The Wall Street consensus forecast for 2026 earnings growth is strong by historical standards. Analysts are giddy and projecting another year of double-digit growth in S&P 500 earnings per share (EPS). FactSet’s most recent data showed an expected 2026 earnings growth rate for the S&P 500 of about 15 percent. That is well above the long‑term average of roughly 8–9 percent. If FactSet is correct, such would mark a third consecutive year of double‑digit earnings gains.

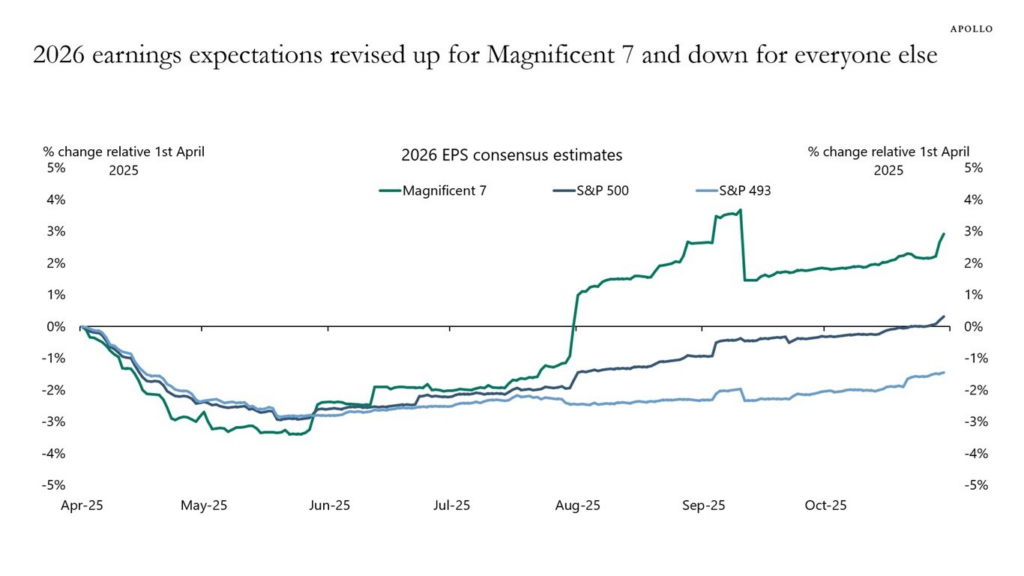

Notably, the 2026 earnings assumptions are driven by the continued strength in the large technology and communications sectors. With those sectors dominated by the “Magnificent Seven,” it is hoped that they continue to contribute disproportionately to earnings growth. Those seven companies alone are forecast to grow earnings strongly once again. As shown, since 2018, there has been very little earnings growth from the bottom 493 companies.

Furthermore, despite the exuberance from Wall Street analysts regarding the overall index, expectations for 2026 earnings improved only for the top seven companies, while estimates for the bottom 493 have seen virtually no change since April.

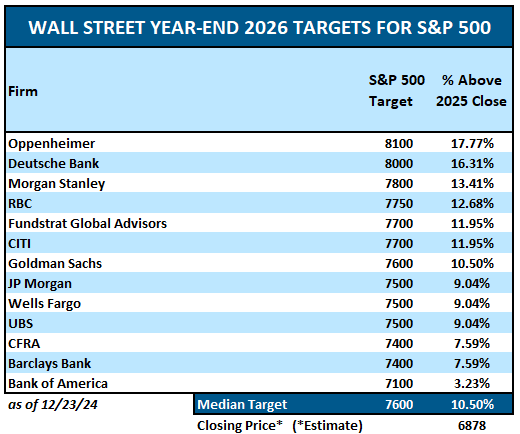

Notably, these 2026 earnings forecasts are influenced by broader market return expectations. For example, many sell‑side strategists are assigning S&P 500 price targets that embed this earnings growth outlook. For example, as shown, current analysts’ forecasts imply that the index could rise between 8% and 17% in 2026. However, to justify that price increase (P), they assume an earnings (E) rate that keeps valuations (P/E) stable.

In other words, Wall Street hopes that earnings expansion rather than valuation multiples will drive market gains. However, over the last 5 years, multiple expansions led the charge as earnings growth failed to keep pace.

This optimism currently comes against a backdrop of a resilient U.S. economy. GDP growth forecasts center on continued expansion, albeit modest, with some estimates indicating annual growth of around 2 percent. That stability reinforces the case for continued corporate profitability. One support is fiscal policy from the recently passed OBBB, which provides tax relief and deregulation. Still, this type of projected growth is not guaranteed. As such, investors should recognize that earnings forecasts reflect analysts’ estimates at a given moment, which is always “bullish” to ensure that Wall Street can sell you products.

As we previously reported, the accuracy of analysts’ estimates is far down their list of concerns.

However, instead of focusing on Wall Street estimates, which will likely be revised lower in the future, investors should pay closer attention to what will drive 2026 earnings growth.

The Link Between Economic Growth, Profit Margins, and Earnings

Earnings growth does not occur in a vacuum. Corporate profits are inherently a function of economic growth, pricing power, input costs, and labor dynamics. If the economy grows at a moderate pace, as most anticipate, corporate revenues are expected to expand in line with broader demand. Many forecasts for GDP growth in 2026 hover around the 1.8% to 3% range. Those estimates are driven partly by fiscal support and ongoing investment in sectors such as technology and infrastructure. This modest expansion provides a supportive backdrop for 2026 earnings, as historical correlations suggest. (Outliers are historically a function of recovery or impact from a crisis or recession)

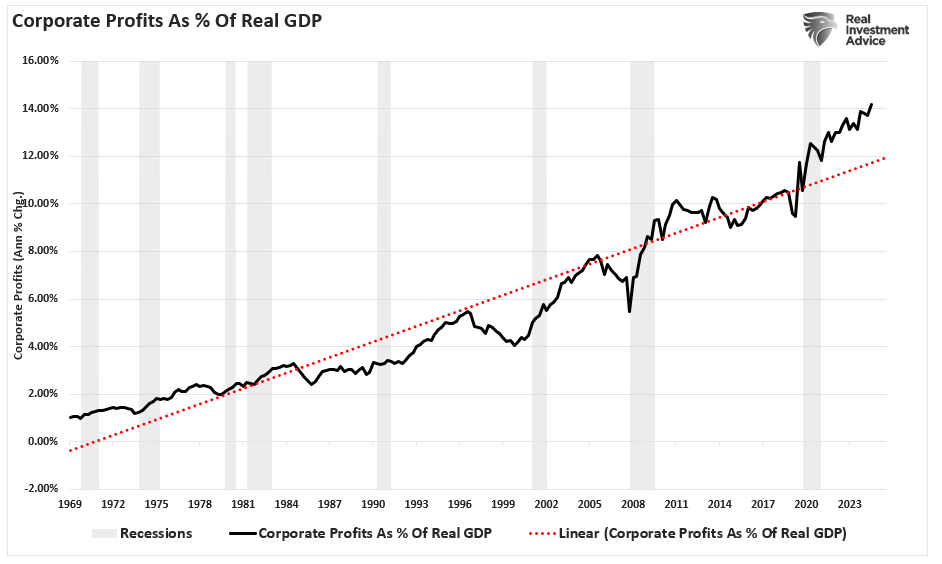

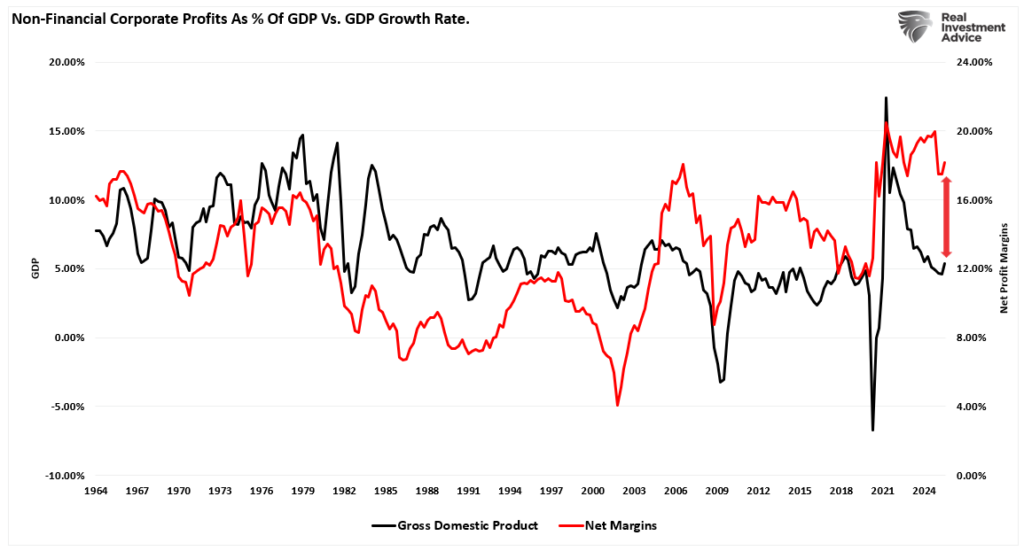

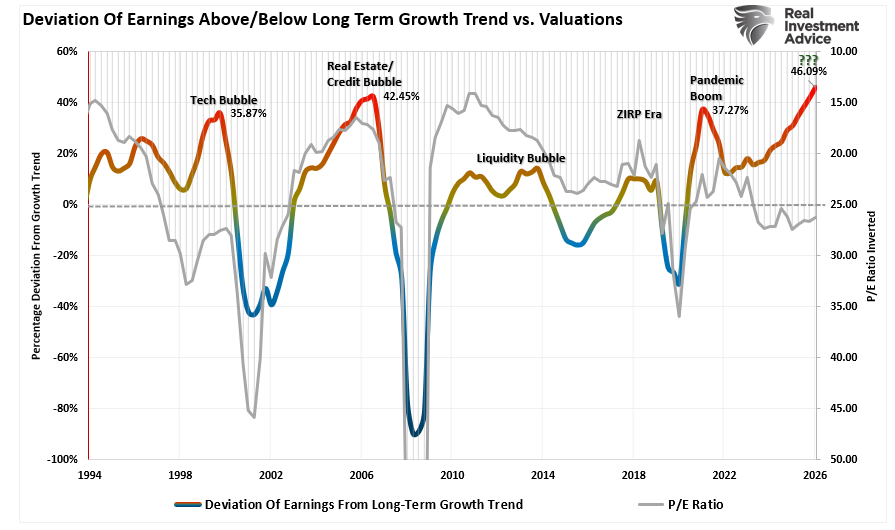

At the same time, corporate profit margins in the S&P 500 are currently very high relative to historical norms. According to FactSet, the estimated net profit margin for the index is near its highest level since tracking began in 2008, at around 13.9%, compared to a ten-year average of 11%. We also see this in corporate profits as a percentage of real economic growth, which is at its highest deviation from the long-term profit growth trend in history.

Elevated margins suggest companies have maintained pricing power and cost control, even amid inflationary pressures. But these high margins raise questions about sustainability. Given the supply-demand imbalances (more demand than supply), which allow for elevated margins, it is worth noting that as the economy returns to more normalized growth rates, profit margins tend to follow. Such is particularly the case as inflation pressures subside, employment weakens, and competitive forces erode pricing power. Margin compression has historically dampened earnings growth. Even if revenues are rising, if rising costs cannot be passed on to consumers, they eat into profits.

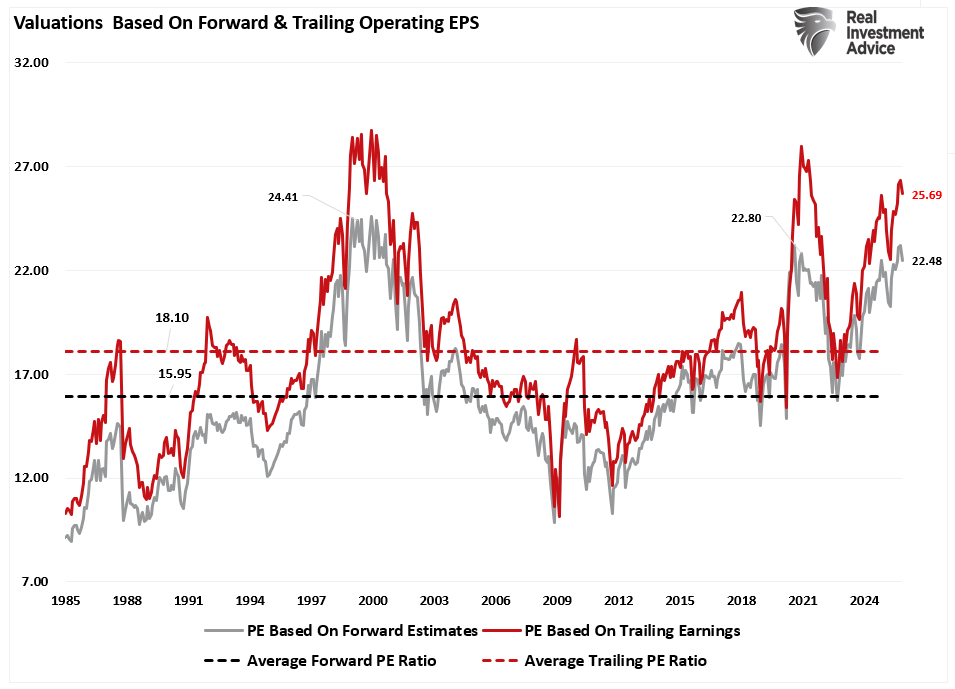

Valuations also matter. As noted above, the current price-to-earnings ratio for the S&P 500 remains above historical averages, at approximately 22x forward earnings. Those valuation levels are also well above the five- and ten-year averages. In other words, the market is pricing in continued earnings momentum. Therefore, if growth slows toward historical norms or margins compress, elevated valuations will mean even modest earnings disappointments could result in share price declines rather than gains.

The most considerable risk to investors is that the 2026 earnings estimates, which are the most deviated above its 125-year growth trend, disappoint, and the markets reprice lower. As shown, historically, when earnings become deviated from actual economic activity, the mean reversion process is not kind to investors.

In this context, understanding the mechanics behind earnings expectations becomes critical. Analysts’ expectations for robust earnings growth assume that these economic and profit margin conditions remain supportive; however, any divergence from this script increases the risk of downward earnings revisions, valuation compression, and market volatility.

Analyst Optimism, Valuation Risk, and Structural Challenges

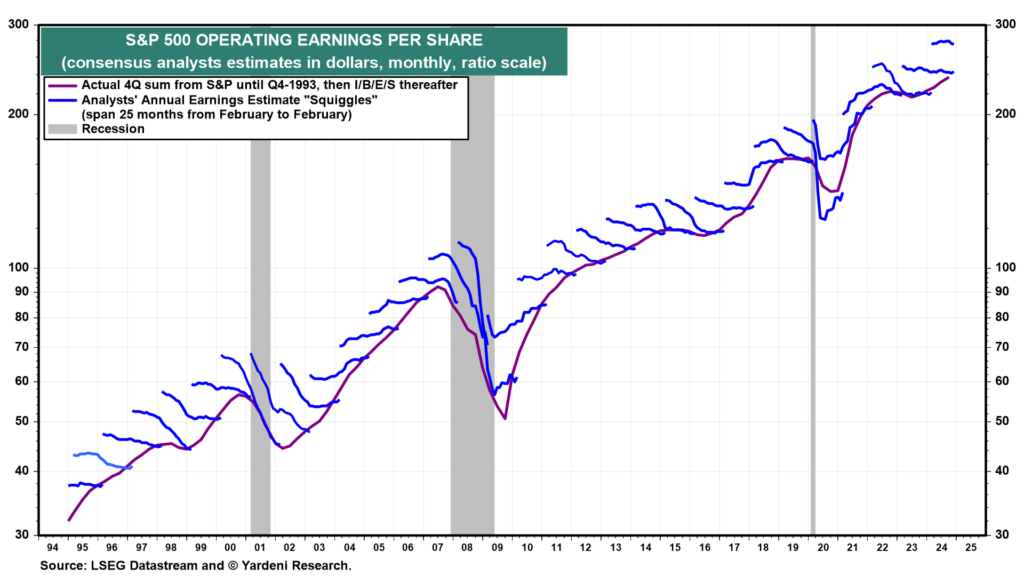

One of the enduring themes in earnings forecasting is the bias toward optimism early in the forecast cycle. Analysts typically issue forward earnings estimates at the start of a year and revise them lower later as actual economic and corporate results become available.

As noted above, such optimism is partly behavioral and partly structural; analysts often have incentives tied to institutional clients who favor growth narratives. When growth assumptions falter due to weaker demand, rising costs, or unforeseen macroeconomic shocks, analysts will typically revise their estimates downward. This creates the familiar pattern of “estimates drifting lower” over the course of the reporting year.

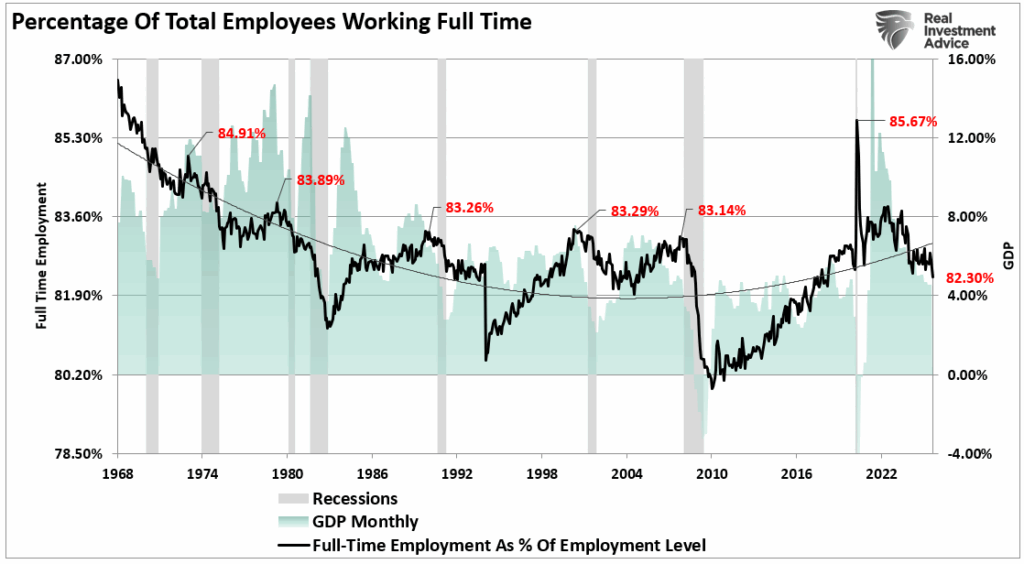

The current earnings growth consensus for 2026 is no exception. While forecasts indicate roughly 12.5–15% EPS growth, several structural vulnerabilities underpin these expectations. As discussed, profit margins are at elevated levels, which makes sustaining margin levels challenging in an environment where employment is declining.

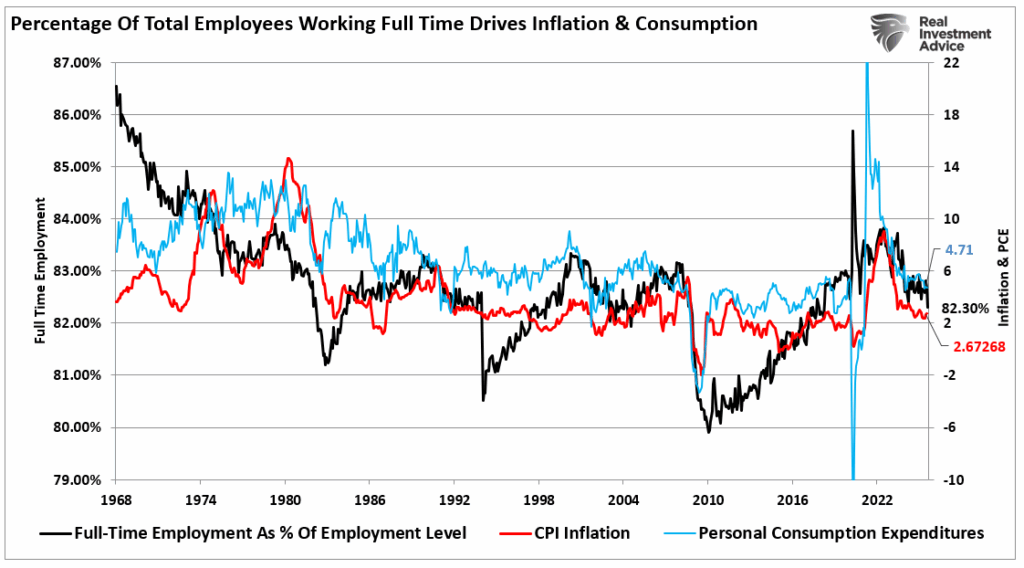

Given that full-time employment is declining, which correlates with the reversal of economic growth rates, it is unsurprising that inflation and personal consumption are also trending lower. This is because employment, particularly full-time employment, supports economic supply and demand.

Second, sector concentration risk is significant. A significant portion of projected 2026 earnings growth stems from a small group of mega-cap technology companies. If these firms underperform or face regulatory, competitive, or macroeconomic headwinds, the impact on aggregate earnings could be disproportionately large. A concentrated earnings base magnifies downside risk because fewer companies are carrying the growth load. As we noted previously:

“While technology and AI-driven firms have recently become bright spots, their strength cannot offset broader corporate margin pressures. In Q2, S&P 500 earnings grew 6.4%, with 80 percent of companies beating estimates. But this masks a weakening breadth of growth, where earnings beats are concentrated in essentially just two sectors. There would have been no earnings growth without Megacap Technology and major Wall Street banks.”

Lastly, valuations remain historically high. Elevated price‑to‑earnings ratios reflect market confidence in future earnings growth. But high valuations also reduce the margin for error. If growth falls short of expectations, a multiple contraction is a likely outcome, resulting in stock price declines even if earnings do grow. Several market strategists caution that nearly all favorable assumptions must materialize for current valuations to be justified.

While analysts note that policy factors, such as deregulation and potential tax incentives, are a tailwind for earnings, their actual impact remains uncertain. Policy implementation timing, regulatory uncertainties, and shifting political landscapes can blunt or delay these effects. Investors should note that fiscal tailwinds often operate with lags and can be offset by rising costs elsewhere in the economy.

As such, investors should consider several key factors in 2026.

- Expect Earnings Revisions: Analysts are historically optimistic in their early forecasts, and downward revisions are standard. Investors should monitor quarterly earnings guidance and track earnings revisions as one of the earliest indicators that actual performance may diverge from consensus. Early downward revisions often precede broader market corrections, so maintaining a disciplined watch on guidance can help you adjust risk exposure sooner.

- Focus on Quality Over Momentum: Higher‑quality companies—those with strong balance sheets, consistent free cash flow, stable profit margins, and resilient business models—tend to outperform during periods of earnings disappointment. When consensus growth slows, lower‑quality or speculative names typically experience sharper drawdowns. Allocating capital toward quality can reduce downside risk.

- Manage Valuation Risk: With forward price-to-earnings ratios above long-term averages, it is crucial to stay mindful of valuations. Avoid chasing valuations that imply perfect outcomes. If earnings growth disappoints, valuation compression is likely to occur. Use valuation metrics, such as the PEG ratio, to assess whether growth prospects justify current prices.

- Monitor Economic Indicators: Keep a close eye on key macroeconomic data, including GDP growth, inflation trends, and labor market indicators. These indicators directly influence corporate revenues and margins. Early signs of a slowing economy or rising inflation pressures should prompt reevaluation of equity risk exposure.

- Diversify Beyond the U.S. Market: The U.S. market valuations are high and heavily concentrated in a handful of mega‑cap tech names. Diversifying into international equities or sectors less dependent on narrow profit drivers can reduce concentration risk. Other markets may offer stronger valuations and more attractive earnings prospects if the U.S. slows.

- Use Defensive Instruments Appropriately: In periods of earnings uncertainty, adding defensive instruments—such as high-quality bonds, low-volatility equities, or hedging strategies—can help mitigate downside risk. These positions typically underperform during strong rallies but provide ballast when earnings or economic data disappoint.

- Prepare for Volatility: Volatility increases when analysts reduce earnings forecasts, and uncertainties mount. Investors should adopt a tactical approach that accounts for higher volatility, utilizing position sizing and stop-loss discipline to protect their capital. Volatility indicators such as the VIX can serve as early warning signals.

- Revisit Fiscal and Policy Tailwinds: Assess how fiscal policy changes—such as tax incentives or deregulation—are actually impacting corporate profitability. If intended policy benefits fail to meet expectations, earnings momentum may weaken. Staying attuned to policy developments helps recalibrate expectations and positions.

Just remember, while all analysts are very bullish about 2026, there is no guarantee.

More By This Author:

Fannie And Freddie To The Rescue

Investor Lessons From 2025 For 2026

New Year’s Resolutions For 2026 – Investor Version

Comments

Log in or sign up to join the conversation.