Press reports suggest that the European Central Bank is about to change the remuneration of liquidity as soon as October. We review the options on the table and see how they will affect money market spreads, collateral scarcity, and swap spreads.

What’s on the table: TLTRO changes or tiering

Persistent press reports suggest a change in ECB liquidity policy as soon as the 27 October meeting. As rates rise, so will the amount of interest paid to banks on the €4.7tn of excess liquidity in the system. The central bank has a number of options at its disposal to reduce what is perceived as a subsidy to banks, stemming in part from around €2tn of cheap targeted longer-term refinancing operations (TLTRO) loans. It will also reduce the risk of central bank losses and thus of operating at with negative equity as our economics team has noted.

Three options are reportedly being discussed:

- Remunerate each bank’s TLTRO balance at 0%

- Treat each bank’s TLTRO balance as a required reserve and change the remuneration of required reserves, presumably 0%

- Introduce tiered remuneration of Excess Liquidity (EL, excess reserves and deposit facility balances): some at the deposit rate, some at 0%

Option 1 and Option 2 have their pros and cons. Option 1 may bring litigation risk, while Option 2 implies a complicated change in the ECB’s reserve framework. Both cast unhelpful doubts about change of terms in future ECB liquidity operations. Assuming they both result in TLTRO balances being remunerated at 0%, all options are an incentive for banks to repay TLTRO loans early and their scope shouldn’t go further than that. We should also mention that it wasn't discussed in the most recent press report – a change in the TLTRO lending rate to banks would achieve the same results but bring the same drawbacks.

Option 3 is more momentous, in that it could outlive TLTRO. We’ve discussed various tiering designs in a recent publication, and compared them to Swiss and UK situations. The design that seems to have retained the ECB’s attention is one where some portion of each bank’s EL would earn the deposit rate up a certain threshold, and where any EL above that threshold would earn 0%. This option does create an incentive for banks to repay TLTRO funds early, but will also ‘save’ the ECB interest expenses in the longer run. We think it will also compound the widening of money market spreads in subsequent years.

The ECB should succeed in causing early TLTRO repayments

Source: ECB, ING

A faster reduction in excess liquidity

The most immediate effect of these measures will be to push banks to reduce their TLTRO balances faster. As things stand, the largest repayment is due in June 2023 but maturities stretch to as far as end-2024. By making TLTRO carry-negative we expect a large chunk of them to be repaid. Of course, in the context of growing funding market stress, it would be understandable that some banks keep some TLTRO balances as a precaution. Out of the €2.1tn TLTRO balances a first €0.5tn early repayment in December 2022, and another €0.5tn in March 2023, once year-end funding uncertainty has eased, are realistic.

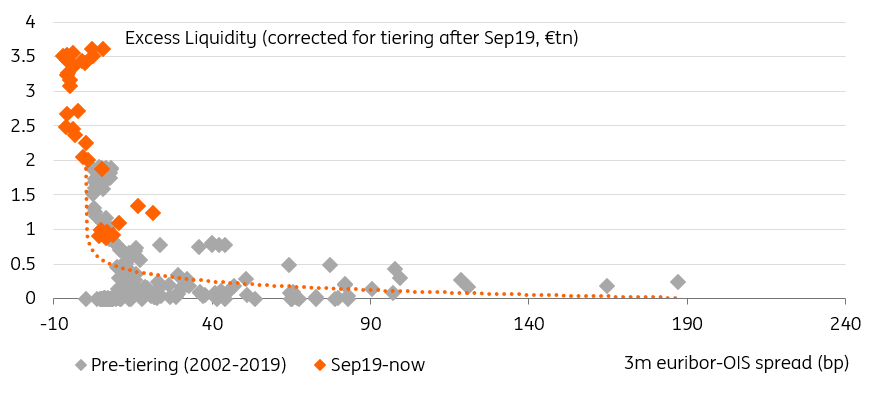

Excess liquidity is still high enough that an immediate €1tn drop should not affect money market rates much, but there is a catch. If the price of liquidity will not change much, the credit premia should rise on the combined effect of less liquidity chasing yields, and on a slightly greater systemic risk resulting from less abundant central bank funding at a time when the economy is heading into a severe recession. This means the chart below probably understates the widening of Euribor-Estr basis that could occur in 2023.

Estr-deposit rate on the other hand should remain more stable, and could even drop temporarily as the deposit rate risks no longer being the marginal interest rates for some money markets. This is one of the shortcomings of this tiering design that we've discussed in more details in an earlier publication.

Lower liquidity will eventually widen money market spreads

Source: Refinitiv, ING

Collateral scarcity: a light at the end of the tunnel?

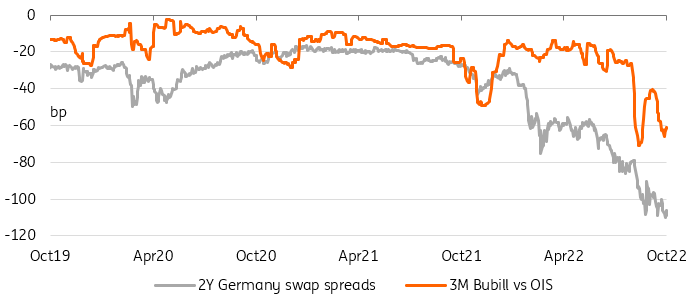

Another important implication of an earlier reduction of EL might be a change of dynamic in the repo market. Early TLTRO repayments means easing collateral scarcity. We think the impact would be mostly indirect because core repo rates have remained below the ECB’s deposit rate, offering no incentive to banks to get their liquidity away in exchange for collateral. Lower liquidity overall should, however, affect non-banks actors and their reliance on the repo market.

An earlier reduction in EL will compound other factors with a more direct effect on collateral scarcity. Governments in the eurozone are expected to increase their borrowing to finance energy support packages, including the much-discussed €200bn German plan, but with possible joint EU issuance also adding to the supply of safe collateral. Quantitative Tightening (QT) will in all likelihood be phased out and will also serve to ease the pressure on the collateral market by reducing the size of ECB bond hoarding.

The above doesn’t address the important issue of government deposits being remunerated at 0% (down from the deposit rate currently) after end-April 2023. To be sure, some of this liquidity will find itself deposited back at commercial banks, denting the effect of early TLTRO repayments, but the balance will still amount to a significant incentive for government entities to push cash out in exchange of collateral.

Lower will help ease collateral pressure, a little

Source: Refinitiv, ING

More By This Author:

U.S. Spending Strains Intensify

Asia Week Ahead: China’s 20th Party Congress Is The Highlight

Rates Spark: Keeping Up The Hawkish Pressure

Comments

Log in or sign up to join the conversation.