Image Source: Pexels

While many commentators will focus on a host of changes to the Federal tax system, the more important topic concerns the budget’s impact on the Federal debt going forward. With inflation and interest rates uppermost in the mind of Canadians, the Federal budget analysis offers an excellent opportunity to examine how spending and taxation decisions impact our public finances.

To begin with, the government has essentially used more than all of fiscal space available to it. In order to keep the overall deficit from expanding significantly, it was necessary to add tax increases on selective individual categories and on capital gains, the only areas that offered some tax room.

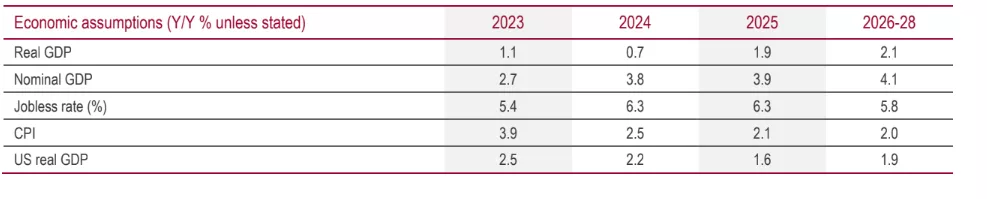

The Canadian economy is expected to grow at rather anemic pace. Private forecasters expect real GDP to grow at a mere 0.7% in 2024 and a touch better in 2025. Nominal GDP, which governs revenues and spending, is anticipated to be restricted to around 4% yearly in the next two years. The figures look even worse when we consider that population growth is running at 2%, resulting in a decline in the real GDP per capita. Economic growth conditions limit the amount of fiscal room available to Ottawa, something that is implicitly acknowledged in the budget documents.

(Click on image to enlarge)

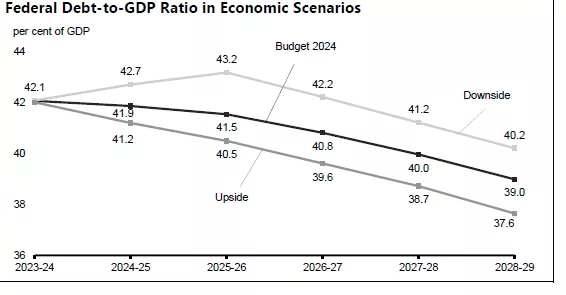

Given this dismal growth outlook, the next measure to consider is the Federal deficit in relation to GDP, that is, just how impactful will the shortfall in revenues be in relation to the growth of the economy. Depending on the expected rate of growth, the Federal debt-to GDP will range from 40.5% to 43.2%, and will likely decline from there out to 2028. By international standards, this is a relatively low ratio. The US debt-to-GDP is 120% in 2024 and is expected to worsen considerably in 2025. When adding on provincial debt, Canada continues to have a favourable standing regarding overall government debt.

Source: Finance Canada

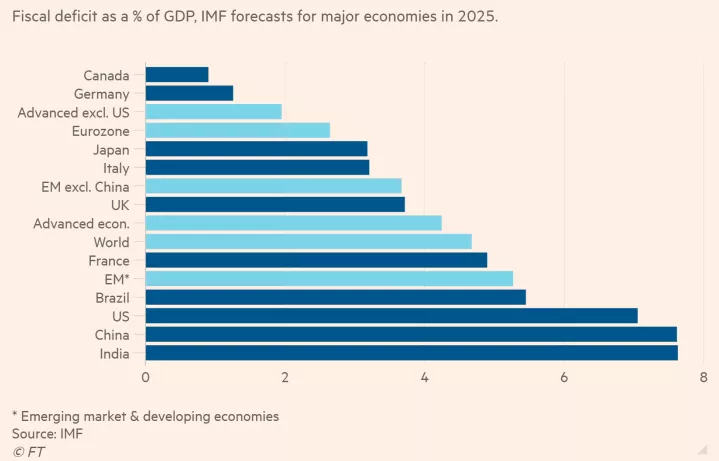

Another way to look at the debt situation is by considering the annual deficit as a percentage of GDP. Here Canada is the envy of the world with an estimate is 1.3%. Forecasts for other major economies, range from the Eurozone, 2.5%, to the US, 7.7%.The deteriorating situation in the US is now getting more attention, given the huge surge in new issuances coming this year.

(Click on image to enlarge)

Consequently, participants in the Canadian debt market do not anticipate any change in Canada’s AAA-rating. Additional supply will not affect yields. The Federal government will continue to access the debt market at relatively low-interest rates, even in the long end of the yield curve. Again, the Canadian experience is in sharp contrast to the US where relatively much heavier borrowing requirements will likely result in a much more steeper yield curve in the long end.

More By This Author:

Suppose We Never Get Back To 2% Inflation Rate

Canada Is Now Experiencing A Hard Landing

The Great Canadian Debate Is Underway Why Productivity Is So Poor

Comments

Log in or sign up to join the conversation.