In August 2025, Beyond Meat (BYND), a plant-based meat producer, took to social media to call reports of its bankruptcy “unequivocally false“. Despite the assurances, the company was floundering, and bankruptcy was a possibility. The company has significant liabilities and has lost money every year since its IPO. Adding to their woes, sales peaked in 2021 and have steadily declined since. Can Beyond Meat avoid bankruptcy while losing money and watching sales decline?

To help address its issues, on October 15th, the company completed an agreement that allowed its creditors to swap their debt for a combination of new debt and equity. The deal was dilutive to shareholders and drastically reduced Beyond Meat’s valuation. Beyond Meat shares reacted poorly over the next two days, falling by over 30% to nearly $0.50. Bear in mind, this was a $200+ stock in early 2021. Despite the bleak outlook, a meme trader named Demitri Semenikhin started promoting Beyond Meat shares on social media. Days later, the Roundhill Meme Stock ETF added Beyond Meat shares to its portfolio. Since Demitri pumped the company, its stock rose from $0.52 to over $7.00.

Beyond Meat is yet another example of the extreme speculation in the market. The company, despite recent efforts, will likely go bankrupt. While the debt swap may buy time, their weakening sales and heavy debt load, when combined with expected negative cash flows, are not a recipe for survival. Maybe shares are correctly rallying because management can turn the company around. Or, more likely, meme traders will make outstanding short-term profits as they sucker speculative investors into Beyond Meat to buy their shares at a higher price and leave these investors holding the bag.

(Click on image to enlarge)

What To Watch Today

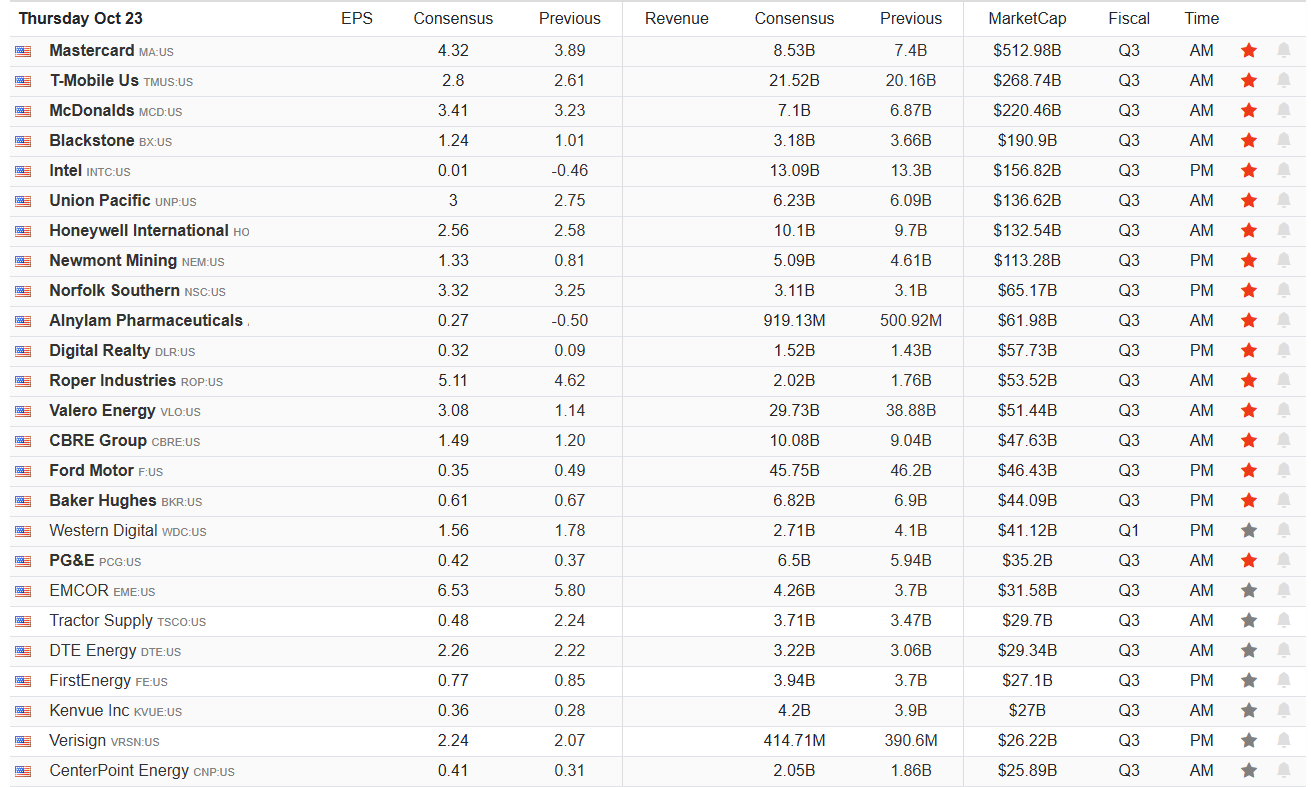

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

Yesterday, we discussed the ongoing speculation in the market, which has led to a rather extreme deviation from the 40-week moving average. Over the last couple of days, we have finally seen the expected reversal in the momentum and more speculative trade bets as we head into the end of the month.

(Click on image to enlarge)

This rotation is not surprising over the last few days, as October marks the fiscal year-end for about 24% of all mutual funds. As such, they need to rebalance exposures, capture gains, and sell tax losses for the year, which tends to add some pressure to markets near the end of the month.

Technically, the market is struggling with the bottom of the rising trend line following the “Liberation Day” sell-off. The good news is that the market did reclaim the 20-DMA and is closing in on triggering a momentum “buy signal.” This aligns with the idea that after a brief “spat” in the market, the seasonal backdrop we discussed in last weekend’s #BullBearReport will kick in. As we discussed, earnings, corporate buybacks, and very bullish investor sentiment and positioning will remain supportive through year-end.

(Click on image to enlarge)

The bad news is that the market failed at the bottom of the rising bullish trend channel from the “Liberation Day” lows. This makes the 20-DMA an important short-term support with the 50-DMA just below it. For now, however, the bullish trend remains, and “buy the dip” continues to work for now.

As we concluded in that post:

“While the broader seasonal trend starts soon, there is a risk to the bullish backdrop. As we have already seen, October is known for its volatility pickup, and this past week has undoubtedly served as a reminder. However, any weakness during this stretch often provides entry points, not reasons to exit. Markets that consolidate or pull back in October usually rebound in November. On the other hand, December is often weak during the first couple of weeks of the month as professional fund managers distribute their annual capital gains, dividends, and interest. That distribution period tends to provide a short-term pullback that investors can buy into before the year-end rally. Lastly, additional monetary accommodation could support the rally with the Federal Reserve signaling further rate cuts and an end to Quantitative Tightening (QT).

Does this mean there is “zero risk” that something could go wrong, leading to a bigger correction? No. There is always a risk that some unexpected, exogenous event could disrupt markets. However, investors who try to wait for ideal entry points risk missing the rally. While upside may be slower and more rotational than earlier in the year, the path of least resistance remains higher as we move toward year-end. The seasonal setup, earnings, and buybacks support the case for a stock market rally into the final quarter.”

Trade accordingly.

Banks May Get A Break

The banking sector’s lobbyists have been working full-time to reduce Biden-era banking capital proposals. Two years ago, the banks feared the Fed would impose large capital requirement hikes. Such would reduce their ability to lend and buy securities, but it would also reduce risks. While safer, the banks would be less profitable. A lot has changed over the last two years.

The Federal Reserve’s most recent proposal on bank capital requirements is a sizeable retreat from its more aggressive stance. Initially, in 2023, the Fed was pushing for a 19% capital requirement hike, but this was reduced to 9% in 2024. The Fed is now floating a more modest 3% to 7% increase for most major banks. It seems Wall Street’s argument that heavier capital rules would choke lending and economic growth rang true with the Fed. This shift, now under interagency review, aims to finalize regulations without the gridlock that stalled prior efforts. While the proposal would be good for bank profits, boost capital market liquidity, and allow for more bank stock buybacks, it risks undermining post-2008 safeguards that aimed to avoid another financial crisis.

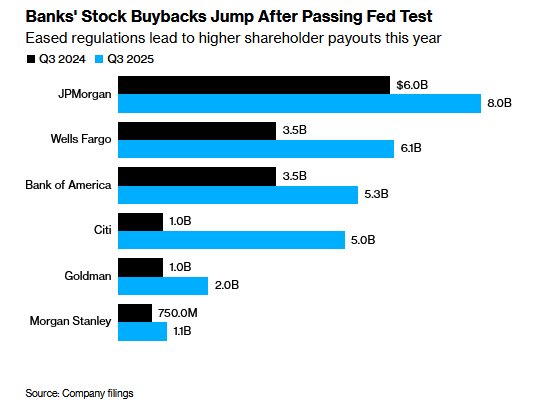

The graph and commentary below are courtesy Bloomberg:

Large banks have already shown more confidence in handing profit back to shareholders as regulators move to relax the enhanced supplementary leverage ratio and ease some aspects of the annual stress tests. The six biggest US banks boosted their stock buybacks by about 75% in the third quarter to more than $27 billion.

Dollar Debasement: Reality Or A Dangerous Narrative?

Gold prices are soaring. And with each tick higher, more and more market pundits and investors are coming out of the woodwork, asserting that dollar debasement is the reason. Is that the correct reason, or might gold be in a momentum-fueled speculative bubble like many other assets?

The answer has significant implications for the price of gold. If the answer is that reality aligns with current popular perceptions, gold prices—despite recent increases—may be fairly valued or even undervalued. However, if the answer reveals that the narrative is seriously flawed, gold prices could easily drop by 25-50% or more. To answer our questions, let’s examine the popular definitions of dollar debasement promoted by those supporting the dollar debasement theory to determine if they are valid.

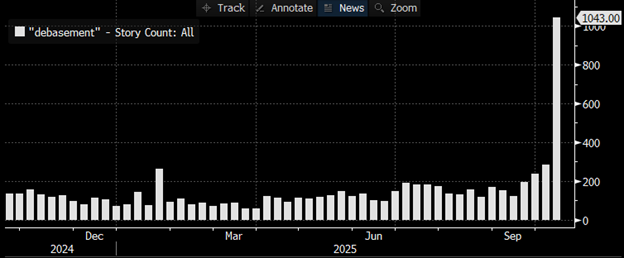

The following Bloomberg graph shows that the instances of media stories using the word “debasement” are soaring.

Tweet of the Day

More By This Author:

Leveraged ETFs: Yet Another Sign Of Rampant SpeculationJoe Weisenthal’s Take Down Of The ‘Debasement’ Trade

Speculative Bull Runs And The Value Of A Bearish Tilt

Comments

Log in or sign up to join the conversation.