Market rates are pointing higher as central banks are under pressure to do more. This is exemplified by the latest upside surprise in the US CPI and, in the eurozone, by the ECB pushing the topic of quantitative tightening on all channels. In the UK it is fiscal policy putting pressure on the BoE, and that stand-off continues to be a major source of volatility.

CPI data sends a clear signal that the Fed needs to do more

The US CPI report came in higher than expected, with the core rate marking a new peak of 6.6% and surpassing the level seen at which the Fed began hiking interest rates in March. The data is a clear signal that the Fed has more to do. In the wake of the Federal Open Market Committee minutes which showed that the Fed sees the cost of doing too little on inflation outweighing those of doing too much, the market has started to attribute a small chance to an even larger 100bp hike in November, and 75bp now looks like the bare minimum. Looking into December markets now see a 50% chance of a further 75bp. Mind you, our economists still think it is more likely that the Fed will slow its pace then.

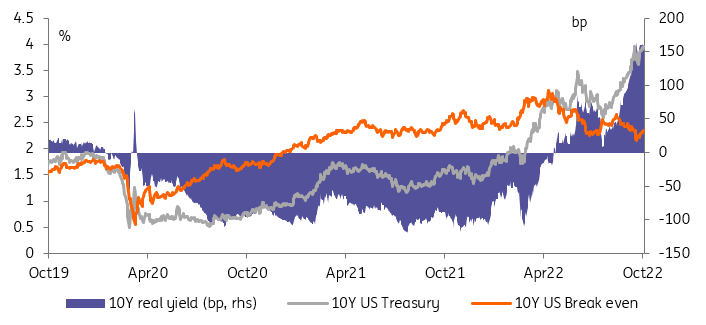

Looking beyond the pricing of immediate Fed policy, the CPI report briefly pushed the 10Y Treasury yield above 4% again, the third time within the past two weeks. Eventually, a break above 4% for the 10Y now looks inevitable as the Fed is unlikely to signal any inclination to slow its pace near term.

Bearish risk: 10Y Treasuries should rise above 4% and real yields push even higher

Image Source: Refinitiv, ING

Gilt markets remain a source of extreme volatility

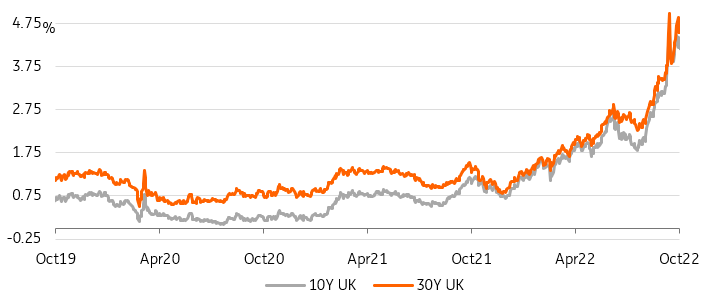

The US CPI report saw 10Y US Treasuries spike with an intraday move of almost 24bp. But that move still pales next to the more than 40bp intraday swing in 10Y gilt yields over the course of yesterday’s session. Speculation suggesting a potential U-turn of the government regarding its fiscal plans had been the main driver, leaving 10Y gilts to end the day some 25bp lower at close to 4.2%. The ill-fated long end of the curve saw 30Y gilt yields ending almost 30bp lower.

The BoE is still planning to end its gilt market intervention after today

While it may seem that the Bank of England could win this stand-off, it does not mean it is the end to the volatility in the market just yet. For now, the reports of a potential U-turn are just speculation and officially the government is still sticking to its plans, according to later statements. With the BoE still planning to end its gilt market intervention after today and the government's medium-term fiscal strategy at the end of October, markets could be left on tenterhooks for longer.

Not out of the woods yet: gilts need BoE support and fiscal U-turn confirmation

Image Source: Refinitiv, ING

The October ECB meeting is shaping up to become a busy one

The wild gyrations in gilt markets have managed to pull 10Y and longer EUR rates lower, but the front-end rates have pushed higher with the European Central Bank showing resolve in pursuing more policy tightening. Hawks like Belgium’s Wunsch not excluding key rates even above 3% keep up pressure on the front-end pricing of hikes as inflation data continues to surprise to the upside. For October the market is already discounting a more than 80% chance of a 75bp hike.

Euro front-end rates have pushed higher with the ECB showing resolve in pursuing more policy tightening

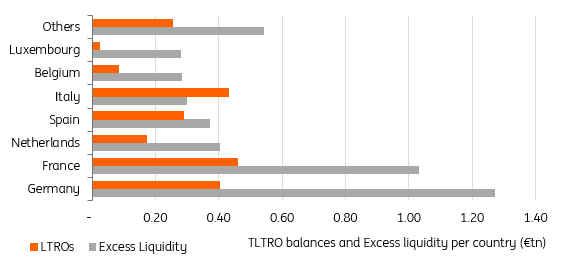

But it is the more concrete plans to whittle down the balance sheet that continue to grab the headlines. Reuters had already earlier reported that staff was working on three options to make it less profitable for banks to hold on to their targeted longer-term refinancing operations funds, one of them a likely tiering of bank reserves. A decision in that regard could already be taken at this month's policy-setting meeting. But that would only be the first step as we have learned over the past few days. Also according to Reuters reporting, the ECB could already be laying the groundwork for the next step, which is quantitative tightening, by changing the wording of the reinvestment guidance already this month as well. This would then leave a decision to actually kick off quantitative tightening for the December or February meetings. The hawks on the ECB council are obviously the ones targeting an early 2023 start to letting the bond portfolios roll off Bloomberg reported.

Tiering risk: TLTRO balances and excess liquidity are unevenly distributed in the eurozone

Image Source: ECB, ING

Today’s events and market view

Clearly, the data and monetary policy backdrop suggest persistent upward pressure on rates. However, developments in the gilt market remain a wild card. Even more so as today will see the BoE's last buying operation in support of long-end gilts – unless it were to decide on an extension of the operations the gilt market would be even more exposed to headlines surrounding the government's rethink of its fiscal plans.

In data, the focus remains on the US today. Retail sales for September should have received a lift as auto sales rebounded and gasoline should be less of a drag given a recent stabilization in prices. More closely watched will probably be the University of Michigan consumer confidence survey and in particular the gauges of consumer price expectations. Consensus sees the 1Y inflation expectations receding, but perhaps more worryingly it sees the 5-10Y expected inflation measure inching up a tad to 2.8% from 2.7%.

More By This Author:

India: Inflation Creeps HigherWASDE Update: U.S. Supply Cuts

FX Daily: Fed’s Hawkish Risk Management To Keep The Dollar Bid

Comments

Log in or sign up to join the conversation.