The financial services sector has an abundance of blue chip companies. With management teams in the space intrinsically good in financial management, it comes as no surprise that companies in the sector feature strong track records of shareholder value creation. In fact, out of the roughly 350 blue chip companies we have compiled, which feature at least 10 successive years of dividend hikes, 91 operate in the financial services sector.

Boasting 18 years of consecutive dividend increases, Ameriprise Financial is one of those companies. Supported by a long-lasting track record of annual dividend increases going back at least a decade, we believe that companies like Ameriprise Financial have proven their capability to deliver steady growth and raise their dividend, even in a recession.

Accordingly, we feel that blue chip stocks that satisfy the 10-year payout growth streak criterion are among the safest dividend stocks that investors can buy.

The fifth installment of the 2022 Blue Chip Stocks In Focus series will analyze Ameriprise Financial, Inc. (AMP).

Business Overview

With a 128-year history of providing solutions to assist clients in achieving their financial goals, Ameriprise Financial has grown to become one of the leading companies in the wealth & asset management industries.

The company’s wealth management division offers a differentiated advice value proposition. With a network of over 10,000 financial advisors, Ameriprise strives to establish long-term personal relationships with its clients and provide them with customized solutions, including banking, brokerage, and insurance services.

The company’s asset management division, promoted through the Columbia Threadneedle Investments brand, offers a wide range of investment advice and products to high-net-worth individuals and institutional investors. As of its latest filings, Ameriprise Financial had $1.3 trillion in assets under management.

Wealth and asset management firms are highly susceptible to the underlying state of the capital markets. During optimistic market environments (e.g., the more than decade-long bull run that followed the 2007-2008 Financial Crisis), companies in the space draw increasing inflows from investors. During uncertain periods in the capital markets, however, exactly the contrary happens, impairing the companies’ performance.

While asset management firms recorded significant outflows during the first half of 2022 due to the ongoing market turmoil, Ameriprise’s performance remained robust, at least as far as its Q1 results go. For the quarter, revenues rose 9.3% to $3.66 billion, while adjusted earnings-per-share came in at $5.98, compared favorably to the prior year’s result of $5.43. The improved performance was powered by loftier total assets under management, which rose 17% to $1.3 trillion.

Source: Investor Presentation

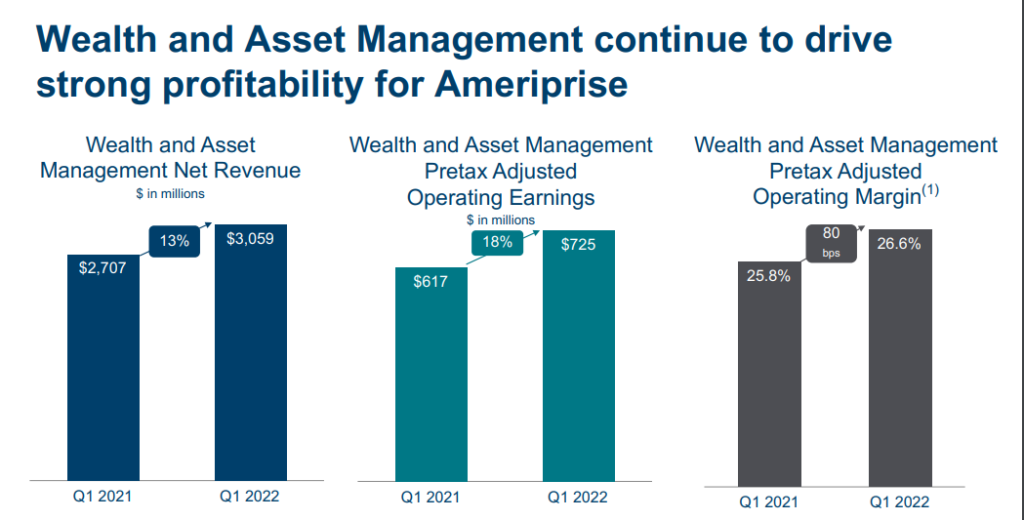

Specifically, client assets for Advice & Wealth Management expanded 8% to $823 billion. The segment’s net revenues increased by 9% as a result. Adjusted operating earnings for the asset management segment by 13%, as segment as operating margins expanded by 80 basis points.

The asset management segment also performed well, with total assets under management growing 24% to $699. Long-term investment performance also remained vigorous, as more than 80% of funds were above the median on an asset-weighted basis over 3, 5, and 10-year time periods across equity, fixed income, and asset allocation strategies.

Backed by the strength of its Q1 earnings, we now expect that the company will earn $25.41 for the full year.

Growth Prospects

During the past decade, Ameriprise Financial compounded its earnings-per-share at a rate of about 19.3% per annum. Growth accelerated in the most recent years on the back of elevated asset prices, as this figure stands at 21% over a five-year basis.

As we advance, we are estimating a more prudent 8% earnings-per-share growth from the company. While this implies a heavy deceleration from its past growth levels, it’s better to be rather conservative in the face of the current market environment. We expect earnings growth to be powered largely by increasing revenues and share buybacks. We also expect the company’s asset management segment to remain rather resilient, as proven by the 24% increase in AUM and the 25% increase in earnings despite Ameriprise recording $0.7 billion in outflows during the quarter.

Source: Investor Presentation

We are also forecasting dividend growth to keep approximately the same pace as earnings growth since the company is likely to persist in favoring share repurchases given the stock’s consistently low valuation multiples. For context, the company’s 18-year dividend growth streak has retained a rather rapid pace. Specifically, dividends have grown at a 10-year CAGR of 18.1%.

Competitive Advantages & Recession Performance

Ameriprise has developed a strong brand, which makes for a rather significant competitive advantage in what is a very competitive industry. While the company’s performance has remained concrete despite the ongoing restlessness in capital markets, Ameriprise is not immune to a recession.

Specifically, investors should respond to any uncertainty associated with evolving recession fears, rising inflation, interest rate hikes, and geopolitical pressures, which could reduce the company’s assets under management. A number of other macroeconomic factors could also affect the company’s financials. For example, the recent considerable dollar appreciation against major currencies is likely to have a negative impact on the value of the company’s AUM in the coming quarters.

The Great Financial Crisis makes for a great example of how declining asset prices can affect Ameriprise’s earnings. Still, the company’s results rebounded rather quickly.

You can see a rundown of Ameriprise Financial’s earnings-per-share from 2007 to 2011 below:

- 2007 earnings-per-share of $3.45

- 2008 earnings-per-share of -$0.16

- 2009 earnings-per-share of $2.98

- 2010 earnings-per-share of $3.94

- 2011 earnings-per-share of $4.87

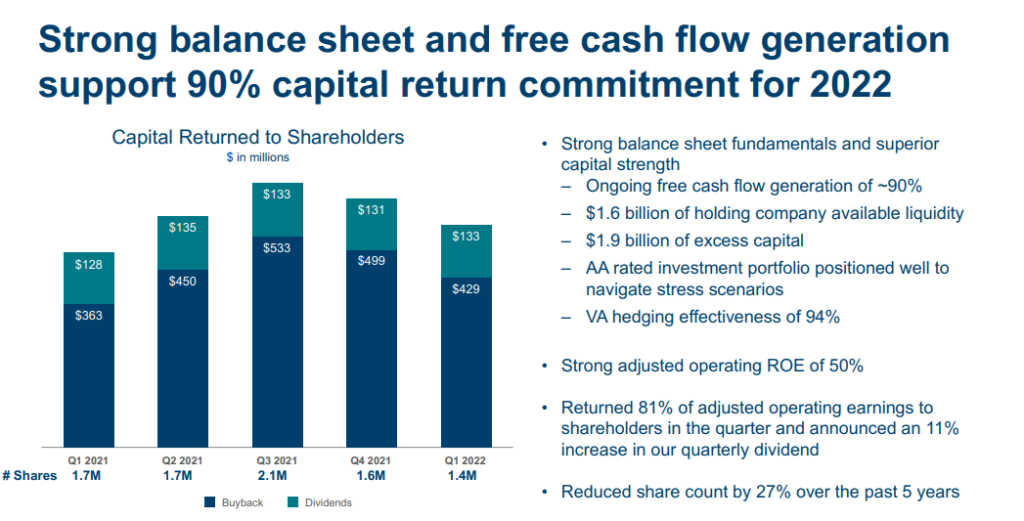

It’s also worth noting that while most companies in the industry carry heavy amounts of debt on their balance sheet, Ameprise actually holds a net cash position of $4.52 billion. It should allow the company to continue returning capital to shareholders at a very aggressive pace.

Source: Investor Presentation

Overall, we believe that the company’s dividend is very safe. The payout ratio stands at a comfortable 20% based on our EPS estimate for the year, and it has never crossed the 33% threshold over the past decade.

Further, should the company experience financial pressures, it’s more than likely to slow down or pause its aggressive buybacks before touching the dividend. For context, the company has repurchased and retired 57.5% of its common stock since 2010.

Valuation & Expected Returns

Ameriprise shares have traded at an average P/E ratio in the low teens over the past decade. Based on our present EPS estimate, shares are trading at a (forward) P/E of 9.6. We have set our fair medium-term P/E ratio at 11.5, reflecting the stock’s historical average.

Source: Author

If Ameriprise’s price-to-earnings multiple expands from 9.6 to 11.5, future returns would be boosted by 3.6% per year through 2027. Along with our expected EPS & DPS growth of 8% and the current dividend yield of 2.0%, estimated annualized total returns over the next five years come out at 13.5%.

Consequently, while investors should be wary of the company’s performance during a recession, we rate Ameriprise Financial stock as a buy.

Final Thoughts

Ameriprise Financial is a high-quality company with a strong brand value in the industry. The company is susceptible to the underlying circumstances of the capital markets, which could harm its results during a potential recession. Still, the qualities of Ameriprise’s balance sheet and management are likely to lead to a quick rebound in results, as demonstrated during the 2007-2011 stretch.

The company’s 18-year dividend growth track record is a testament to its resilience and overall qualities as well. Overall, for the reasons mentioned, we believe that dividends should remain well-covered even during a potential market downturn. Hence, Ameriprise makes for an attractive blue chip stock to buy, especially at its current valuation multiple.

More By This Author:

Warren Buffett Stocks: Occidental Petroleum

Blue Chip Stocks In Focus: Lowe’s Companies Inc.

Warren Buffett Stocks: Verizon Communications

Comments

Log in or sign up to join the conversation.