Image Source: Pixabay

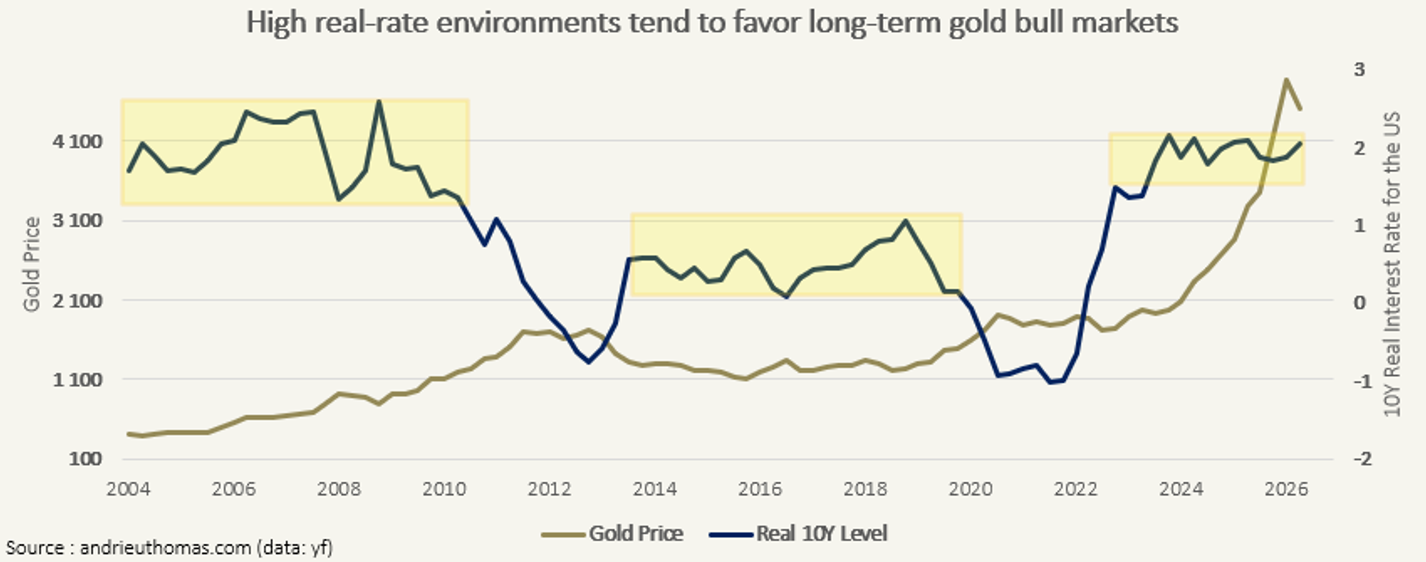

The price of gold in euros has just broken an all-time record! An ounce of gold is now at €2,300, double its price of five years ago:

Gold soars while oil plummets, particularly in the last quarter. With oil and gold prices so decorrelated in recent months, gold miners are likely to report even stronger-than-expected results:

Graphically, the GDX index, which measures the sector's overall performance, is in an optimal buying configuration after successfully testing its resistance line. The current prices of many mining companies look set for a strong upward impulse, provided their results reflect the decorrelation between gold and oil as expected:

Oil is down, as are all commodities.

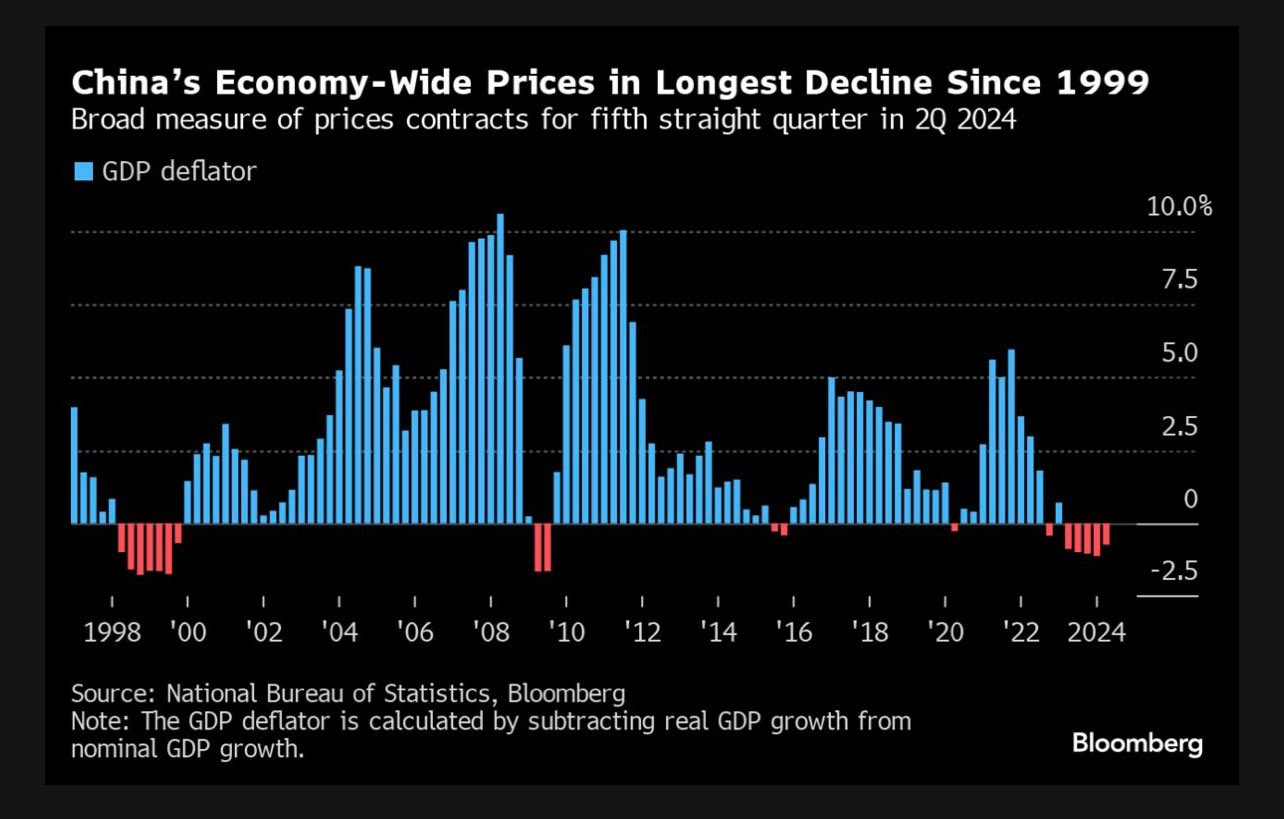

The main reason for the fall in commodities is the deflationary situation in China:

China is slowing down at a pace not seen since the last financial crisis. It is difficult to predict the repercussions of such a slowdown on the global economy, as the last time China suffered a similar slowdown, its economy was much smaller than it is today. As China's share of world trade has grown considerably, the potential repercussions of this slowdown on international trade and other economies are amplified.

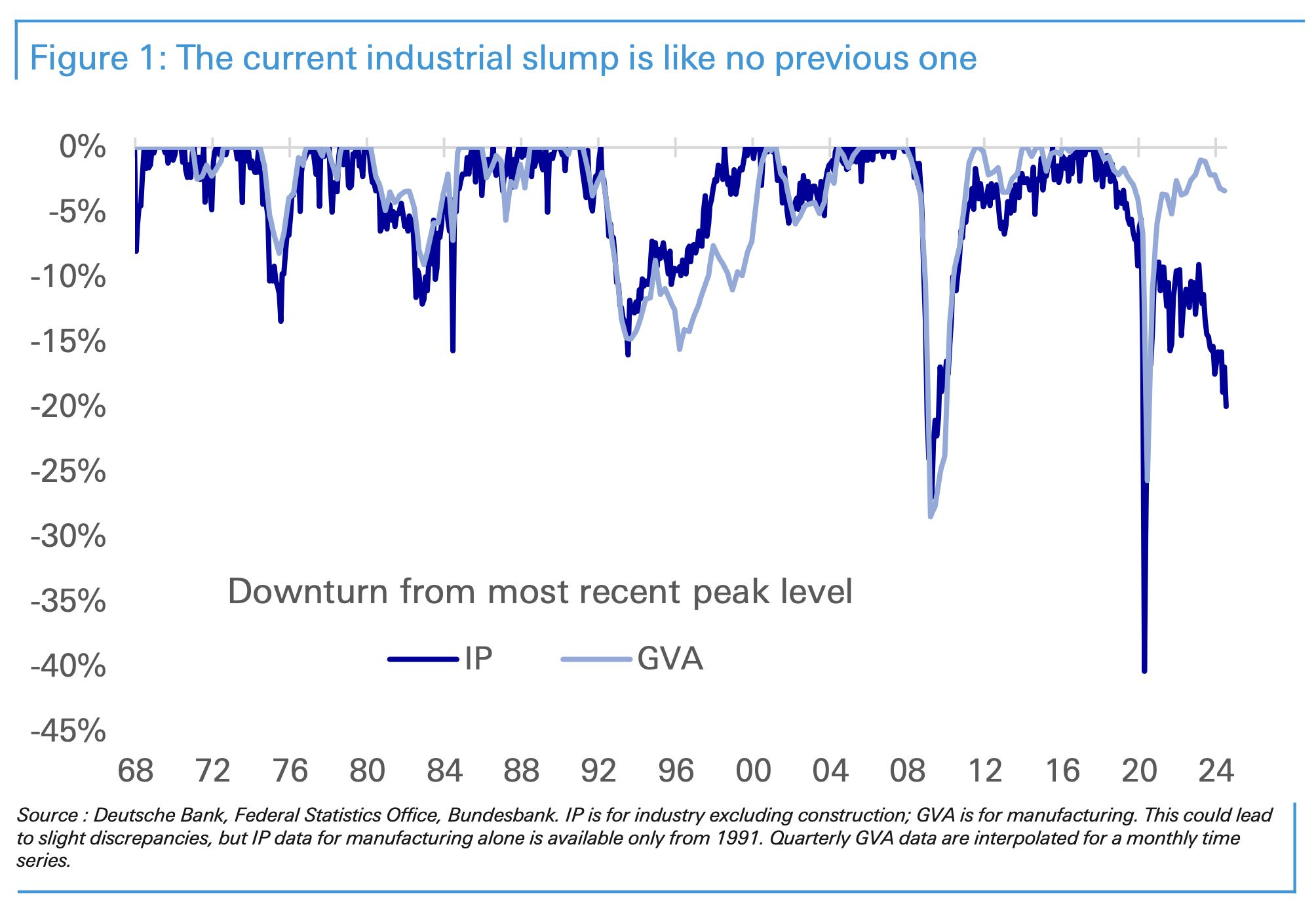

Germany has been hit hard by the economic slowdown in China. Having already suffered from rising energy costs linked to the war in Ukraine, Germany's export-intensive economy is now facing a decline in Chinese demand. This slowdown is having a direct impact on its business model, exacerbating the difficulties faced by German industrial companies, which depend heavily on the Chinese market:

The current industrial downturn is unprecedented, with a sharper and more sustained fall than in previous crises, notably those of 2008 and 2020. This contraction exceeds past downturns, highlighting the major challenges facing the industrial sector.

This time, the German slowdown seems more structural.

Europe's industrial engine is in sharp decline, raising the question of the ability of southern European countries - the “Club Med” members - to manage their debt repayments. Without the industrial growth of the eurozone's major economic powers, such as Germany, these countries could find themselves in difficulty. Indeed, the solidity of the European economy is essential to guarantee fiscal stability and the repayment of sovereign debts.

Among the countries at risk, France is currently the first to be mentioned. Unlike the sovereign crisis of 2011, when it was not as often in the front line, France is consistently among the worst performers, with growing concerns about the seriousness of its fiscal situation.

France has had to request an extension from the European Commission to submit its public deficit reduction plan, originally scheduled for September 20. This request aims to bring the plan into line with the 2025 Finance Bill. Under the European excessive deficit procedure, France must return to a deficit below 3% by 2027. However, unforeseen local authority spending and disappointing tax receipts could worsen the deficit, requiring additional savings estimated at around €110 billion by 2027.

France is threatened by economic stagnation, with GDP forecast to decline by -0.1% for the final quarter of 2024, according to Insee. Second-quarter growth has also been revised downwards. Although Insee maintains a growth forecast of 1.1% for 2024, the higher-than-expected deficit and the slowdown in economic activity complicate the preparation of the 2025 budget. These factors could reduce tax revenues and future growth, creating budgetary uncertainty.

As was the case in Greece in 2011, France will not be able to avoid an austerity plan with very high social costs. The end of the year promises to be another turbulent one!

On the other side of the Atlantic, austerity plans are not among the topics debated by the candidates in the forthcoming US presidential election. Despite a worrying deficit and rising debt refinancing costs, this issue seems to be ignored by the main candidates.

At the same time, the US economy is also experiencing a slowdown, but it is above all persistent inflation that is causing concern. This “sticky inflation” continues to affect monetary policy and the country's economic outlook.

The Consumer Price Index (CPI) rose again this month, indicating that inflation persists. We are now at 51 consecutive months of month-on-month price increases.

Although CPI inflation for August stands at 2.5%, it is significantly higher for several essential goods. For example, car insurance is up 16.5%, transport 7.9%, hospital services 5.8%, cost of homeownership 5.4%, rents 5%, car repairs 4.1%, food away from home 4%, and electricity 3.9%.

Inflation affects essential services, which explains why, despite an official rate of 2.5%, Americans have the impression that inflation is much higher. This perception is amplified by the sharp rise in prices in key everyday sectors.

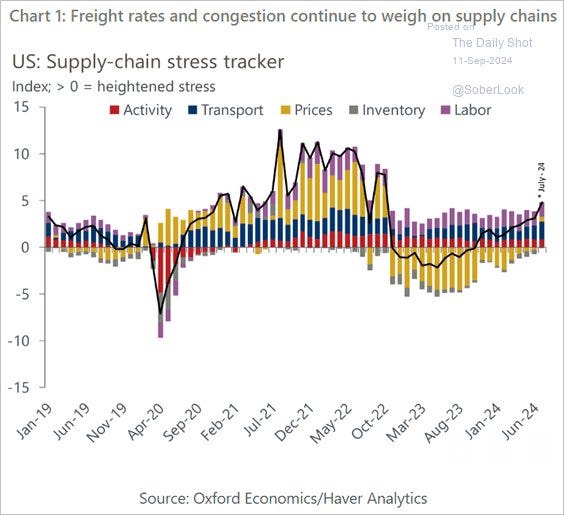

Inflation is unfortunately not about to stop in the country, partly due to the deterioration of the supply chain, notably because of transport problems:

Prospects of strikes at Atlantic ports and rising shipping costs increase the risk of ongoing supply chain disruptions. These developments should be monitored closely, as they could exacerbate inflationary pressures in the United States.

More By This Author:

Gold: A Way To Optimize Your SavingsWhat Will Trigger The Second Phase Of Inflation?

Money Printing Contributes To Growing Inequalities

Comments

Log in or sign up to join the conversation.