Guest post by Marc Rubinstein

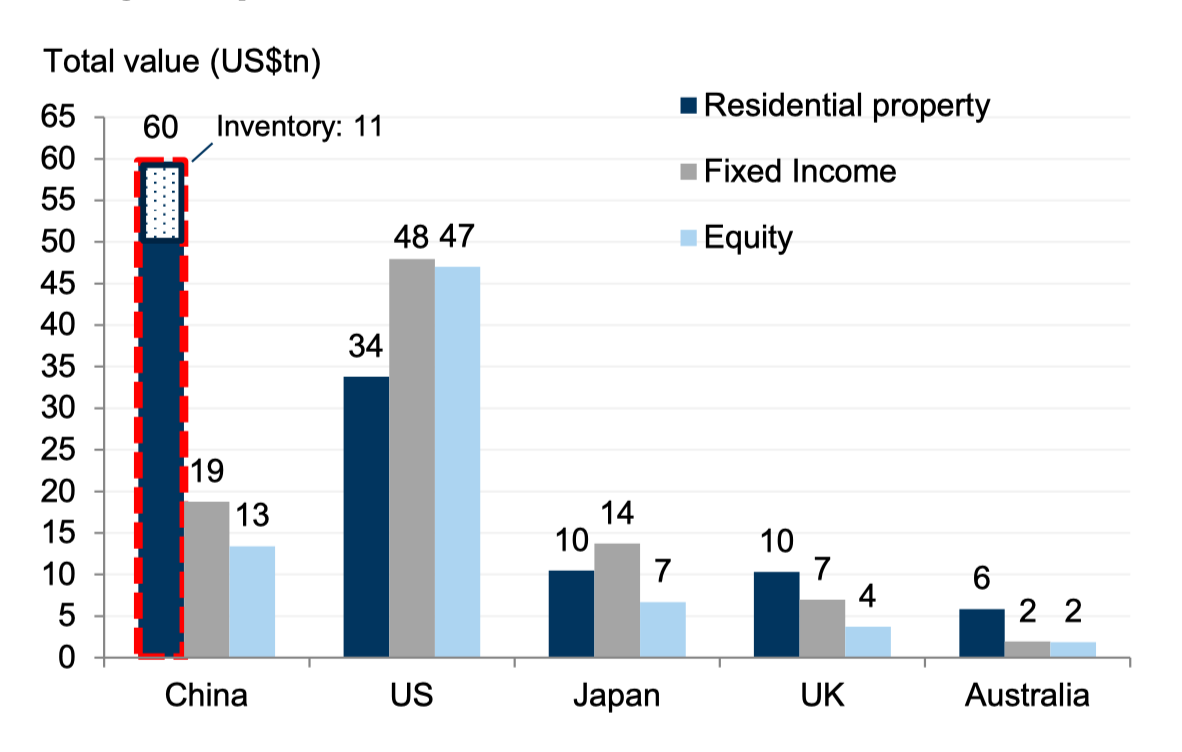

It’s been described as “the most important sector in the universe” and it’s easy to see why. The Chinese property sector is first and foremost big. The total value of all the homes in China stands at $60 trillion – twice the size of the US residential market and bigger even than the entire US bond market. The Chinese property market is probably the largest asset class globally.

(source: WFE, CEIC, Japan Cabinet Office, Halifax, Goldman Sachs Global Investment Research)

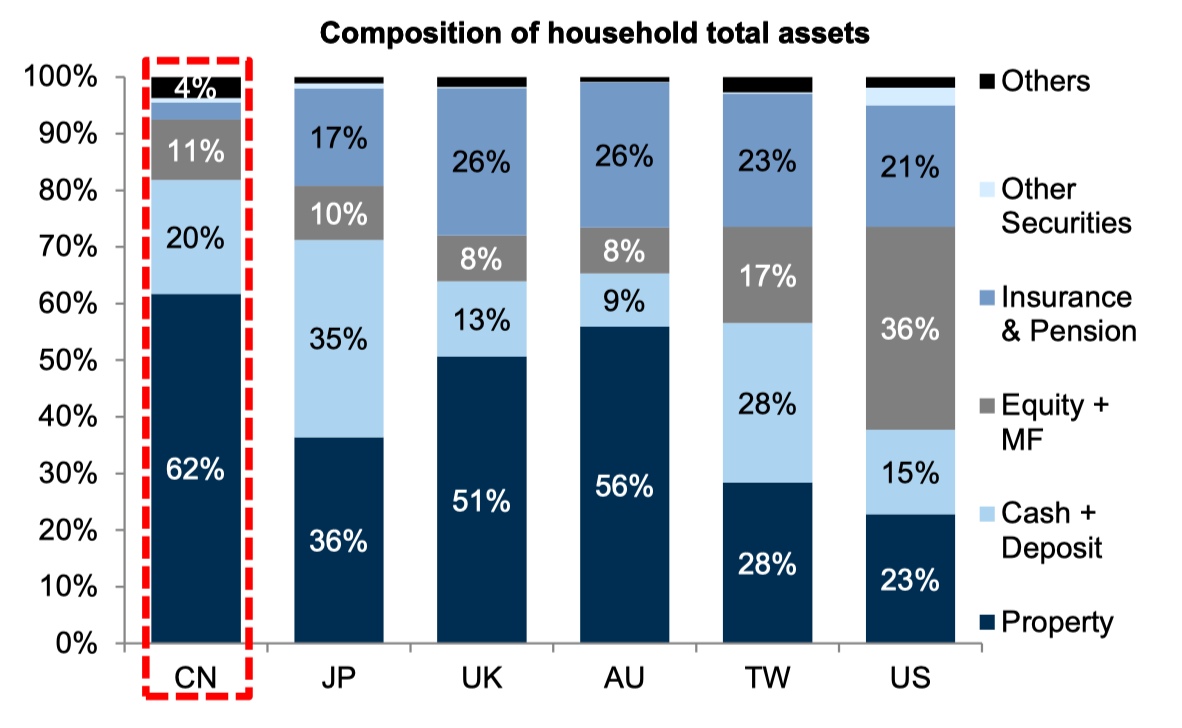

It’s also central to the economy. Real estate investment stood at over 13% of GDP in 2019, of which more than 70% was linked to residential building. Add in the contribution of the construction industry and the share jumps closer to 29%. Yet even this potentially understates the importance of property to the economy: Housing accounts for almost two-thirds of households’ overall assets – compared with around a third in Japan and a quarter in the US – so it has a major bearing on people’s spending decisions. [1]

It’s central to government finances, too. Since changing its constitution to allow land-use rights to be bought and sold under long term leases, the Chinese state has relied on land sales to raise funds to meet its budget. Based on data from the IMF, revenues from land sales accounted for around 39% of local government revenues, equivalent to 7% of GDP, in 2017.

And it’s central to the financial system. Banks rely on real estate and land holdings as the main source of collateral to secure loans. Housing loans account for around a third of banks’ loan books and have grown more quickly than other loan categories. In the four years through to 2018, the average annual increase in real estate credit was 20%, versus 6% in manufacturing.

So when the biggest star in the most important sector in the universe burns out, you’d think it would have ramifications. That star is Evergrande, which we discussed here a year ago. One of the largest property developers in China, it found itself on the wrong side of three “red lines” that Chinese authorities had drawn to curb leverage in the sector. Having grown aggressively using borrowed funds, it buckled under the new guidelines and creditors began to take fright.

Behind the scenes, policymakers mobilised to gauge the fallout. In June 2021, China’s financial regulator instructed banks to conduct a stress test around an Evergrande failure. The conclusion was plainly that banks could handle it. In December, China’s central bank governor ruled out a state-sanctioned bailout, proclaiming that the situation would need to be dealt with by the market: Evergrande was on its own. Later that month, the company skipped payments on coupons due on US Dollar denominated debt and credit rating agencies officially categorised it in default.

Evergrande bond price (source: Bloomberg)

Since then, Evergrande has been working on a restructuring, but with its bonds trading at eight cents on the dollar, creditors don’t harbour much hope of recovery. This week, the company’s CEO and CFO both resigned amidst an investigation into how $2 billion of deposits were used as security for third parties to obtain bank loans, which some borrowers then failed to pay back. Before they departed, they had promised to release a preliminary restructuring plan by the end of July and today, the company provided some rough details with a full plan to come later in the year.

Against the backdrop of a slowing real estate market, other developers got squeezed, too. In the first half of 2022, property sales dropped by 29%, land sales plummeted by 50%, and average home selling prices fell by 5%. New home prices have now slid for 10 consecutive months and sales have fallen for 12 straight months, the longest slump since China created a private property market in the late 1990s.

Monthly change in China 70-city home price index

Evergrande may have been the largest, but it wasn’t the only property developer to default on debt. Since the beginning of last year, 35 property companies have skipped bond payments. Shanghai-based Shimao Group is one of the latest to be added to the list, having failed to pay off a $1 billion offshore bond earlier this month. Currently, around three-quarters of Chinese property high yield bonds are priced below 35 cents on the dollar, signalling significant stress.

Initially, the financial regulator’s analysis that the banking sector could be sheltered from the real estate stress proved correct. Most defaults were restricted to developers’ offshore debt; even Evergrande has remained current on its onshore debt (for now). Bank loans to property developers are typically well collateralised, and their direct exposure to developers is in any case not that high – only around 6% of average loans among the larger banks.

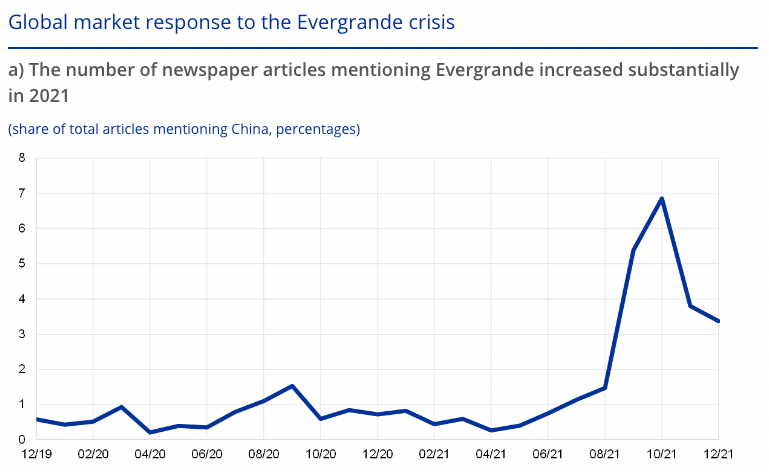

So for a while, banks chugged along. Evergrande newsflow peaked in September and then the world forgot about it. Crisis averted.

Shares of newspaper articles mentioning Evergrande of total articles published on China in the Wall Street Journal and the South China Morning Post. (source: ECB)

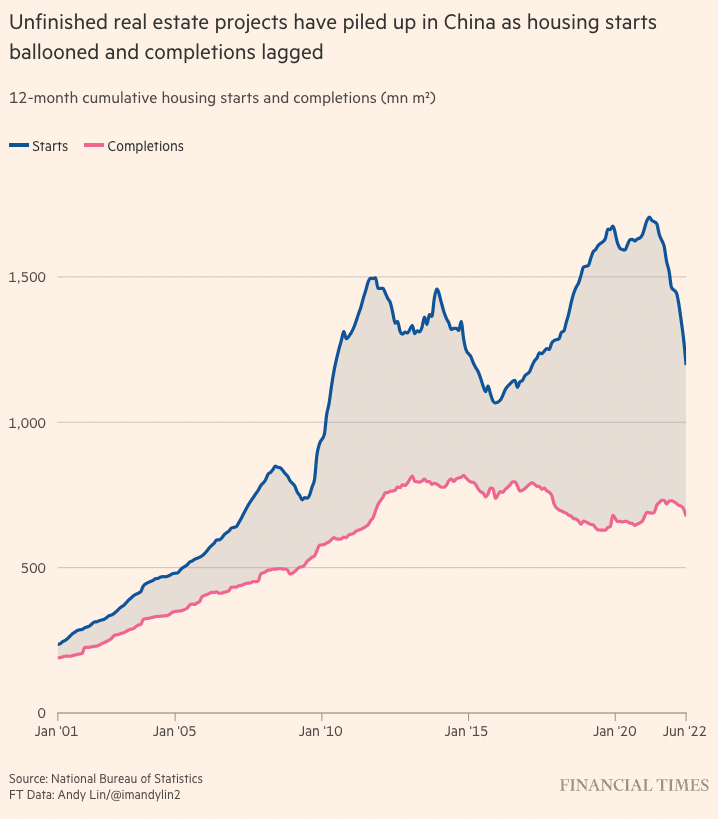

But then, people stopped paying their mortgages. In late June, around 900 residents in the southeastern province of Jiangxi stopped making repayments on loans they had taken to finance Evergrande apartments whose completion had stalled. Within weeks, the boycott spread to at least 300 equally unfinished projects across more than 90 cities. [2]

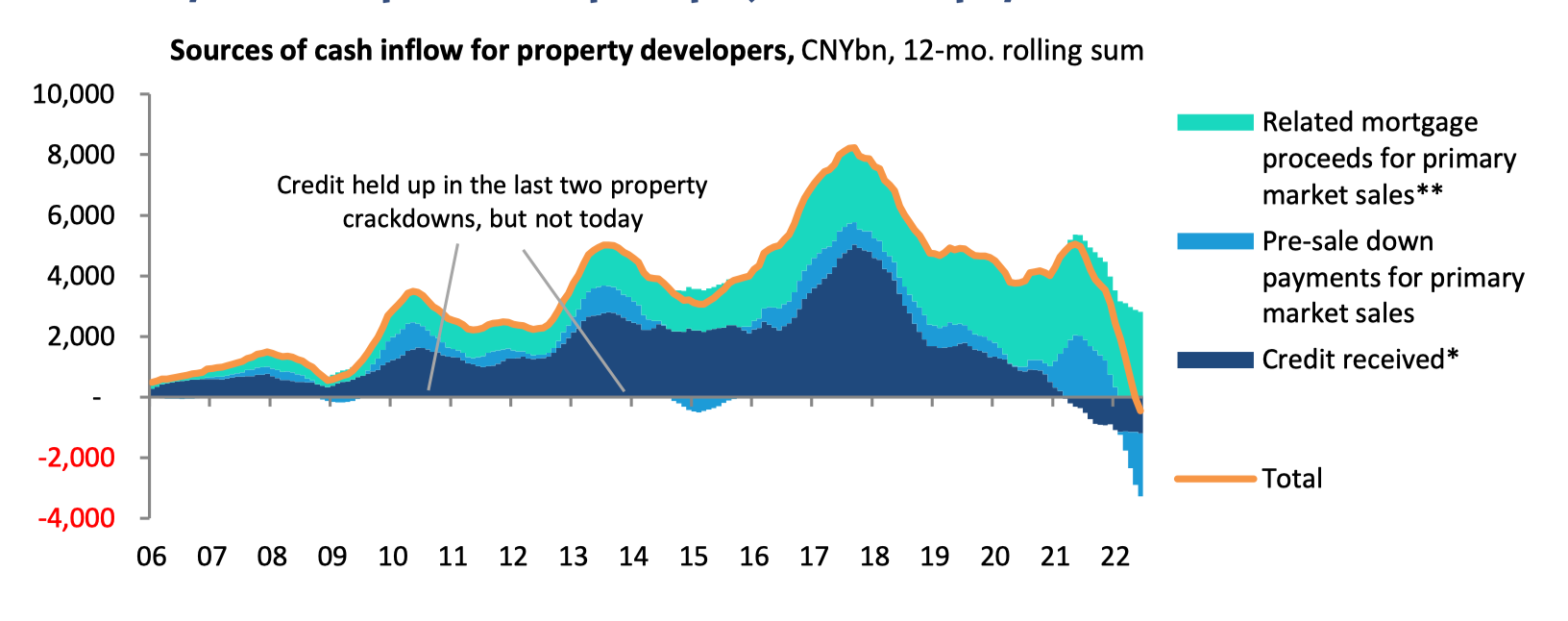

The issue is that traditional credit, be it from banks or bond markets, represents only a part of Chinese property companies’ funding. In addition, developers raise funds through pre-sales. Purchasers make down payments into a developer’s escrow account some 18-24 months before taking delivery of their home which are then topped up via mortgage loans. These funds would normally be sufficient to cover the remaining cost of construction of the project, but developers have a history of mismanaging them. When the market was strong, it didn’t matter – incoming funds from new pre-sales compensated for the misallocation of historic funds. But when the market turned – and traditional credit channels turned off their supply of new credit – many developers ran out of funds to complete projects. Instead of using escrow funds to build homes, many raided them to meet other liquidity needs.

*Property developer loans, trust credit, on- and offshore bonds.

**Based on primary market sales ratio in 23 cities and includes housing provident fund loans.

(source: CEIC, Wind, Autonomous Research)

Sounds a bit like a Ponzi scheme? As liquidity has retrenched the world over, schemes sustained by steady inflows of cash have begun to falter. That’s been the case across the crypto ecosystem and it’s been the case in venture too, as we discussed two weeks ago in The Great Unwind. Chinese real estate is another, larger example where the ripple effects are now being felt.

It’s no wonder borrowers are refusing to pay. As well as paying rent or covering the cost of finance on their existing home, they are paying a mortgage on a new home they are unsure when they will get possession of, if at all. Unfinished residential projects across China represent only 1.7% of total outstanding mortgage loans so it’s not a huge exposure for the banks, but it is a lot riskier than they anticipated: The loans are guaranteed by property developers, so what looked money-good in 2019 and 2020 looks decidedly less so now.

To stave off the crisis, authorities are reportedly putting together a national fund of up to RMB 300 billion to help complete unfinished projects. Just as the Federal Reserve keeps one eye on the stock market as a gauge of conditions it helps maintain, and the European Central Bank looks at peripheral bond spreads, Chinese authorities look at home prices. President Xi stresses that houses “are for living in, not for speculation,” but they nevertheless represent a significant proportion of household wealth and any damage has wide implications. Attention is particularly focused right now, in the run up to the China Party Congress later in the year.

(source: NIFD, CEIC, Wind, Japan Cabinet Office, Halifax, Goldman Sachs Global Investment Research)

For years, people have been waiting for the Chinese financial system to implode. In 2015, hedge fund manager Kyle Bass, who had been early to the troubles of the US financial system in 2006, wrote to his investors: “Similar to the US banking system in its approach to the Global Financial Crisis (GFC), China’s banking system has increasingly pursued excessive leverage, regulatory arbitrage, and irresponsible risk taking. Banking system losses – which could exceed 400 percent of the US banking losses incurred during the subprime crisis – are starting to accelerate.”

Since then, we’ve seen several waves of negative profit growth but no significant erosion of book value. A government bailout of unfinished homes would prevent such an erosion from occuring now. More generally, Chinese mortgage loans have a number of features that mitigate their risk. One is the high rate of down payment that borrowers are required to make – 30% for first time buyers and 80% for second-home buyers. Another is that, unlike in the US, banks are able to pursue a borrower’s other assets if they default on their mortgage. So although boycotts are currently rife, ongoing strategic defaults are less likely. Finally, rising home prices in the past (+68% between 2015 and 2018 in major cities) have created a sizable buffer to cushion mortgage loans.

In the US, property developer stress was the earliest sign of impending crisis: the sector peaked in 2005. The Chinese banking system is better capitalised today than the US system was back then, and the state has more tools available to contain losses. But it’s difficult to see how the most important sector in the universe can unwind without any collateral damage elsewhere. It’s a slow process, but it’s one that needs watching.

For more historical context on China financials, see my piece on Evergrande and my piece on the Chinese banking sector.

[1]Economists Kenneth Rogoff and Yuanchen Yang came up with the 29% estimate. It was subject to some criticism as too high, but the economists defended it in an addendum to their original paper in December 2021.

[2]Prior to mid-July, crowdsourced online documents tracked boycotts across the country. But then they were censored.

More By This Author:

Hollow Men, Hollow Markets, Hollow World

They’re Not Sending Their Best

What is Robinhood?

Comments

Log in or sign up to join the conversation.