Classical conditioning teaches us a valuable lesson regarding the current investor dilemma. Pavlov’s research discovered a basic psychological rule: when a neutral stimulus is repeatedly paired with a reward‑stimulus, eventually it will trigger the same response even when the reward is absent. The famed experiment by Ivan Pavlov illustrated that dogs would salivate at the sound of a bell after the bell was repeatedly paired with food. The pattern is simple: bell becomes signal, trigger leads to reflex, behavior becomes automatic.

The concept translates directly into the investor dilemma in financial markets. As Steve Sosnick of Interactive Brokers recently noted:

“The other morning, someone asked me why we were trading higher. I made the flippant comment, “they rang the opening bell, that’s why.” Taking that a step further, on a morning when stocks are higher on a rally that began modestly in the pre-market but accelerated rapidly after the regular session opened, it is reasonable to wonder whether there is indeed a Pavlovian quality to the current market environment.”

That really should be unsurprising. Over the past 15 years, the markets were repeatedly bailed out of more serious corrections by either fiscal or monetary policy. That neutral stimulus (the interventions) was repeatedly paired with a reward-stimulus of markets going higher. As such, investors were “conditioned” to expect rescue whenever issues arise, to buy stocks on every decline, and to believe that this cycle will indefinitely continue. Such was the point we made recently with respect to “moral hazard.”

“The Federal Reserve’s well-intentioned interventions have created one of modern finance’s most powerful behavioral distortions: the conviction that there is always a safety net. After the Global Financial Crisis, zero interest rates and repeated rounds of quantitative easing conditioned investors to expect that policy support would always return during volatility. Over time, that conditioning hardened into a reflex: buy every dip, because the Fed will not allow markets to fail. What exactly is the definition of ‘moral hazard?’

Noun – ECONOMICS: The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.

However, the Pavolovian experiment is complete, as investors are chasing asset prices in the companies with the worst fundamentals, assuming that the Federal Reserve will “insure” them against losses.

In other words, just as Pavlov’s dogs would start salivating at the “ringing of the bell,” investors are “chasing speculative assets” simply on the assumption that the “food” will arrive. But, as noted, while the Federal Reserve has trained investors to “buy the dip” over the last 15 years, that market has detached from underlying liquidity. In other words, since 2022, investors have been chasing stocks higher and drifting from one “Fed statement” to the next, looking for clues as to when monetary accommodation will return.

The investor dilemma is that while “buying the dip” has been an effective strategy over the last decade, the current backdrop has changed. The many variables that allowed “reflexive behavior” to work, such as ultra‑low yields, endless liquidity, and expanding central‑bank balance sheets, are fading or gone. The Federal Reserve has previously stated that a “return to zero yields” will not be in its “playbook” in the future. Therefore, current investor behavior is a function of experience, not the changing present.

But that is also why “Animal Spirits” are such a powerful force, and a danger.

The Problem With Animal Spirits

The term Animal Spirits” comes from the Latin term “spiritus animals,” meaning “the breath that awakens the human mind.”

The term can be traced back to 300 BC in human anatomy and physiology. It refers to the fluid, or spirit, responsible for sensory activities and nerves in the brain. Besides the technical meaning in medicine, animal spirits is also part of literary culture. In that form, they referred to states of physical courage, delight, and exuberance.

Its modern usage came about in John Maynard Keynes’ 1936 publication, “The General Theory of Employment, Interest, and Money.” He used the term to describe the human emotions driving consumer confidence. Ultimately, the financial markets adopted the “animal spirits” to describe the psychological factors that drive investors to take action. This is why human psychology is essential in understanding the close linkage to short-term valuation measures.

The 2008 financial crisis revived interest in the role that “animal spirits” could play in the economy and financial markets. The Federal Reserve, under the direction of Ben Bernanke, believed it necessary to inject liquidity into the financial system to lift asset prices to “support” consumer confidence. The result would be a self-sustaining environment of economic growth. In 2010, Bernanke made his famous statement as the economy was on the brink of slipping back into a recession. The Fed’s goal was simple: ignite investors’ “animal spirits.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

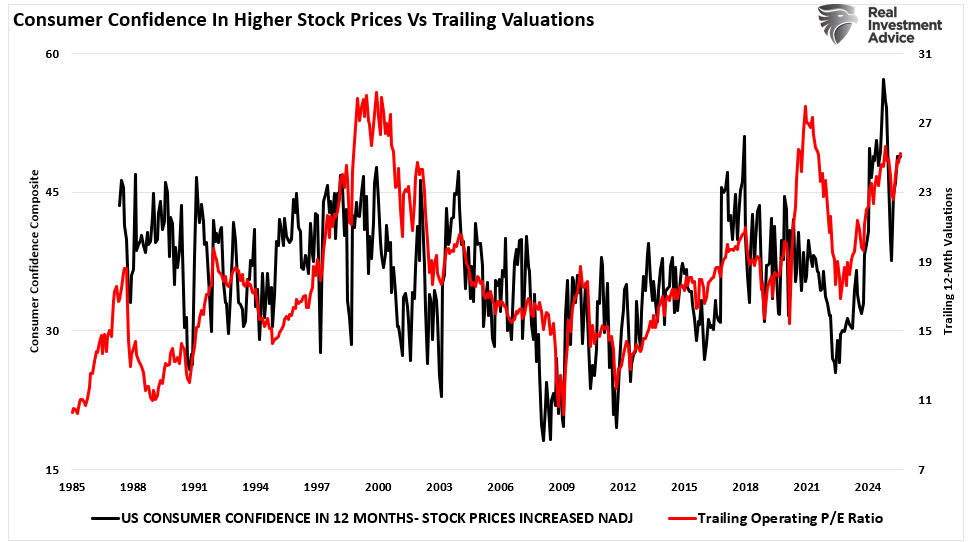

“Bernanke & Co.” successfully fostered a massive lift in equity prices, boosting consumers’ confidence. (The chart below shows the composite index of the University of Michigan and Conference Board surveys. Shaded areas are when the index is above 100.) However, since 2022, the markets have become detached from underlying economic activity as the massive stimulus and interventions continue flowing out of the economic system.

The investor dilemma is that instead of flowing through the system, liquidity remained bottled up within institutions and the ultra-wealthy, who had “investible wealth.” However, the bottom 90% of Americans live paycheck to paycheck. The chart below shows the failure of the flush of liquidity to translate into economic growth. While the stock market returned over 371% since the 2007 peak, that increase in asset prices was more than 8.5x the growth in real GDP and roughly 3.5x the growth in corporate revenue. (I have used SALES growth, which is not as subject to accounting manipulation.)

Understanding that asset prices should reflect economic growth, which creates revenue growth, the deviation is a risk worth addressing. What matters today is the investor dilemma facing the markets. The assumption is that the mechanism remains the same, and outcomes will be the same. However, there is no guarantee of that. There is no guarantee that the Federal Reserve will revert to massive monetary expansions during the next crisis. There is also no guarantee that the markets will respond the same. While investors believe stimulus will drive growth, and that markets will follow, the transmission mechanism may not work as efficiently next time. After the 2008 crisis, the Fed pushed liquidity into the system. But much of that liquidity stayed within banks and the wealthy, failing to transmit broadly into wages, profits, and real growth. The investor dilemma arises when you ignore this breakdown.

Currently, investors are taking on increasing levels of risk based on the assumption that the “bell” will ring again. But what if it doesn’t?

Why the Investor Dilemma Matters Now

The current market environment magnifies the investor dilemma for three reasons:

- Valuations are elevated.

- Stimulus is less potent.

- Economic momentum has slowed, and global risk is rising.

Yet, retail investors are chasing dip‑buying, as the “Fear of Missing Out” dominates flows, with many assuming another surge in asset prices is just around the corner. Maybe that is the case. However, if you examine the breadth of the market, you’ll see cracks. Large‑cap indices may hover near highs while small and mid‑cap stocks lag significantly. More notably, the divergence between the market-cap weighted and equal-weighted S&P 500 (RSP) suggests breadth remains weak, lulling investors into a false sense of safety

Additionally, commodities, one of the core barometers of economic health, are signaling caution. When oil breaks trend, manufacturing suffers, and inflation declines. That is not a signal of economic prosperity to support elevated earnings expectations.

The investor dilemma of FOMO blinds you to these signals because you are focused on chasing asset prices rather than the risk that action exposes you to. For example, you drive faster than the speed limit because everyone else is too. However, the faster you drive, the risk of getting a speeding ticket (or worse) increases.

With liquidity thinning and policy tools constrained, the risk to investors is increasing. It is unlikely that central banks will flood the market like they did after 2008 or during the pandemic, without a coincident crisis. However, investors act as though the rescue is automatic, increasing risk without respect for inputs and outputs. When the stimulus fails to deliver, you face asymmetric outcomes. That is the practical consequence of the investor dilemma. You are trained, but the training does not match the terrain.

You risk a misstep if you ignore valuation, breadth, and monetary multipliers. At some point, the “buy the dip” mentality will fail, as the “dip” becomes the start of a more significant downtrend. The investor dilemma convinces you that the past will repeat itself. The reality is: conditions change.

Navigating the Investor Dilemma in Your Portfolio

You must shift your mindset from reflex to discipline to manage the investor dilemma.

- Ask yourselves when a dip appears: is this an opportunity or a trap? Don’t simply buy because you “feel” like you should. Question the fundamental backdrop, valuations, and whether economic underpinnings exist. That simple query breaks the investor dilemma loop.

- You must build a plan, not react impulsively. Set allocation thresholds, define stop‑loss levels, and review exposures. If you assume every dip is a buy, you fall into the investor dilemma trap of over‑risking. Diversify not just across assets but across regimes, consider strategies that protect capital if the assumption of constant rescue fails.

- Focus on fundamentals. While it seems to be an “outdated concept” in the current environment, ignoring earnings, leverage, breadth, and growth has led to horrible outcomes. Evaluate whether companies deliver real growth, whether valuations reflect risk, and whether global signals support expansion. If fundamentals are lacking, you’d be better off managing risk.

- Accept unpredictability. The investor dilemma thrives on certainty, but markets often surprise complacency. The current regime will flip for whatever reason, and the ability to accept unpredictability reduces risk exposure over time.

Many things can and will eventually go wrong. Eventually, “buying the dip” won’t lead to a positive outcome. Unfortunately, investors are now trained to believe that such will not happen. However, that is the investor dilemma; it is the one risk you must navigate. Recognizing the conditioning, shifting your posture, building protection, and acting deliberately will keep you alive when “buying the dip” eventually goes wrong.

More By This Author:

Hindenburg Strikes: Omen Or False Alarm?Fed QT Ends. What Does That Mean For Markets?

Gold Myths Luring Investors Into Risk

Comments

Log in or sign up to join the conversation.