Image Source: Pexels

Recovery in the Polish industry is progressing, with the outlook of stronger domestic demand and signs of recovery from the German industry laying the groundwork for further improvement.

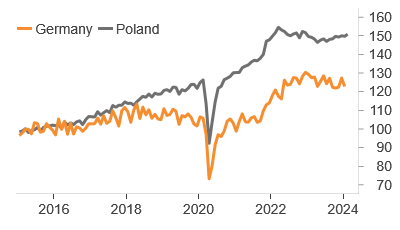

The Polish industry is recovering from stagnation. In February, industrial production expanded by 3.3% year-on-year, above the consensus of 2.4%. The figures for January were also revised upward from +1.6 to +2.9% YoY. The structure of production indicates that the recovery is wide ranging, mainly from global tradable sectors through defense orders (Ukrainian equipment repairs) and, to a lesser extent, from domestic consumer goods.

The growth in production was primarily driven by investment-related repair maintenance and installation of machinery and equipment category (48.5% YoY) and other transport equipment (17.8%, in all likelihood railway-related). We have also seen a recovery in industries related to natural gas (chiefly chemical production). Declines were primarily led by mining and utilities, given lower global energy commodities prices and atypically warm weather in February.

Outlook for 2024

There are grounds for recovery in both our trading partners and Poland. In Germany, we see a recovery in energy-intensive sectors, which were very weak for most of 2023. We can also see a recovery in transport. These sectors typically lead the recovery in other industries.

In Poland, the main growth driver in 2024 should be the strong pace of real wages, which are currently the highest seen since December 1999 – and this should finally translate into consumer spending. The Polish corporate sector (along with the rest of the economy) seems very deleveraged and should finally catch up with investment after years of very poor outlays. The third driver should be EU money, with Poland having two and a half years to spend the Recovery and Resilience Facility (7-9% of GDP). Other EU member states have had six years for this.

Today's data shows that Poland's recovery is progressing, and we expect this trend to continue in the coming months. Consumption will be the main driver of the country's growth in 2024, but today's production data also shows a recovery in exporting sectors.

Industrial production in Poland and Germany (2015 = 100)

Image Source: CSO data.

More By This Author:

UK Inflation Set To Fall Below 2% By May After Latest DataWhat A Shift In Fed Dots Would Mean For G10 FX

Italian Industrial Production Sees A Soft Start To 2024

Comments

Log in or sign up to join the conversation.