Image Source: Pexels

With policymakers hinting back in June that they could force inflation lower, we are anticipating a 50bp hike from the Bank of England next week. In the US, next Friday's jobs and business survey reports are set to confirm the economy is slowing.

US: Business survey results and jobs reports are set to confirm the economy is slowing quite quickly

Between now and the 21 September FOMC meeting, there are two US job reports, two inflation prints, and the Jackson Hole annual symposium. Consequently, it isn’t surprising that the Fed chose to be vague in its forward guidance after hiking rates by 75bp on Wednesday. The Federal Reserve has made it clear it is prepared to sacrifice growth as it looks to beat inflation down toward its target, but now that the US is in a technical recession and is seemingly headed toward what might be termed a “real” recession with rising unemployment and falling consumer spending, we expect the Fed to pivot to 50bp hikes in September and November.

This view should get some support from next Friday’s jobs report. There are still two vacancies for every one unemployed American, and small businesses are crying out for staff, so we suspect that it will be a lack of supply that holds back the figure with payrolls set to increase by 220,000. With unemployment remaining at just 3.6%, wages still growing at around 5% year-on-year, and inflation just shy of 10%, the Fed will continue hiking for now. However, business surveys such as next week’s ISM reports are set to confirm that the economy is slowing quite quickly and the Fed will tighten policy more modestly in the coming months.

UK: Bank of England to deliver a 50bp rate hike

We expect a 50bp rate hike from the Bank of England next week, its first such move this cycle. That’s not because the data we’ve received since June’s 25bp hike decision has moved the needle all that much – it hasn’t. But policymakers hinted back in June that they could act ‘forcefully’ to get inflation lower. And with a 50bp move more-or-less priced in, that’s what we expect them to do.

However, we think the Bank’s window for further rate hikes is gradually closing. There are likely to be hints of this in the Bank’s new forecasts, which we expect to again show inflation would be below target in 2024/25 if policymakers follow through with the number of rate hikes markets have been pricing. But aside from that, the Bank may be reluctant to signal a forthcoming pivot in policy – not least because of the hawks’ concerns about recent sterling weakness.

Canada: Expect a shift toward more modest incremental hikes

In Canada, a decent jobs report will suggest that the Bank of Canada still has more work to do given inflation is at 40-year highs. Like the Fed, we expect the Bank of Canada to pivot toward more modest incremental hikes in coming meetings after the surprise 100bp jump at the last meeting. We expect a 50bp hike on 7 September.

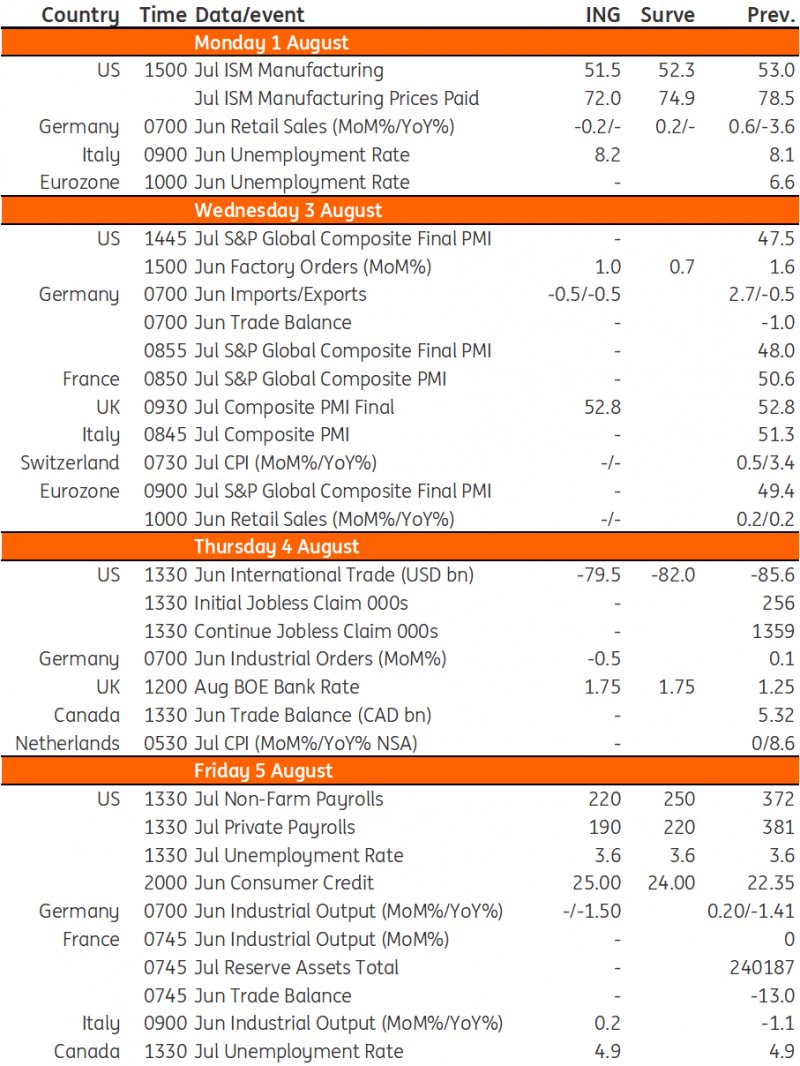

Developed Markets Economic Calendar

Image Source: Refinitiv, ING

More By This Author:

FX Daily: Data Sensitivity To Keep FX Volatility High

Asia Week Ahead: Central Bank Decisions, Inflation And Manufacturing Reports

FX Daily: The Dollar’s “Pivot” Hasn’t Arrived Yet

Comments

Log in or sign up to join the conversation.