Image Source: Pexels

UK stocks saw an initial rebound on Wednesday following losses in the prior session, as investors eyed potential relief from U.S. tariffs. The FTSE 100 rose by 0.5% early in the day but later slipped into negative territory. Previously, the blue-chip index had retreated from record highs due to new tariffs imposed by U.S. President Donald Trump on key trading partners. Optimism was sparked by comments from the U.S. Commerce Secretary suggesting possible tariff exemptions for Mexico and Canada, which fueled hopes for continued negotiations. Additionally, market sentiment improved after President Trump indicated that Ukraine was ready to negotiate a resolution to its conflict with Russia, following last week's tense exchange with President Volodymyr Zelenskiy. Among sectors, precious metal miners led the gains with a 3.6% surge, marking the strongest performance. Financial stocks also provided support, with the banking sector rising 2.2% after a steep decline of over 3% on Tuesday. UK bond yields climbed, reflecting a selloff in longer-term German bonds, as parties negotiating a new German government agreed to revise borrowing rules and boost government spending, particularly in defense. This development lifted the UK defense sector, which advanced by 2.5%. Other economically sensitive sectors also performed well, with construction, materials, and travel and leisure each posting gains of over 2%. On the economic data front, the UK S&P Services Purchasing Managers' Index dipped slightly to 51 in February from 51.1 in January. The survey highlighted that service firms were cutting their workforce at the fastest pace since 2020, as they braced for next month's tax and minimum wage increases.

Single Stock Stories & Broker Updates:

-

Shares of Breedon Group rise 14% to 486.5p, the highest since January 2022, after acquiring U.S. construction materials company Lionmark for $238 million. The company anticipates 6% growth in 2024 EBITDA and revenue due to entry into U.S. markets and cost controls. Analysts at Peel Hunt expect steady progress despite challenging conditions in Great Britain. The stock has increased 9.26% year-to-date.

-

Shares of Balfour Beatty fell 5.8% to 429.2 pence, their lowest since Jan. 15. Leo Quinn will resign as CEO after 10 years, succeeded by Philip Hoare from AtkinsRéalis. BALF stock rose ~37.3% in 2024.

-

Shares of Capita rose 7.14% to 14p. The company reported a 2024 adjusted operating profit of £95.9 million, a 5.5% increase from 2023, due to a cost-reduction program. Adjusted revenue is expected to be steady in 2024, with a slight rise in operating margin, despite some impacts from existing Life & Pensions contracts. The group aims to be free cash flow positive by the end of 2025. Capita's stock has fallen approximately 36% in 2024.

-

Quilter's shares rise 6.8% to 162p; FTSE mid-cap index up 0.84%. The British wealth manager reports a 17% y/y increase in adjusted profit before tax and raises FY dividend by 13% to 5.9p. Forecasts a cost base of ~500 mln pounds in 2025, predicting mid to high single-digit rise in adjusted profit. Total AUMA at 119.4 bln pounds, up from 106.7 bln pounds a year ago. QLT gained ~50% in 2024.

-

Shares of Games Workshop rise 8.8% to a record 14,970 pence; the company anticipates 2025 PBT to exceed expectations due to strong core performance and licensing. Peel Hunt cites strong momentum and maintains a "buy" rating, raising the target price from 14,400 to 15,000 pence. Stock up ~57.50% in the last year.

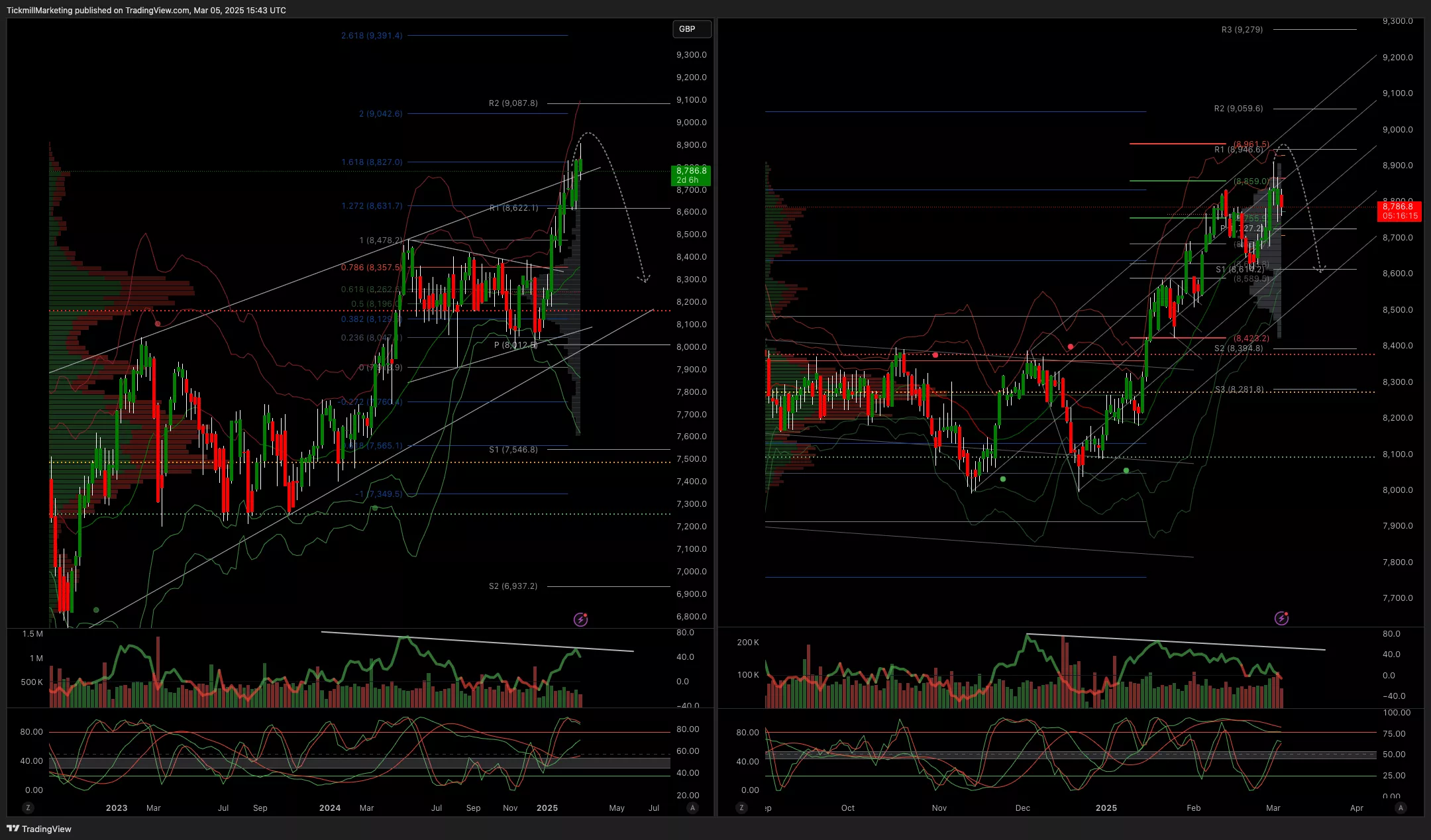

Technical & Trade View

FTSE Bias: Bullish Above, Bearish below 8950

- Primary support 8700

- Below 8700 opens 8600

- Primary objective 9050

- Daily VWAP Bearish

- Weekly VWAP Bullish

(Click on image to enlarge)

More By This Author:

Daily Market Outlook - Wednesday, March 5

The FTSE Finish Line - Tuesday, March 4

Daily Market Outlook: Tuesday, March 4

Comments

Log in or sign up to join the conversation.