see the latest updates on CPI where the top line figure is expected to have moderated slightly, to 2.6%. Given the current tariff environment, this update is good to know but we doubt anyone will be finding it particularly useful as a forecasting tool. Initial and continuing claims will also be updated, with continuing claim expected to have dropped slightly and initial claims adding about 6,000 to sit at 225,000 for the observation week ending April 5.

While the pause button has been mashed, markets are still working out the potential effect of 125% tariffs on China which have not been included in the pause, not to mention the 10% blanket tariff applied to everyone else. Did we mention that Canada tariffs were also not impacted by yesterday’s about face? We expect that calculus to continue to play out in today’s trading. Don’t forget, as smart as all these analysts and their models are, the hard truth is that nobody has a crystal ball and all they can do is crunch what data they have when they get it. In this environment, that can lead to some, uh, interesting times.

More By This Author:

Trump: How You Like Me Know?Tariff Clarity? Earnings Pre- Announcements?

Trump Auto Tariffs, Fed Speakers, CoreWeave’s IPO

Comments

Log in or sign up to join the conversation.