<< Read Part 1: Just How Vulnerable is the Canadian Housing Market

Until very recently, we have come to accept that there is a very a close link between economic growth and the growth in net assets or net worth in the advanced economies. That tight correlation is no longer holding, according to a new report by the McKinsey Globe Institute( Rise of Global Balance Sheets). The study measures the balance sheets of 10 advanced economies and concludes that:

“Across ten countries that account for about 60 percent of global GDP—Australia, Canada, China, France, Germany, Japan, Mexico, Sweden, the United Kingdom, and the United States—the historic link between the growth of net worth and the growth of GDP no longer holds.....Savings have found their way instead into real estate, which in 2020 accounted for two-thirds of net worth”.

Since the beginning of this century, economic growth has been far from stellar as each recovery from a recession has been disappointing, yet our collective net worth has increase unabated, most of which is tied to land values. North Americans have experienced a tripling of home prices over the past decade, while national income growth barely exceeded an increase of 50% in nominal terms over the same period. Now, there is clear evidence that economic growth and wealth are fully decoupled. The authors of the McKinsey report point out that the value of residential real estate, including land, amounts to 46% of global net worth in 2020.

If net worth is rising because of house and land values, then what does this mean for financial stability? The Canadian experience is an excellent case study on this question. First, a word about measurement issues. Debt-to-GDP ratios are often used to probe the question of market sustainability. However, this ratio is ill-suited, since no one is expected to pay off all long-term debt with just one year’s income. A much more useful measure is to examine loan-to-value as a way to assess to what extent the surge in home prices threatens financial stability.

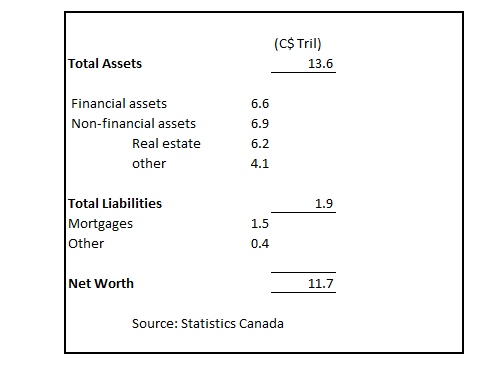

Household Assets and Liabilities, Canada, 2019

The pandemic has a significant impact on household credit, mortgage, and consumer loans, in Canada. The latest figures on household wealth are for 2019 and the data shows that Canadians have a relatively large cushion to withstand any drop in real estate values. Specifically, the ratio of loan-to-value was a very conservative 25% in 2019. The pandemic set off a flurry of housing purchases, driving up realty prices by as much as 20% in 2021. However, Canadian banks remained relatively conservative in issuing new mortgage money as their mortgage portfolio did not grow anywhere near the increase in residential real estate values ( mortgage lending).The net effect is that the loan-to-value estimates for 2021 would most likely have declined, further minimizing the risks and vulnerabilities to the Canadian financial system.

Comments

Log in or sign up to join the conversation.