I used to write all of my Epsilon Theory notes by starting with two or three or twenty quotes and images, so that the note wouldn’t really start until like … page 5. It was an affectation of the sort that a lot of new writers adopt, and I dropped it when I finally realized it had become a shtick.

But sometimes the old ways are the best ways. Eight years ago, here’s how I started a note that was also titled “Hollow Men, Hollow Markets, Hollow World“.

Apocalypse Now (1979)

| Kurtz: | Did they say why, Willard, why they want to terminate my command? | ||

| Willard: | I was sent on a classified mission, sir. | ||

| Kurtz: | It’s no longer classified, is it? Did they tell you? | ||

| Willard: | They told me that you had gone totally insane, and that your methods were unsound. | ||

| Kurtz: | Are my methods unsound? | ||

| Willard: | I don’t see any method at all, sir. | ||

| Kurtz: | I expected someone like you. What did you expect? Are you an assassin? | ||

| Willard: | I’m a soldier. | ||

| Kurtz: | You’re neither. You’re an errand boy, sent by grocery clerks, to collect a bill. |

I first saw Apocalypse Now as a college freshman with two roommates, a couple of years after it had been released, and I can still recall the dazed pang of shock and exhaustion I felt when we stumbled out of the theatre. Nobody said anything on the drive back to campus. We were each lost in our thoughts, trying to process what we had just seen. Our focus was on Marlon Brando’s Colonel Kurtz, of course, because we were 18-year old boys and he was a larger than life villain or anti-hero or superman or … something … we weren’t quite sure what he was, only that we couldn’t forget him.

When I reflect on the movie today, though, I find myself thinking less about Kurtz than I do about Martin Sheen’s Captain Willard. Both Kurtz and Willard were self-aware. They had no illusions about their own actions or motivations, including the betrayals and murders they carried out. Both Kurtz and Willard saw through the veneer of the Vietnam War. They had no illusions regarding the essential hollowness of the entire enterprise, and they saw clearly the heart of darkness and horrific will that was left when you stripped away the surface trappings. So what made Willard stick with the mission? How was Willard able to navigate within a world he knew was playing him falsely, while Kurtz could not?

Hollow Men, Hollow Markets, Hollow World (March 30, 2014)

Eight years ago.

Before Trump. Before Covid. Before a hot war with Russia and a cold war with China. Before Bitcoin became Bitcoin! ™.

It’s hard to remember the before-times, right? It’s hard to remember how alienated and disenchanted and hollowed-out we all felt THEN, even before all of the crap of the past eight years.

Forty years ago, as a teenage boy, I imagined myself as Kurtz, the anti-hero/superman/supervillain.

Eight years ago, as a 50-year-old man, I downgraded my imagination to Willard, the good soldier/assassin/errand boy.

Today? LOL. Ego is a powerful drug, and it takes events like those of the past eight years to draw it out of your system. Today I finally know who I am in Apocalypse Now, who we ALL are in its narrative arc terms.

I am a villager.

We are all villagers in Kurtz’s world, an unnatural, literally insane world created by proclamation and fiat. Sure, our standard of living may be a little bit better than in the picture above, but the essential hollowness is the same. Maybe worse. And now an implacable agent of change – in the movie it’s the assassin Willard but in the real world it’s inflation, war, disease and climate – has arrived to collect the bill that is due.

This is an Old Story.

I don’t just mean that Apocalypse Now was taken directly from Heart of Darkness, Joseph Conrad’s 1899 novel. I mean that the story of hubris at a societal level, where prideful human leaders lift themselves and their people up to unnatural heights by stealing what is not rightfully theirs, only to have their society struck down in retribution, is probably the oldest social narrative arc of them all.

And that is exactly what our Kurtzian leaders have done in the United States over the past 25 years. In their overweening pride, they have stolen what is not rightfully theirs to lift themselves and their people up to unnatural heights. Through monetary and fiscal policies that have pulled forward future growth and productivity into the present, they have not only stolen wealth and prosperity from our children and our children’s children, but they have also created a political dynamic that has hollowed-out the Constitution and its attendant political norms.

We are a husk of ourselves. A wealthy and pampered husk of ourselves, sure, where I find myself disappointed if the local liquor store has only five different artisanal mezcals to choose from, but a husk nonetheless. Sometimes I wonder what the 5th-century Roman equivalent of artisanal mezcal would have been.

How did this happen? Here, I’ll show you.

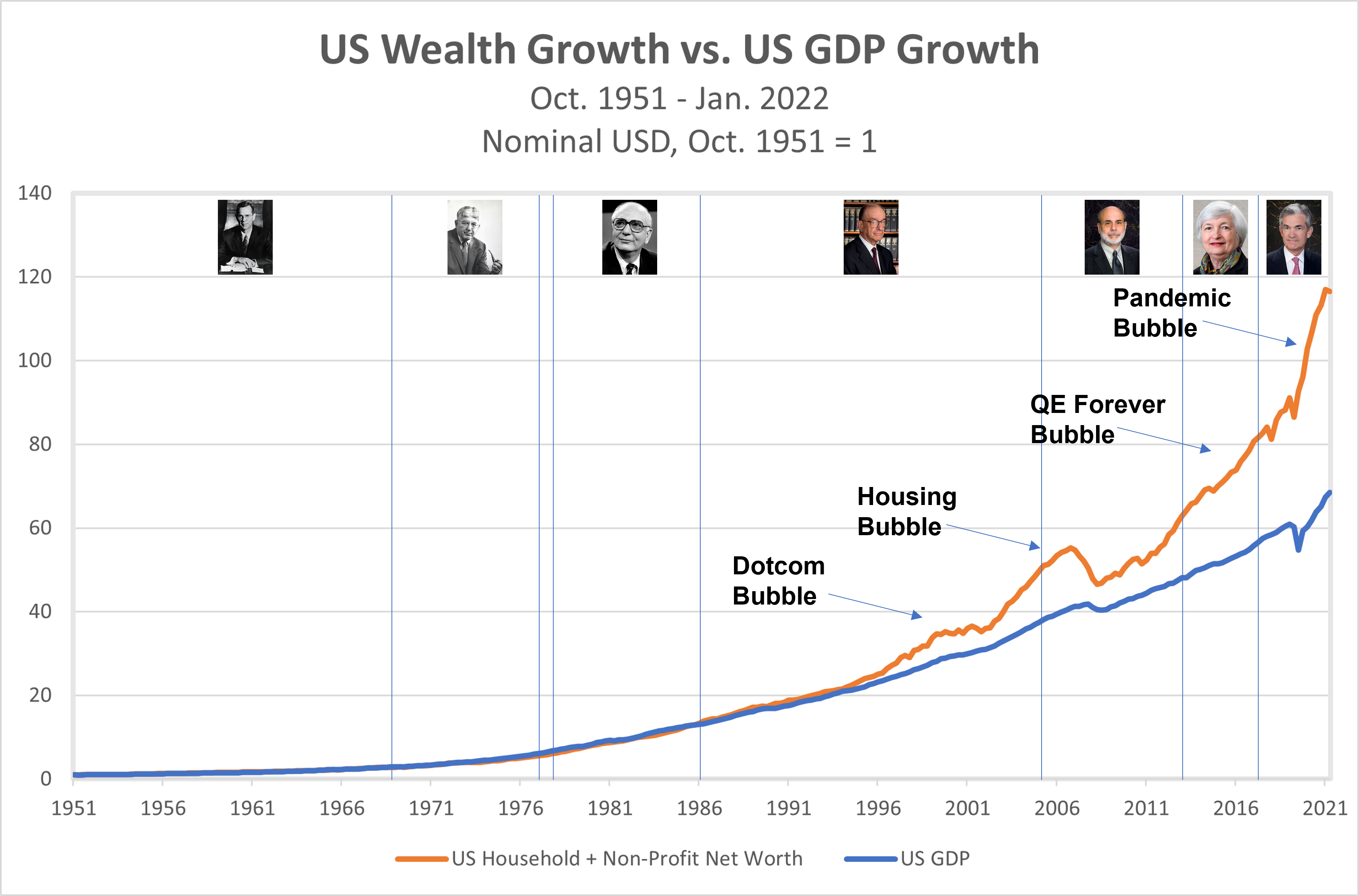

This is a 70-year time series of the growth in American wealth (US household and non-profit net worth) plotted against the growth in the American economy (US GDP). All of the data is from the St. Louis Fed’s FRED resource. I’ve superimposed the terms and headshots of Fed chairs over this period (that’s William McChesney Martin on the far left, followed by Arthur Burns, Paul Volcker, Alan Greenspan, Ben Bernanke, Janet Yellen and Jay Powell), along with the various major asset bubbles we’ve had since the path of US wealth growth diverged from the path of US GDP growth in the mid-1990s.

By using nominal dollar measurements we avoid issues of inflation, and by comparing growth rates we avoid issues of stock (wealth) vs. flow (GDP). Also, please don’t @me about log charts. They add absolutely nothing to the analysis here. This is a true apples-to-apples comparison between two things that, IMO, should typically grow together and pretty much in lockstep. That’s because I believe this:

As a people, you can’t be a lot richer than your economy grows without stealing that wealth from someone else.

Maybe it’s stolen (sorry, I mean extracted or taxed or traded for) from people in other countries through colonial terms of trade. Maybe it’s stolen (sorry, I mean pulled forward) from future people in your own country through artificially low interest rates, monetized debt-driven stimulus, and an increasingly levered financial system supporting increasingly non-productive mal-investment. Insert monocle-wearing Hmmm emoticon here.

By the way, nothing that I described in the prior paragraph is the exclusive or even predominant domain of one political party or the other. If you insist on saying, for example, that debt-driven stimulus policies are a Democratic party thing against which the Republican party stands in staunch opposition, then I will present you with a bound copy of the 2017 Tax Cuts and Jobs Act and just start laughing at you.

Also by the way, I believe that a modest national debt and modest leverage in the financial system are good things, not bad things. I believe that a gold standard is a pretty terrible way to run a monetary system. I believe that deficit spending is entirely justified across a pretty wide range of national exigencies. And as I’ll discuss at length in a bit, I believe that central banks play a crucial and necessary role in the modern world.

None of these things – a fiat currency, fiscal flexibility with the ability to take on substantial debt, an autonomous central bank with wide-ranging authority over monetary policy and financial system regulation – are at odds with the basic idea that our wealth as a people should grow hand in hand with the growth of our economy.

I know this is true, because that’s exactly what happened in the United States for almost 50 years.

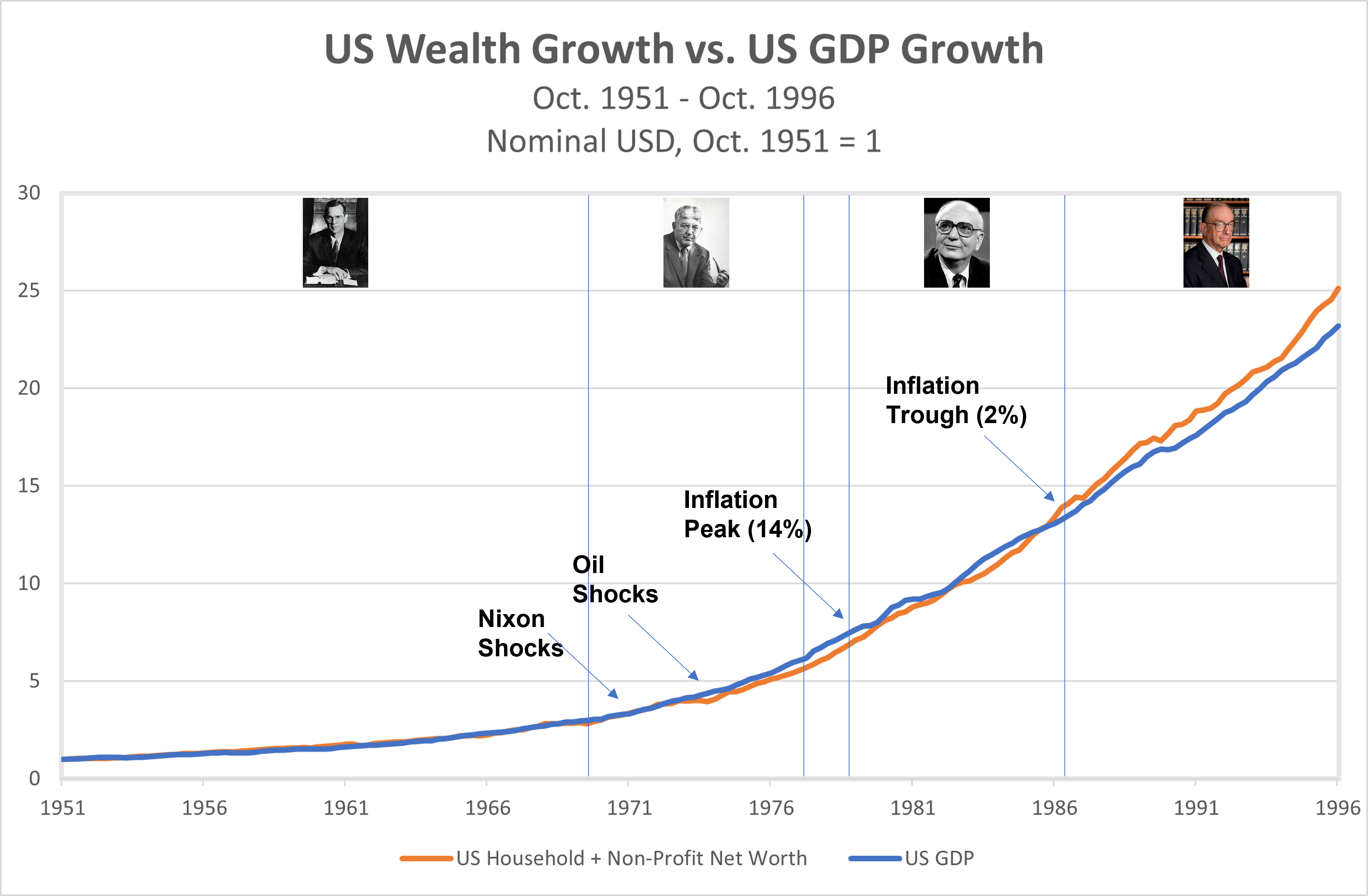

Here’s the same chart from before, but zooming in on the 1951 – 1996 period.

As you’d expect, the Nixon shocks in the early 1970s (ending the gold convertability of the dollar and punting the post-WWII Bretton Woods system) plus the OPEC oil shocks separated the absolute lock-step relationship between wealth growth and economic growth, but the two were still very much joined at the hip throughout the 1970s, 1980s and early 1990s, across the Fed chairmanships of Arthur Burns, William Miller (only 1 year, not pictured), Paul Volcker and the early days of Alan Greenspan. Not coincidentally, the 1970s were the last time we had embedded wage/price inflationary pressures in the United States (CPI peaked at 14% in late 1978, just before Volcker took the helm), and US monetary policy over this period was consumed by trying to bring inflation down by any means necessary. As a result, it would have been inconceivable in the Volcker Fed (1979-1987) and the early days of the Greenspan Fed to even consider using monetary policy to inflate nominal wealth levels without risking resurgent inflation in the real economy.

By the mid-1990s, however, it was all too conceivable. About halfway through Alan Greenspan’s 20-year (!) Fed chairmanship, the Maestro had a revelation: blessed by the Great Moderation (high productivity and low inflation expectations), the Fed could use monetary policy as a political tool to make us richer than our economy could grow, without re-triggering wage/price inflation in the broader economy.

By keeping interest rates lower than what would have been considered ‘normal’ over the prior few decades and by relaxing regulatory constraints on derivative securities, banking regulations and the like, Greenspan believed that he could inflate home prices and financial asset prices without hitting wages and prices more broadly.

Now that’s a neat trick! Sure there would be occasional bouts of “irrational market exuberance”, like the Tech Boom (and crash) of 1999-2001, but that’s a small price to pay for the pareto-superior (how’s that for a ten-dollar word!) wealth outcomes provided by activist monetary policy.

This was the birth of our insanely financialized world.

I’ve included red arrows to show the slope or speed of the growth in US wealth at different periods over the past 25 years, as well as green arrows to show the slope or speed of the growth in US GDP. The plain graphical interpretation is exactly what you think it is – every Fed chair since Greenspan has not just continued the separation of wealth growth from GDP growth, but has accelerated that separation.

Ben Bernanke was the first to double down on Greenspan’s epiphany, and he achieved that acceleration by expanding the instruments by which monetary policy could inflate financial assets directly. The most obvious new instrument was what became known as ‘quantitative easing’ or QE, which covers a wide range of balance sheet actions. In simplest terms, QE just means buying enough stuff (‘large-scale asset purchases’, in the lingo) to drive the price of that stuff up and the yield of that stuff down. This has two big effects:

First, if you buy enough of something that’s fundamental or a reference point for how all borrowing is priced, like US Treasuries, then artificially pushing the price up and the yield down on that fundamental thing should make all borrowing cheaper. This is the essence of pulling forward investment from the future. By making the price of borrowed money artificially lower, you encourage companies and households to borrow money today and buy something with it … a new factory, maybe, if you’re a big company, or a new car, maybe, if you’re a household. And if the country is in the middle of the worst Depression since the 1930s and everyone is losing their job and no one is buying a new car, then pulling forward some investment from the future so that the present day doesn’t absolutely collapse makes a lot of sense! But if that’s not the situation … well, hold that thought.

Second, artificially pushing the price up and the yield down for something that is fundamental to every investment portfolio, like US Treasuries, means that all of the retirees and pension funds who buy US Treasuries and are counting on that yield as income to fund their retirement or their obligations are going to be forced to buy riskier assets, like mortgage-backed securities or dividend-paying stocks, to get that same level of income. This is called the ‘portfolio channel effect’ in the official lingo, but you may also hear it referred to as ‘financial repression’, especially if you get to the point of a yield or interest rate of zero, so that savers don’t get any income at all from holding their government bonds. And if you have negative interest rates, such as have been commonplace in Europe over the past 5 years or so, then savers and retirees are truly forced to do something substantially risky with their money. Now again, if you’re in the middle of the worst Depression since the 1930s and no one is willing to invest any money in any stock for fear that the entire financial system is about to collapse, then prodding everyone to take more risk than they’d otherwise be comfortable with makes sense. I’m not crazy about the nudge, but I get it!

That situation – the worst Depression since the 1930s, where everyone is losing their job and no one is willing to invest any money in anything, and everyone is afraid that the entire financial system is about to collapse – is exactly what Ben Bernanke and the Fed faced in early 2009. I think that the emergency action they took then, what became known as QE1, is totally fine. More than fine. Honestly, I think that QE1 saved the world. I think that QE1 was exactly why central banks were invented in the first place – to provide emergency liquidity in incredible quantities when everyone else is too scared to do it. It’s like that scene in Pulp Fiction when John Travolta plunges the syringe of adrenaline straight into Uma Thurman’s heart. The Fed is Travolta, Thurman’s heart is the global economy, and the adrenaline is QE1.

No, the problem wasn’t QE1. The problem was QE2 and QE3 and QE-infinity. The problem was turning a $2 trillion balance sheet with the completion of QE1 into a $9 trillion balance sheet today! The problem was turning a one-time straight-in-the-heart shot of adrenaline into a permanent intravenous mainline of adrenaline.

The problem – like it always is in this Old Story – was the transformation of emergency government intervention into permanent government policy.

The problem – like it always is in this Old Story – was the hubris of people like Ben Bernanke and Janet Yellen, who honestly believe that it is not only possible to rescue an economy through monetary policy, but that it is also then possible to control an economy through monetary policy.

Yes, control. As direct market actions through more and more QE began to lose their edge as early as 2010, the Fed found yet another toolbox “to support a lagging economy”. They found narrative. They found that their words (‘forward guidance’ in the lingo, or sometimes ‘communication policy’) could be used instrumentally, not as a reflection of authentic belief or (god forbid) uncertainty and humility, but as a conscious tool to drive market behaviors in a desired direction. And that desired direction, of course, in the absence of inflation in the real economy, is always up.

Ben Bernanke, in his final substantive speech as Fed chair, marveled at the efficacy of this new toolbox for modern monetary policy. Their first and historically primary toolbox – setting very short-term interest rates – had proved ineffective at stopping the financial system freefall of the Great Financial Crisis. Their second toolbox – balance sheet expansion and QE – had saved the world initially, but required more and more purchases for less and less impact. This third toolbox, however – communication policy and forward guidance – well, there seemed to be no limit to its ability to shape market and broader macroeconomic outcomes, provided that the Fed maintained its ‘credibility’ with these verbal promises today to maintain its “extraordinary accommodation” far into the future. And oh by the way, we were in good hands with Bernanke’s retirement from the Fed (as he headed off for a well-remunerated future with Ken Griffin and Citadel), because the person who had led the development of this new toolbox within the Fed was none other than the incoming Chair, Janet Yellen.

The Yellen Fed was peak Fed. Peak, not in the sense of maximum balance sheet expansion, but in the sense of maximum faith and maximum zealotry that the Fed’s three toolboxes – short-term interest rates, balance sheet operations and communication policy – could achieve any desired macroeconomic outcome in this, the best of all possible worlds. Business cycle? What business cycle? Welcome to the era of permanent recovery! As for financial crises … well, haha, it would perhaps be presumptuous to say that a financial crisis will never occur again, but with our current knowledge and tools for prudential monetary policy, certainly we can say that a financial crisis will not occur in our lifetimes. These were, in fact, Janet Yellen’s literal words.

Ben Bernanke and Janet Yellen were true-believers in the power of monetary policy to control markets and the economy in a way that – in my experience as a former professional academic – only former professional academics can be. They were true-believers in a way that, to read his memoir, Alan Greenspan was not. Greenspan thought he could sneak in some wealth creation on the coattails of Volcker’s inflation-crushing campaign, not that he could eliminate the business cycle and rule the world from the Mount Olympus of the Eccles Building. Now, to be sure, that doesn’t let Greenspan off the hook here. In fact, you can argue that Greenspan was the most culpable of the lot because he knew better!

I think that Jay Powell is a lot more like Greenspan than Bernanke and Yellen. I think he knows better. I think he knows that it is economically unsustainable, socially destructive and politically poisonous to inflate wealth so much more than an economy grows. I think that his efforts to raise interest rates and start shrinking the balance sheet, efforts he started making almost as soon as he was sworn in as Fed Chair, are a reflection of this.

I also think that Jay Powell, centimillionaire, has personally been an enormous beneficiary of the wealth-inflation policies that Alan Greenspan set in motion in the mid-1990s. I also think that Jay Powell, banker, would sooner betray his convictions than risk a tarnished reputation with his Wall Street tong as the man who ended the decades-long party. I also think that Jay Powell, politician, was on the verge of having his career summarily ended at that White House dinner with Trump on Christmas Eve, 2018. And for all of those reasons, that tiny little notch in household wealth in Q4 of 2018 – the bear market of 2018 that felt like the end of the world to so many – was reversed into stronger than ever wealth inflation and economic financialization.

And then came Covid.

And then came the economic response to Covid, which was not only a resumption of full-bore QE and balance sheet expansion (about $2 trillion worth), but also the largest stealing pulling forward of wealth for direct distribution to the already well-off of any government program in the history of man.

Again, I am 1,000% in favor of emergency government action to save an economy in general and to save jobs in particular. What our government did in reaction to the Covid recession and bear market was not that. The Paycheck Protection Program (PPP), for example, distributed about $800 billion directly to American businesses, ostensibly to cover the cost of maintaining workers on payrolls. In truth, only about one-quarter of that money supported jobs that would have otherwise been lost. More than 70% of the PPP distributions, more than half a trillion dollars, went to the richest 20% of American households. That’s separate from the $680 billion in Federal unemployment benefits and $800 billion in ‘economic impact payments’ (stimulus checks), both of which also saw substantial, although less than PPP, wealth payments flow directly to already well-off households that were in no danger of losing a job or, really, suffering any sort of economic hardship from the Covid pandemic.

For millions of Americans, particularly relatively wealthy Americans like lawyers and doctors and bankers and accountants and consultants and financial advisors, 2020 wasn’t a difficult year financially, it was their best year ever.

This is what drove the enormous post-pandemic acceleration of wealth growth over economic growth.

This is what created resurgent inflation and inflation expectations.

This is what broke the world.

How? Because the hundreds of billions of non-emergency dollars pulled forward from future Americans that went straight into the pockets of Americans who suffered zero economic damage from Covid on top of the hundreds of billions of non-emergency dollars pulled forward from future Americans that went straight into the pockets of relatively well-off Americans from the 2017 Tax Cuts and Jobs Act on top of the TRILLIONS of non-emergency dollars spent by the Fed to artificially lower the price of money and inflate financial assets and channel mal-investment and create the worst decade of productivity growth in the history of the United States and make us FEEL rich without BEING rich … yeah, THAT is what causes inflation.

The entire justification for Greenspan’s original sin was that a little bit of egregious wealth inflation wouldn’t spur inflation in the real economy. So long as inflation stayed tamped-down in the real economy, so long as it wasn’t persistent, so long as everyone knew that everyone knew that inflation wasn’t a problem … we could party on. We could survive the central-banking-as-religion academic zealots. We could survive the reputation-over-soul bankers. But once that common knowledge shifts, once everyone knows that everyone knows that inflation IS a problem, it all goes poof.

Low inflation – in both real world and narrative world – is the necessary and sufficient condition for these red arrows to be steeper than the green arrows.

High inflation – in either real world or narrative world – requires the red arrow to be less steep than the green arrow.

Greenspan’s magic trick – inflating wealth without sparking inflation in the real economy – is dead. It doesn’t work anymore. There’s no more room for monetary policy to create “free” wealth, for these growth lines to separate further. There’s only room for these lines to converge, and the only realistic way for that to happen is for the wealth growth line to go down. A lot. Remember, a bear market is only a little notch in that line. A nationwide collapse in home prices, like in 2008-2009, is only a modest dip.

Roughly speaking, we need a wealth destruction event that’s equivalent to the 2008-2009 Great Financial Crisis just to get the ratio of wealth to GDP back to pre-pandemic levels.

If you sincerely want to eliminate inflationary pressure and expectations, that is.

If you don’t want to eliminate inflationary pressure and expectations, or rather, if the political consequences of the wealth destruction required to eliminate inflationary pressure and expectations are too unbearable, then you can instead simply mandate the effects of inflation away through wage/price controls and related policies (effective nationalization of large swaths of economic activity, for example). But those are your choices. Neither is attractive. At least with the former – wealth destruction to get at the heart of what creates inflation – you can recover and grow your way back to a more equitable and more vibrant society. The latter, though – wage/price controls and outright nationalization or pseudo-nationalization of entire economic sectors – man, you never recover from that.

Unfortunately, I think the political consequences of the wealth destruction now required to control inflation authentically ARE too unbearable for every status quo political institution, for both the Dems and the GOP. I think by far the most likely path forward is greater and greater political lashing-out into worse and worse policy positions, both economically and culturally.

Apocalypse Now.

Or at least now-ish.

So what happens to us villagers when Captain Willard kills Kurtz and calls in the air strikes?

You know, when I wrote that original Hollow Men note eight years ago, I thought I understood this quote from Conrad.

The question is not how to get cured, but how to live.

Joseph Conrad (1857 – 1924)

That’s a quote from Lord Jim, not Heart of Darkness, but whatever. It’s a wonderful quote, because there is no “cure” for the modern condition, whether it’s our modern condition or the modern condition of 1899. This is the world we’ve got. There is no other. The warped Kurtzian kingdom isn’t hidden away up-river in some jungle, it’s all around us. Right now. We are IN that warped Kurtzian kingdom, and there is no escape, no cure. There is only how we choose to carry ourselves as human beings through the conclusion of this Old Story. There is only how to live.

Eight years ago, I thought the answer to this question was just to play the game better.

On defense, recognize that modern markets are, in fact, quite hollow and everything you hear from a public voice is being said for effect. But that doesn’t mean that the underlying economic activity of actual human beings and actual companies is similarly fake or bogus. The trick, I think, is to recognize the modern market for what it IS – a collection of socially constructed symbols, exactly like the chips in a casino, that we wager within games that combine a little skill with a lot of chance. There is a relationship between the chips and the real-world economic activity, but that relationship is never perfect and often exists as only the slimmest of threads. The games themselves are driven by the stories we are told, and there are rules to this game-playing that you can learn. But it’s a hard game to play, and it’s even harder to find a great game-player who will bet your chips on your behalf. A better strategy for most, I think, is to adopt an attitude of what I call profound agnosticism, where we assume that ALL of the stories we hear (including the narratives of economic science) are equally suspect, and we make no pretense of predicting what stories will pop up tomorrow or how the market will shape itself around them. What we want is to have as much connection to that underlying economic activity of actual human beings and actual companies as possible, and as little connection as possible to the game-playing and story-telling, no matter how strongly we’ve been trained to believe in this story or that. I think what emerges from this attitude can be an extremely robust portfolio supported by more-than-skin-deep diversification … a portfolio that balances historical risks and rewards rather than stories of risk and reward, a portfolio that looks for diversification in the investment DNA of a security or strategy as well as the asset class of a security or strategy.

On offense, look for investment opportunities where you have information that reflects an economic reality at odds with the public voices driving a market phenomenon. This is where you will find alpha. This is where you can generate potential returns when the economic reality is ultimately revealed as just that – reality – and the voices shift into some other story and the market matches what’s real. These opportunities tend to be discrete and occasional trades as opposed to long-standing strategies, because that’s the nature of the information beast – you will rarely capture it in a time and place where you can act on it. Almost by definition, if the information is being generated by a public voice it’s probably not actionable, or at the very least the asymmetric risk/reward will have been terribly muted. But when you find an opportunity like this, when you have a private insight or access to someone who does against a market backdrop of some price extreme … well, that’s a beautiful thing. Rare, but worth waiting for.

Hollow Men, Hollow Markets, Hollow World (March 30, 2014)

It’s still really good advice for a game-player! Meaning, if your day job or your position in life requires you to take an active interest in markets, like if it matters to you or if you find it interesting how the market reacted to the CPI report this morning, much less if you know that the CPI report comes out every mid-month on a Weds at 8:30am ET, then I think this is really good advice on how to live. And in my professional life, I’ve spent the past eight years building a business with my partner, Rusty Guinn, to put exactly this advice into practice.

But today, as opposed to eight years ago, I am thinking about a lot more than just the narrow confines of the market games I play in my day job.

I am thinking about what happens to the games of markets and politics if we have wealth destruction along the lines of what I suspect will be necessary to wring out inflation from our insanely financialized world.

I am thinking about what happens to the games of markets and politics if we DO NOT have wealth destruction along the lines of what I suspect will be necessary to wring out inflation from our insanely financialized world, but instead choose to order inflation away through the fiat commands of price controls and economic dirigisme.

How do we live when we know full well how this story ends?

Because we all know exactly how this Old Story ends, right? We know that when prideful human leaders lift themselves and their people up to unnatural heights by stealing what is not rightfully theirs, their society is struck down in retribution. We’ve seen this movie a thousand times before.

I don’t have an Answer with a capital A to Conrad’s question of how to live, and if I said I did you shouldn’t believe me. All I know is a Process. All I know is this: We may work in a hollow market and we may live in a hollow world. Kurtz’s time may be up. But let us refuse to be Hollow Men.

Mistah Kurtz – he dead

A penny for the Old GuyI

We are the hollow men

T.S. Eliot, The Hollow Men (1925)

We are the stuffed men

Leaning together

Headpiece filled with straw. Alas!

Our dried voices, when

We whisper together

Are quiet and meaningless

As wind in dry grass

Or rats’ feet over broken glass

In our dry cellar

Nope. Hard pass. This is NOT how we live. Instead, how about we live as autonomous human beings possessed of a soul and a conscience? We find our pack – online and offline, networked and meatworked – other autonomous human beings who treat us as ends in ourselves, never as a means, and demand the same human treatment in return.

And then we tell ourselves a new story.

More By This Author:

They’re Not Sending Their BestWhat is Robinhood?

I’m So Tired Of The Transitory Inflation “Debate”

Comments

Log in or sign up to join the conversation.