Almost daily, Canadians read about soaring housing prices as buyers bid up residential real estate, while housing experts continuously warn about the prospects for a major correction in the market. David Rosenberg argues strenuously that “Canada {is} the second frothiest housing market in the world” (Overvalued). Toronto’s housing market just recorded a 19% increase in prices over the past 12 months. By comparison, Canadian housing prices have risen on average 8% annually.

To what extend housing is overvalued in Canada is a sterile debate. For one thing, the use of such ratios as house price-to-income or household debt-to-GDP come up short as reliable measures of housing affordability. Economists do not have the criteria with which to demonstrate that the housing market is “overvalued”. A far more useful way to look at the housing market is to understand the role that the credit markets play in supporting housing demand.

Specifically, how is housing financed and how sensitive is housing demand to changes in interest rates.

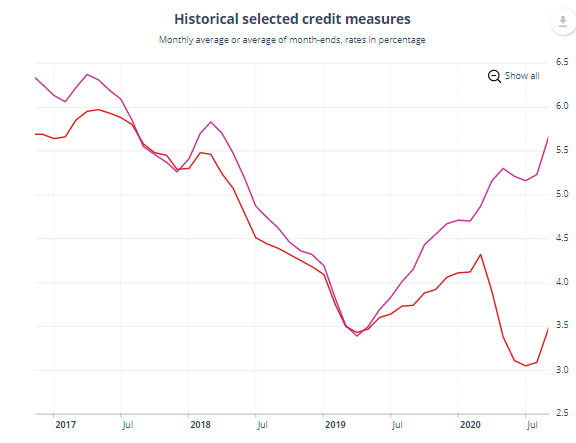

The pandemic has a significant impact on household credit, mortgage, and consumer loans, in Canada. Prior to 2020, household credit was growing at around 6.5% annually. Canadian banks remain relatively conservative regarding lending during the pandemic. Mortgage lending is currently running at 5.5% annually---- well below the nominal growth in housing prices. The other side of this coin is that home buyers are able to provide a considerable amount of equity, from savings. First-time buyers, for example, have taken advantage of parentisl gifts, especially for down payments. A recent CIBC report noted that “ given the trend and the size of gifting, it is clear that this phenomenon is becoming an important factor impacting housing demand and therefore home prices in Canada ( Gifting down payments).

Canadian Household Credit Growth

The Bank of Canada has hinted that it will be raising its bank rate in the near future--- perhaps as early as mid-2022. Consequently, there is growing concern about the impact of higher rates on real estate prices. A recent study by the CIBC considered the sensitivity of mortgage debt to higher interest rates (Ready for higher interest rates). Clearly, new buyers will face higher interest payments, resulting in a marginal reduction in demand for new and existing housing units. However, existing borrowers, the majority of whom took out 5- year fixed rate mortgages in 2017 through 2019, will not be fully impacted by any rate hikes. In sum, housing demand is not fuelled by credit expansion. Financial institutions have been very careful lenders. Buyers are able to provide considerable amounts of home equity. Moreover, should interest rates increase steadily in the next two years, existing borrowers will be immunized until, at least, 2024.

Comments

Log in or sign up to join the conversation.