WASDE Update: U.S. Supply Cuts

Yesterday's WASDE report was largely constructive. For the US market, corn and wheat saw lower 2022/23 ending stocks. However, the market was expecting even more aggressive reductions. As for soybeans, unchanged US ending stocks proved supportive for prices.

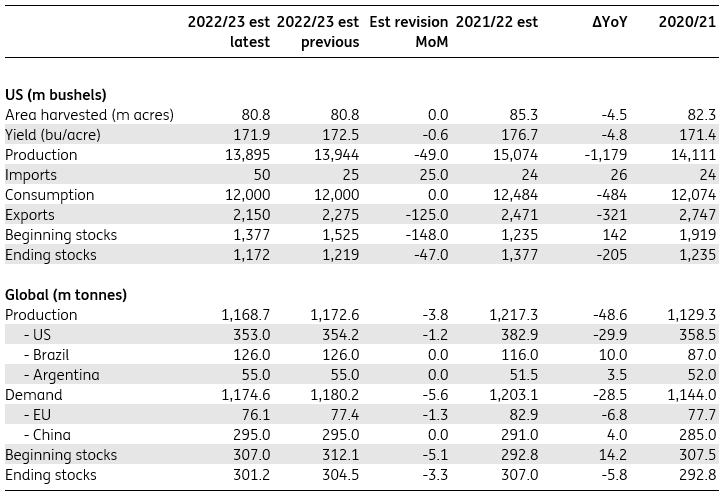

US corn yields revised lower

The USDA revised lower its estimate for US corn stocks at the end of 2022/23 to 1.17b bushels compared to an earlier estimate of 1.22b bushels. However, this still left stocks above the roughly 1.13b bushels the market was expecting. The move was largely due to lower beginning stocks which were lowered by around 0.15b bushels. The agency also lowered domestic corn production estimates for this season from 13.94b bushels to 13.89b bushels on account of lower yields. Export estimates were also revised down by 126m bushels to 2.15b bushels.

For the global market, the USDA reduced its estimate for global ending stocks from 304.5mt to 301.2mt; again, largely on account of smaller stocks at the start of the season. Global beginning stocks were revised down by around 5.1mt due to lower stocks in the US and Ukraine. The revised numbers are largely in line with market expectations of around 301.9mt. Global corn output was lowered by 3.8mt to 1,168.7mt due to lower supply from the US (-1.2mt) and the EU (-2.6mt). Meanwhile, global demand estimates fell from 1,180.2mt to 1,174.6mt.

While the numbers, particularly for the US were not as bullish as the market was expecting, both the US and the global market continue to tighten, which should provide support to prices.

Corn supply/demand balance

Source: USDA

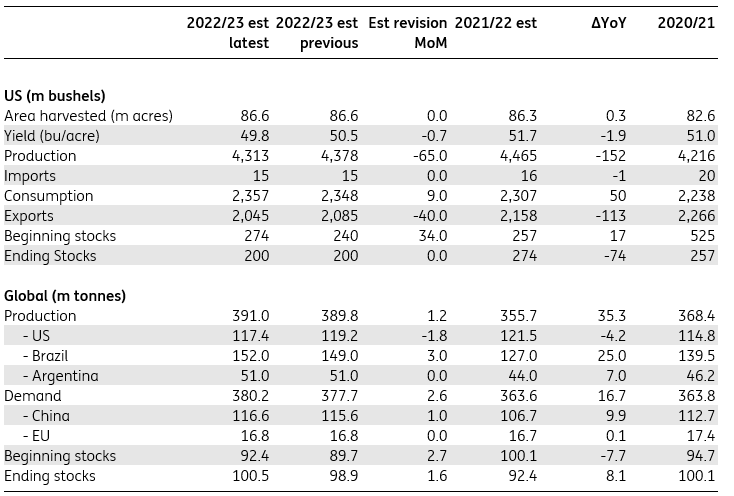

US soybean output cut

The USDA revised lower production estimates for US soybeans by 69m bushels to 4.3b bushels. This was due to a reduction in yield expectations, which were revised down from 50.5 bu/acre to 49.8 bu/acre. Both yields and production came in below market expectations and this has provided a boost to soybean prices. Meanwhile, the agency estimates that lower output and increased competition from South America could impact exports, which were cut from 2.09b bushels to 2.05b bushels. US ending stocks for 2022/23 were left unchanged at 200m bushels; however, this was below the roughly 245m bushels the market was expecting.

For the global market, 2022/23 ending stocks were increased from 98.9mt to 100.5mt, largely on account of higher supplies from Brazil. This number was also slightly higher than the 99.7mt the market was expecting. Global soybean production estimates increased by around 1.2mt to 391mt, which was driven by a 3mt increase in Brazilian supply. Global demand numbers were also increased by around 2.5mt to 380.2mt for 2022/23.

Soybeans supply/demand balance

Source: USDA

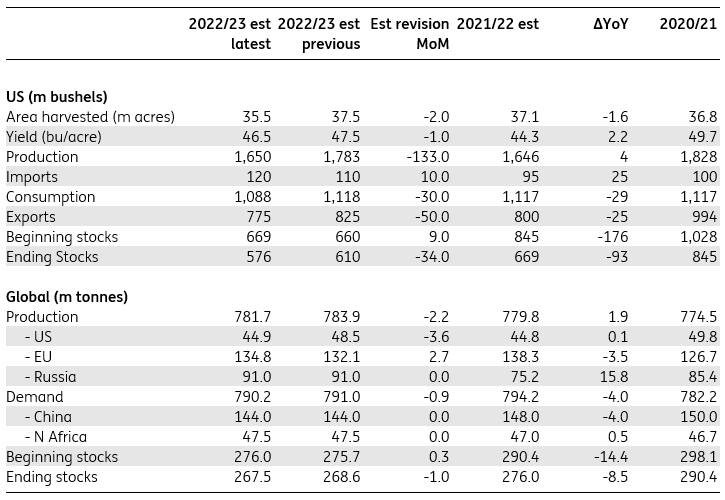

Wheat balance sheet tightens

The USDA lowered US wheat ending stock estimates for 2022/23 from 610m bushels to 576m bushels (lowest since 2007/08); although it was still higher than the roughly 563m bushels expected. The agency lowered production estimates from 1.78b bushels to 1.65b bushels due to falling acreage and yields.

The global wheat balance saw few changes in aggregate with 2022/23 ending stock estimates revised down slightly from 268.6mt to 267.5mt, which was in line with market expectations. 2022/23 output was cut from 783.9mt to 781.7mt with key reductions coming from the US (-3.6mt) and Argentina (-1.5mt).

Wheat supply/demand balance

Source: USDA

More By This Author:

FX Daily: Fed’s Hawkish Risk Management To Keep The Dollar Bid

The Commodities Feed: OPEC Lowers Demand Expectations

Surprise Jump In Eurozone Industrial Production In August

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more