Image Source: Pexels

US core inflation posted a fourth consecutive 0.3% print, showing that progress towards the Fed inflation goal has clearly stalled. Nonetheless, the Fed’s favored measure of inflation is doing a little better and the jobs market is cooling. We look for another 25bp Fed cut next week, but new Fed forecasts should show a shallower series of cuts in 2025.

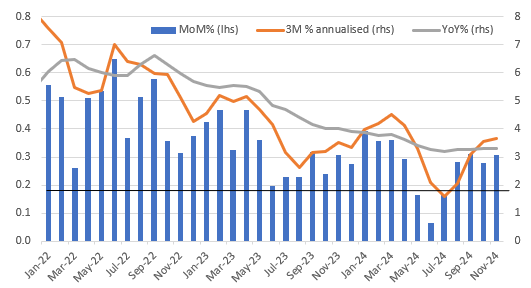

Inflation remains too hot for comfort

US core CPI in November has come in at 0.3% month-on-month, as expected, and the headline has done likewise. The year-on-year headline rate ticks up to 2.7% from 2.6% while the annual core rate has remained at 3.3%. The details show housing looking a little more benign with owners' equivalent rent and primary rents coming in at a pleasing 0.2% MoM, apparel posting a similar increase, and education and communication prices falling 0.4% MoM. The upside pressure largely came from vehicle prices with new vehicles rising 0.6% MoM and used vehicles jumping 2% MoM after a 2.7% increase in October. Most other components came in at around 0.3%.

US core CPI metrics

Source: Macrobond

Fed to cut more cautiously from now on

This is the fourth consecutive 0.3% MoM print and as the chart above shows, the annual inflation rate has stalled at just above 3% for the past six months while the 3M annualized rate has picked up markedly since the summer. To be confident inflation will return to the 2% YoY target we need to see the MoM rate (blue bars) track at 0.17% MoM over time (the black line). It is simply too hot right now. That said, with PPI expected to post a 0.2% increase tomorrow we should be on course for a 0.2% MoM print for the Fed's favored inflation measure – the core PCE deflator – next week.

In terms of implication for policy, the jobs market is cooling and the Federal Reserve repeatedly acknowledges that monetary policy is still in restrictive territory. As such, the Fed appears happy to gradually move policy closer to the neutral level of around 3% and we expect another 25bp rate cut next week. However, the lack of meaningful progress on inflation means that in their summary of economic projections, officials are likely to signal just three rate cuts in 2025 versus the four they projected in September.

More By This Author:

FX Daily: What Today’s BoC Decision May Mean For The Fed And The Dollar

Rates Spark: Sizeable Rate Moves Expected In 2025

Czech Headline Inflation Remains Unchanged

Comments

Log in or sign up to join the conversation.