During extended upward-trending markets that reward risk-takers and punish caution, everyone is a “bull market genius.” That dynamic flips investor psychology and, over time, creates a false sense of control. As the market continues to climb, risk appears to vanish, and investors believe that nothing can go wrong, leading them to take on increasing levels of risk and leverage. After all, why wouldn’t you if there is “no risk” in investing?

“Over the past 15 years, the markets were repeatedly bailed out of more serious corrections by either fiscal or monetary policy. That neutral stimulus (the interventions) was repeatedly paired with a reward-stimulus of markets going higher. As such, investors were “conditioned” to expect rescue whenever issues arise, to buy stocks on every decline, and to believe that this cycle will indefinitely continue. This was the point we made recently regarding “moral hazard.”

“The Federal Reserve’s well-intentioned interventions have created one of modern finance’s most powerful behavioral distortions: the conviction that there is always a safety net. After the Global Financial Crisis, zero interest rates and repeated rounds of quantitative easing conditioned investors to expect that policy support would always return during volatility. Over time, that conditioning hardened into a reflex: buy every dip, because the Fed will not allow markets to fail. What exactly is the definition of ‘moral hazard?’

Noun – ECONOMICS: The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

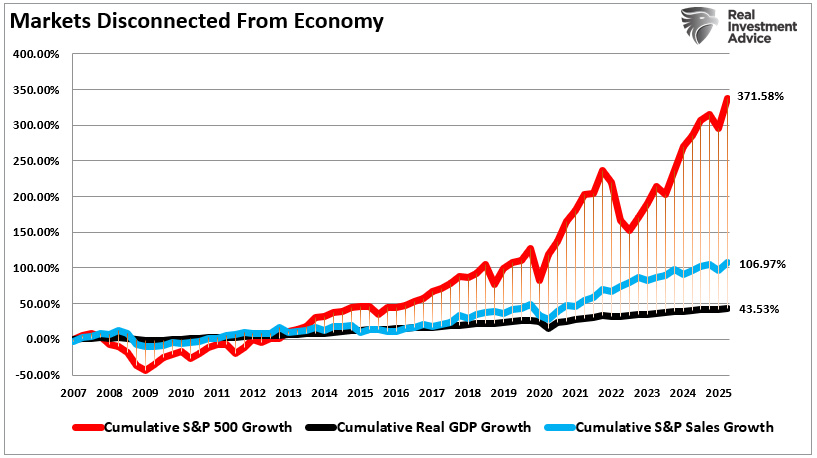

In other words, just as Pavlov’s dogs would start salivating at the “ringing of the bell,” investors are “chasing speculative assets” simply on the assumption that the “food” will arrive. But, as noted, while the Federal Reserve has trained investors to “buy the dip” over the last 15 years, the market has detached from underlying fundamentals,

What starts as smart investing mutates into speculation.

I recently read two excellent articles (here and here) discussing investor behavior during prolonged bull markets. We will dig into the lessons from those articles and how to navigate the market in the future.

The Bull Market Genius and the Problem of Forgetting

Long bull markets build confidence. But not the healthy kind. They create the type that whispers in your ear, “You’re brilliant.” The phenomenon has a name: bull market genius.

Bull market genius is not just overconfidence. It’s a specific brand of self-deception that comes from mistaking a rising tide for your own intelligence. You buy a tech stock. It doubles. You feel smart. You buy five more. They triple. Now you’re a genius, and you start adding leverage to increase returns further. Why wouldn’t you? The market isn’t just working; it’s validating your skill.

However, that is when danger sets in.

As Ben Carlson noted in his article, Benjamin Graham, one of the greatest investors in history, fell victim to this very cycle during the late 1920s. He turned $400,000 into $2.5 million using leverage and aggressive positioning. His success convinced him he had mastered the game. He fantasized about yachts and real estate. Then came 1929. The market collapsed, and his fortune dropped to $375,000, an 85 % decline.

Graham later admitted he ignored risk because the gains felt like proof of his brilliance. That’s bull market genius. It distorts your judgment. It tells you you’re right even when your bets are reckless.

Today’s investors face a similar risk. After more than a decade of upward markets, turbocharged by central banks, low interest rates, and easy credit, many have never seen a sustained downturn. Stocks resemble savings accounts, volatility appears as opportunity, and risk appears as a relic.

In William Bernstein’s article, he discussed what Peter Bernstein (no relation) called the “empty memory bank” problem. Investors who haven’t lived through a real bear market underestimate what losses feel like. They read about crashes, look at them on a chart, but have never experienced the psychological and financial destruction that occurs during one. That absence of pain creates the illusion of safety, which feeds the bull market genius mindset.

This is why you need to be careful about whom you take advice from. Many financial commentators and advisors have never experienced a genuine bear market. That lack of bear market experience leads to much of the “buy and hold” thesis of just “riding out bear market declines.”

Let me warn you, as someone who has lived through and traded through both the Dot-com and Financial Crisis, when the next bear market drawdown arrives, the illusion of safety will be shattered.

What to Focus on When the Cycle Turns

When euphoria dominates, attention shifts from fundamentals to fantasies. At that point, you must focus on risk, not return, which is hard to do when gains keep coming. However, it is a critical step in surviving the long game.

While valuations may not seem to matter in the short run, they do matter in the long run. As discussed in “Valuations Don’t Matter Until They Do,”

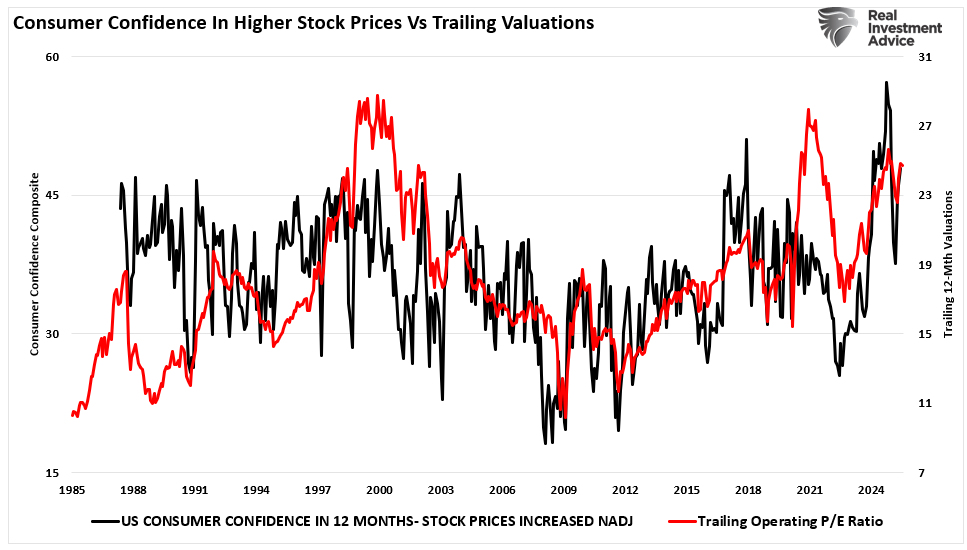

“Market valuation measures are just that—a measure of current valuation. Moreover, market valuations are a much better measure of “investor psychology” and a manifestation of the “greater fool theory.” This is why a high correlation exists between one-year trailing valuations and consumer confidence in higher stock prices.”

What market valuations express should be obvious. If you “overpay” for something today, the future net return will be lower than if you had paid a discount for it. You are not buying companies, but streams of cash flow. This is why the math of valuations is so easy to understand. Markets do not reward optimism indefinitely.

Such is why risk management isn’t an option. As we discussed in “Portfolio Risk Management,“

“Most investors focus on being right by obsessing over stock picks, timing, and macro predictions. However, here is the hard truth you must learn: Accuracy is overrated. Survival is underrated.

Your real edge comes from limiting damage when you’re wrong and maximizing gains when you’re right, which is the very foundation of any risk plan. You will lose. You must build your system around that fact, which encompasses three crucial facets:

- Position sizing,

- Stop-loss rules, and

- A strict discipline that is easily repeatable.

“Ultimately, that blueprint will be what separates long-term success from failure. Risk management isn’t about avoiding loss. It’s about ensuring the losses you take don’t destroy you.“

Risk management is not optional.

The only way to prepare for pain is to internalize it before it arrives. If you wait until your account is down 30%, it’s too late. Your emotions will take over, your discipline will crumble, and your memory will fail you. That’s when bull market genius turns to panic.

The next leg of the cycle may not resemble the last, as markets rarely repeat themselves exactly. However, investor behavior always repeats: overconfidence, crowding, and denial have appeared in every bull run, but always end in panic, despair, and massive capital destruction.

You can sidestep those traps with a few straightforward rules.

- Rebalance regularly: When one part of your portfolio outgrows the rest, trim it back to a more balanced allocation. That’s not market timing. That’s discipline.

- Use stress tests: Simulate a 40 % drop. If that makes you nervous, adjust now.

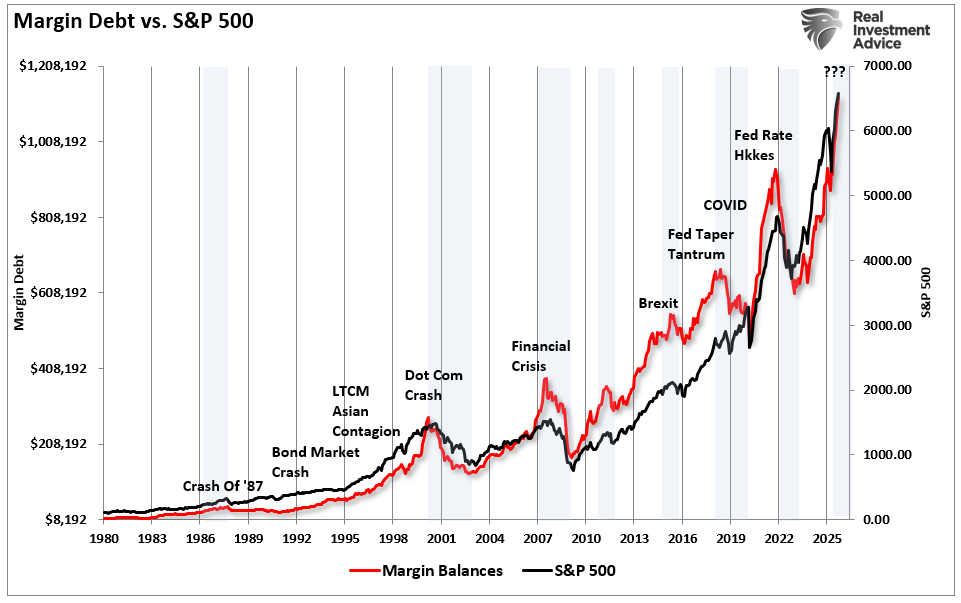

- Keep leverage low: Margin works until it doesn’t. And when it fails, it fails fast.

- Keep 5 % to 10 % in cash or equivalents. That buffer gives you choices when prices drop.

- Favor fundamentals over hype: Valuation, profitability, free cash flow. The basics matter when the music stops.

- Write down your plan: When things get crazy, read it. It will remind you who you were before greed kicked in.

- Study past bear markets: Don’t read headlines, but talk to people who have lived through them. Their experience is more valuable than anything else.

You don’t need to time the top, but you do need to survive the cycle. That starts with protecting the downside.

Discipline looks foolish during a mania, but it will save you during the eventual decline. Your goal isn’t to look smart today, it’s to be standing tomorrow.

If you feel like a bull market genius right now, be careful, as that might be the market fooling you.

The most brilliant move is often the boring one, as bull market geniuses always get crushed when reality returns.

More By This Author:

SpaceX: A Financial And Strategic Windfall For GoogleThe “Double Bubble”

Does AI Capex Spending Lead To Positive Outcomes?

Comments

Log in or sign up to join the conversation.