Image Source: Pixabay

We expect the Central bank of Turkey to keep rates on hold next week, given the current global economic backdrop. However, we recognize there is a significant risk skewed toward more easing as the central bank focuses on preserving growth momentum in industrial production.

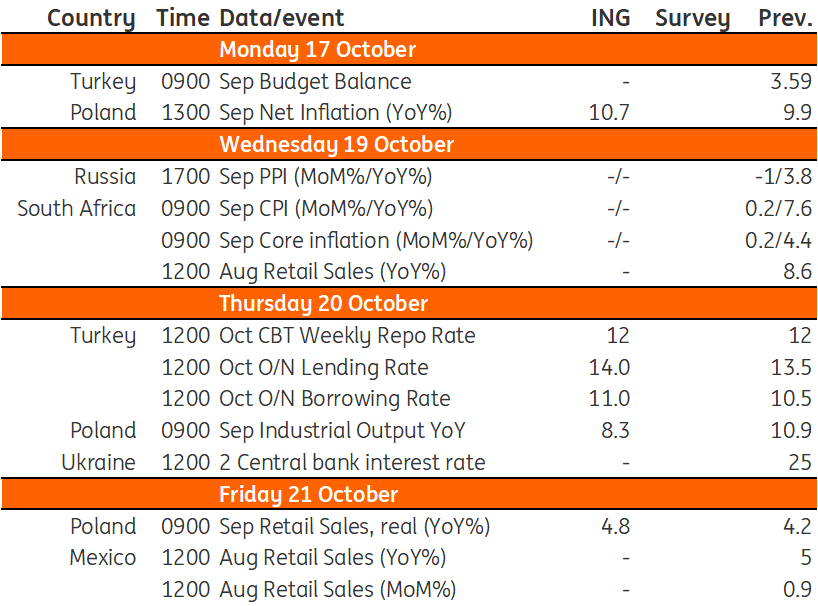

Turkey: Central bank of Turkey is expected to remain mute this month

The Central Bank of Turkey's (CBT’s) recent rate cuts against a backdrop of high external finance requirements and a global risk-off mode can weigh on reserves as we have already seen a decline in the second half of September. Given this backdrop, the bank can remain mute this month. However, there is a significant risk skewed towards more easing given 1) president Recep Tayyip Erdogan’s call for further rate cuts to single digits by the end of the year, and 2) the CBT’s focus on supportive financial conditions in order to preserve the growth momentum in industrial production, and due to the positive trend in employment given recent signals of decelerating economic activity.

Poland: annual growth in industrial output moderated to single-digit levels

Industrial output (forecast: 8.3% YoY):

Seasonally-adjusted data indicate that output started expanding again in 3Q22, after declining in 2Q22. Hard data do not confirm the sharp deterioration in industrial conditions painted by the nose-diving manufacturing PMI. Still, we expect that annual growth moderated to single-digit levels in September. High prices and the potential shortage of energy will weigh negatively on industrial performance in 4Q22.

Retail sales, real (forecast: 4.8% YoY):

Although the inflow of refugees from Ukraine is positive for the consumption of goods, the impact of this factor seems to be waning as high inflation bites into real income and makes consumers more cautious about spending. In September, we expect sales to have expanded by some 4.8% year-on-year, i.e. at a similar pace as in August (4.2% YoY). The structure of sales is projected to remain similar, with poor sales of durable goods and solid sales of necessities (food, clothing). In 3Q22, sales were visibly weaker than in 2Q22 in annual terms, pointing to easing household consumption.

Key events in EMEA next week

Image Source: Refinitiv, ING

More By This Author:

Rates Spark: Keeping Up The Hawkish Pressure

India: Inflation Creeps Higher

WASDE Update: U.S. Supply Cuts

Comments

Log in or sign up to join the conversation.