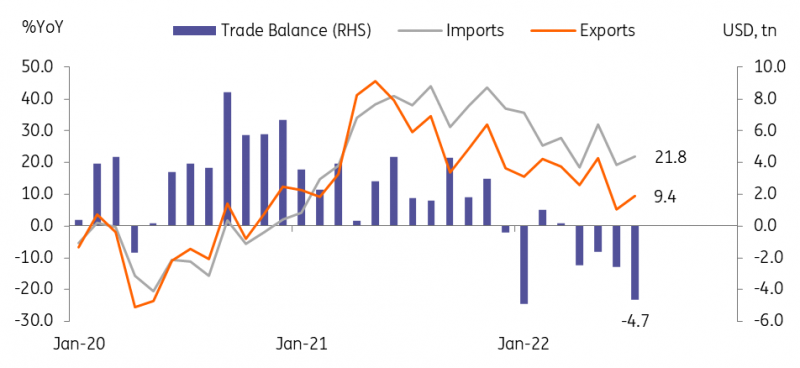

Exports in July showed a solid gain on the back of solid demand for IT and automobiles, but the trade deficit widened as imports surged due to a rise in commodity prices. Still, the weak business survey suggests a cloudy outlook for exports in the near term.

Exports rose 9.4% YoY in July (vs 5.2% in June)

As last month’s idiosyncratic factors dissipated, exports grew firmly in July but slightly fell short of the market consensus of 10.0%.

By exports item, petroleum exports (86.5%) led the growth mainly due to favorable price effects, while motor vehicles (25.3%) and semiconductors (2.1%) also showed a solid gain. The prolonged supply bottleneck in the auto industry seems to be slowly improving and global IT demand appears to remain strong.

By export destination, exports to the US (14.6%) and ASEAN (20.9%) were particularly strong while exports to China (-2.5%), the Commonwealth of Independent States (CIS), and Latin America (LATAM) were weak. Although China’s lockdown measures eased since June, growth momentum has weakened, which is a major downside risk to Korea’s exports in the second half of the year.

Meanwhile, imports (21.8%) exceeded exports again in July, thus the trade deficit widened to -USD4.6bn in July (vs -USD2.5bn in June).

Trade deficit widened in July due to high commodity prices

Source: CEIC

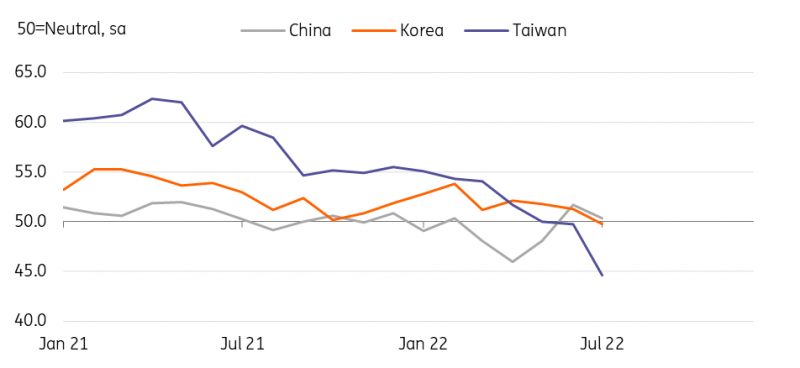

PMI fell to 49.8 in July

The manufacturing PMI fell below 50 for the first time since September 2020, at 49.8 in July (vs 51.3 in June), as the weak local business surveys suggested last week. Along with the sharp declines in China and Taiwan PMIs, the outlook for Korea’s exports is also cloudy. However, while we do not expect exports to contract suddenly in the coming months, benefiting from a diversified export portfolio, the trade deficit will continue for the time being as global commodity inflation remains high.

PMI fell below 50

Source: CEIC

More By This Author:

Key Events In Developed Markets For Week Of August 1

Key Events In EMEA For Week Of August 1

Japan: Monthly Activity Data Suggests GDP Will Rebound In The Second Quarter

Comments

Log in or sign up to join the conversation.